BlueScope Steel Ltd

.png)

BSL Dividend Details

Strong financials and foundation:BlueScope Steel Ltd (ASX: BSL) estimates its first half of 2016 underlying EBIT to be around $50 million or 40% higher than its second half 2015 levels. Also, the company's chairman commented that BSL is making good progress on its restructuring and cost reduction plans. Additionally, in mid-November BSL employees at the Port Kembla Steelworks voted in favour of the new Enterprise Agreements thereby supporting more than $200 million in game-changing cost outs. Also, progress towards the $50 million cost-out target at New Zealand Steel is going at a good pace and the Board has decided that steelmaking at Glenbrook should continue. Meanwhile, for the financial year 2015, BSL recorded net profit after tax of $136.3 million with four out of five company's operating segments recording better financial performance. This was in comparison to a net loss of $82.4 million in the previous year.

.png)

High performing U.S. North Star BlueScope Steel (Source: Company Reports)

In November, BSL completed its move to full ownership of the North Star joint venture business in the U.S. by acquiring the remaining 50% from Cargill. The North Star Bluescope Steel is a high performing U.S. steel mill with a high EBITDA margin of 16.6% (as of March 31, 2015) compared to U.S. industry average of 8.2%. Also, North Star capacity utilization stands at 100% compared to U.S. industry average of 74%. Given the positive outlook, we recommend a “BUY” for this stock at the current price of $4.10

BSL Daily Chart (Source: Thomson Reuters)

Crown Resorts Ltd

.png)

CWN Dividend Details

Focusing on Core Australian markets to offset Macau Pressure:James Packer, the Australian billionaire, quit the board of Crown Resorts Ltd (ASX: CWN) in mid-December, four months after stepping down from the company's Chairman position as the casino group's gambling revenue is on a downtrend since 18 consecutive months in Macau. The stock has risen 10.23% in the last one month (as at January 12, 2016), though Macau gross gaming revenue in December plunged by 21.2%. For the financial year 2015, normalised Net Profit after Tax (NPAT) attributable to Melco Crown Entertainment’s (MCE) was $525.5 million, down 17.9% from prior year. Crown’s share of MCE normalised NPAT was $161.3 million, down $129.9 million or 44.6%. On the other side, Crown Melbourne results were positive while Crown Perth were subdued, however, both witnessed strong international VIP gaming growth. VIP program play revenue at the Australian resorts grew 41.8% to $955.9 million, while EBITDA grew by 14.1%. Moreover, Fitch Ratings affirmed CWN's Long-Term Foreign-Currency Issuer Default Rating (IDR) and senior unsecured rating at 'BBB' with a stable outlook.

These ratings reflect company's strong market position in the Melbourne and Perth markets, driven by its position as the sole casino licence holder in the two Australian states it currently operates - Victoria and Western Australia, the robust performance of its Australian assets, and its stable financial profile. We assign a “Buy” on this stock at the current price of $12.07

CWN Daily Chart (Source: Thomson Reuters)

REA Group Ltd

.png)

REA Dividend Details

Attractive syndication:REA Group Ltd (ASX: REA) expanded syndication model with iProperty Group Limited (ASX: IPP) following its intent to acquire 100% of the company in early 2016 for a cash consideration of $4 for each IPP share ($750 million takeover bid). Currently, REA has 22.7% shareholding in IPP which holds real estate websites in Malaysia, Hong Kong, Indonesia, Macau and Thailand where the advertising market is expected to be 30% larger than Australia. All Australian listings on REA Group’s Chinese language property site myfun.com will be syndicated to a selection of iProperty Group’s sites operating across Hong Kong and Southeast Asia. The syndication has expanded since its trail of 3,000 listings in August 2015 to include more than 40,000 Australian property listings from myfun.com, which include residential and commercial listings and development projects. On the other side, REA group also delivered solid revenue growth of 21% to $146 million and core operations EBITDA growth of 30% to $82 million from year ago period in first quarter financial year 2016. Rising Australian top tier listing products coupled with higher listing volumes in the Australian market, REA delivered an improvement in the revenue growth rate during this quarter.

.png)

Growing performance over the years (Source: Company Reports)

For the full financial year 2015, the company recorded a 20%, 27% and 24% growth in revenue, EBITDA and net profit respectively. Based on strong fundamentals and attractive developments in REA given the current trading conditions wherein the stock is close to its 52-week high price and surged about 11.40% in the last three months (as at January 12, 2016), we suggest a “HOLD” rating on this stock at the current share price of $52.03

REA Daily Chart (Source: Thomson Reuters)

Medibank Private Ltd

.png)

MPL Dividend Details

Ongoing Strong performance:Medibank Private Ltd (ASX: MPL) recorded a pro forma group net profit after tax of $291.8 million which is 13% ahead of Prospectus forecast and 12.9% higher from 2014 levels. In the health insurance segment, the company recorded 33.8% increase in operating profit led by focus on improved claims management processes and management expense improvements. Medibank also announced an inaugural dividend of 5.3 cents per share fully franked higher than prospectus forecast of 4.9 cents per share. Implied full year dividend of 7.4 cents per share (inclusive of pre-IPO dividend to Commonwealth) represents payout ratio of 70%.

.png)

Fiscal Year of 2015 NPAT Performance (Source: Company Reports)

MPL forecasted its health insurance outlook and estimates premium revenue growth target above 5.5% in financial year 2016. Health insurance operating profit is foreseen above $370 million financial year 2016.

Management expense ratio target is set at 8.3% for financial year 2016 and below 8% in financial year 2017. From healthcare market standpoint, health funds still seem to have a central funding role and may increase the scope of Private Health Insurance. Led by the first year performance of MPL and decent dividend yield, we assign a “BUY” rating to this stock at a current price of $2.19

MPL Daily Chart (Source: Thomson Reuters)

TPG Telecom Ltd

.png)

TPM Dividend Details

Boosting capital position: TPG Telecom Ltd (ASX: TPM) is boosting its capital position via $300 million of equity raising through bookbuild process. The group generated a strong performance during the fiscal year ended on 2015, with revenue and EBITDA rising by 31% year on year (yoy) to 33% yoy respectively boosted by AAPT acquisition contribution coupled with organic growth.

.png)

Fiscal year of 2015 (Source: Company Reports)

TPG is expanding its offerings via iiNet acquisitions as well as won two major contracts with Vodafone Hutchinson Australia. However, the stock is trading at higher valuations at a higher P/E while dividend yield is relative low. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price.

TPM Daily Chart (Source: Thomson Reuters)

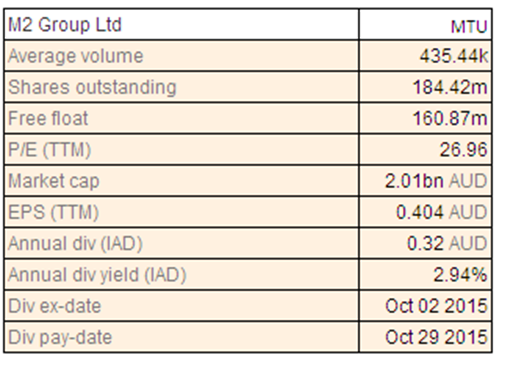

M2 Group Ltd

MTU Dividend Details

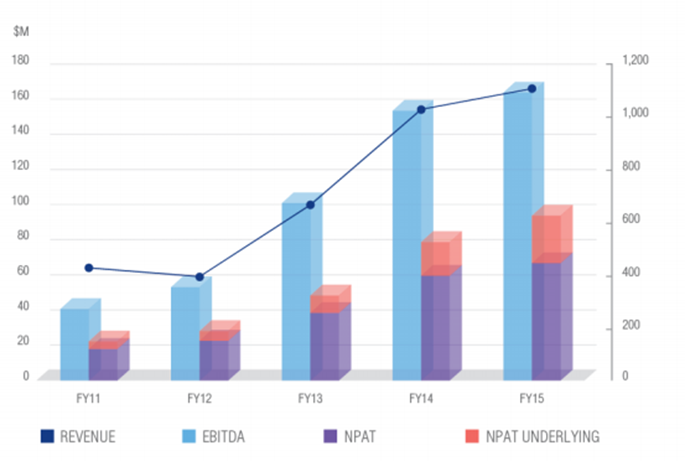

Positive Outlook: M2 Group Ltd (ASX: MTU) consumer segment added over 95,000 services while business segment delivered organic growth with over 12,000 new services during fiscal year of 2015. MTU connected to 21 NBN Points of Interconnect during FY15, and currently connected to 52 POIs to target more than one million premises. The group estimates to offer services to 220,000 customers across Consumer, Business and Wholesale segments while expects 431,000 services in operation across Fixed voice, Broadband and Mobile. Management forecasts a revenue growth of 24% to 26% in FY16 while NPAT is estimated to rise over 30% to 35%. M2 Group recently agreed to merge with Vocus Communications, with MTU shareholders getting 1.625 Vocus shares for each M2 share. The merged entity has been expected to be strategically placed to leverage the NBN in Australia and UFB in New Zealand. Meanwhile, the combined revenue before synergies is estimated to be over $1.8 billion and EBITDA would by $370 million in fiscal year of 2016 while the market capitalization would be more than $3 billion.

MTU group Fiscal year of 2015 (Source: Company Reports)

M2 estimates to generate over cost synergies of $40 million per annum which might be fully realized by the end of FY18. MTU stock rallied over 12.76% in the last three months but fell 3.92% in the last one month (as of January 12, 2016). Based on the foregoing, we give a “HOLD” recommendation on the stock at the current price of $11.07

MTU Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.