Brickworks Limited

.png)

BKW Dividend Details

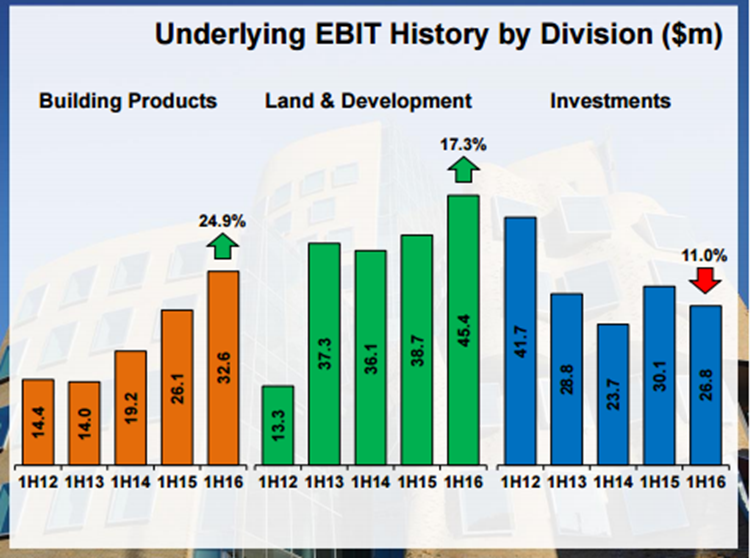

Solid performance but higher valuation: Brickworks Limited (ASX: BKW) stock surged over 5.15% (as of April 06, 2016) in the last four weeks as the group reported a solid decent half year performance ended on January 2016 wherein the Underlying Net Profit After Tax surged 19.4% on a yoy basis. The Building Products EBIT and Land and Development EBIT rose by 24.9% and 17.3%, respectively.

Segment-wise performance (Source: Company Reports)

However, the investments segment EBIT fell by 11% yoy to $26.8 million during the period. Meanwhile, we believe that the recent rally in the stock placed the group at higher valuations with an unreasonable P/E. Accordingly, we give an “Expensive” recommendation to this dividend yield stock at the current price of $15.70

BKW Daily Chart (Source: Thomson Reuters)

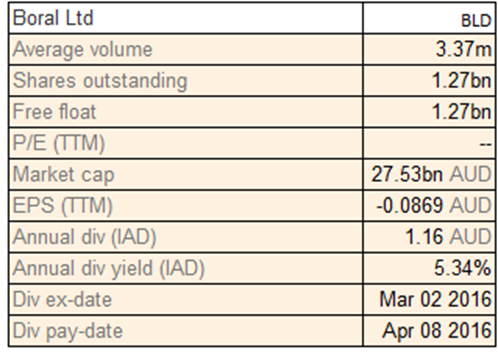

Boral Limited

BLD Dividend Details

Recovering performance in US markets: Boral Limited (ASX: BLD) revenues in the United States surged 29% during the first half of 2016 to $512 million as well as reported a positive EBIT of $8 million against the negative $8 million in pcp. This increase in the region is driven by the Cladding revenue which rose by 4% to US$190 million, Roofing revenue growth of 11% as well as better performance from the Fly Ash & Construction Materials. The group also enhanced its bottom line by 31% yoy to $ 137 million during the period as its efforts of controlling costs have paid off. Boral Gypsum segment revenues delivered 13% yoy growth in revenues, driven by higher overall pricing wherein the Australia/NZ region’s board volumes rose by 12% while average selling prices improved by 5%. Accordingly, BLD stock price rallied by 21.73% in the last six months (as of April 06, 2016). BLD reported a decline of 4% yoy in reported revenue for 1H16 to $2,194 million. Building Products segment revenues plunged by 27% to $192 million while Construction Materials & Cement segment revenues fell by 8% yoy to $ 1,489 million.

Given the ongoing weakness from Chinese markets despite recovering activity from the US and Australia, we believe that the group’s top line would continue to be under pressure in the coming periods. Hence, we recommend “Expensive” for this dividend yield stock at the current price of $6.38

BLD Daily Chart (Source: Thomson Reuters)

Aurizon Holdings Ltd

.png)

AZJ Dividend Details

Building long term prospects: Aurizon Holdings Ltd (ASX: AZJ) stock fell over 24.47% (as of April 06, 2016) in the last six months impacted by its heavy impairment charges in first half of 2016 due to falling commodity prices and costs from west Pilbara Iron Ore project. Recently, the group received notices from seven of the eight Wiggins Island Rail Project clients, who want to exercise their right under relevant agreements in order to decrease financial exposure in Aurizon Network with regards to the Wiggins Island Rail Project. In view of this, AZJ earlier provided its FY16 EBIT guidance of $845 million to $885 million that assumed zero revenue for the WIRP fee. On the other hand, we believe that the group’s long term prospects look promising. The group even extended its NSW coal haulage agreement which would enable them to enhance their haulage volumes from present 18 million tonnes per annum (mtpa) up to a maximum of 26 mtpa.

The group’s ongoing buyback program at current corrected stock prices indicates management confidence to generate returns in stock for the coming months. Hence, we believe that investors need to leverage the recent correction as an entry opportunity and accordingly we place a “BUY” on this dividend yield stock at the current price of $3.81

AZJ Daily Chart (Source: Thomson Reuters)

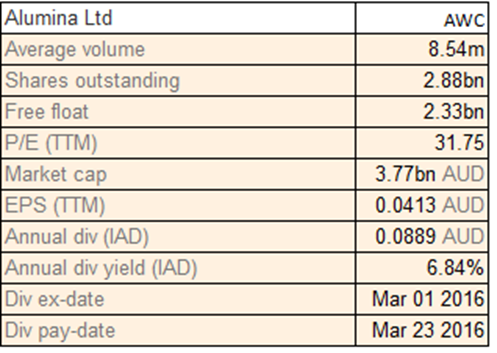

Alumina Limited

AWC Dividend Details

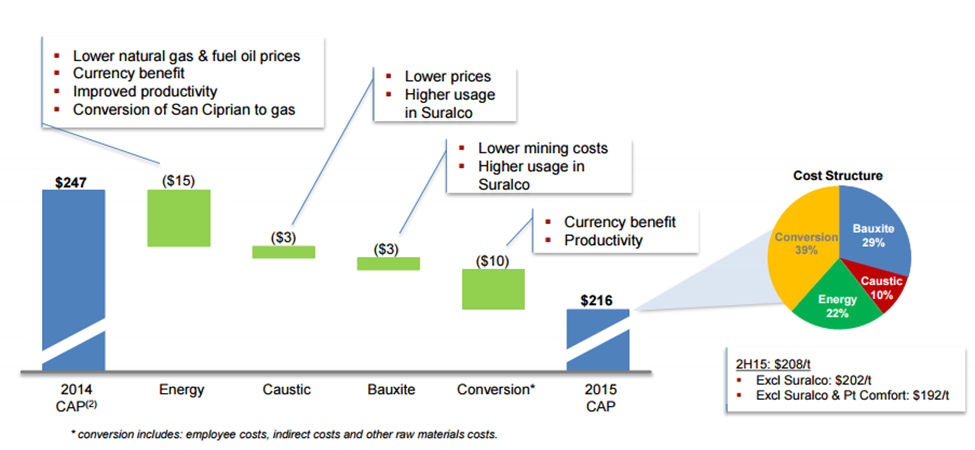

Supply agreements and efficiency improvement: Alumina Limited (ASX: AWC) stock fell over 20% (as of April 06, 2016) in the last one year due to falling aluminum prices. But, the group managed to deliver statutory net profit after tax of US$88 million for fiscal year of 2015 despite the falling prices pressure, against the net loss in fiscal year of 2014. AWAC contributed to this strong bottom line growth as the segment’s EBITDA surged by US$689 million to US$990 million during the period despite US$170 million for restructuring. The segment also improved its cash from operations by $333 million to $809 million, while the group made $300 million prepayment for the Western Australian gas supply agreement. To withstand the commodity pressure, AWAC focused on its costs paid off as Cash cost of alumina production fell by US$33 per tonne while the Average realized price of alumina declined US$9 per tonne. Meanwhile, management issued a weak outlook given the falling aluminum prices and oversupply of alumina due to Atlantic and Chinese refining curtailments.

Decreasing Cash cost of alumina production per tonne (Source: Company Reports)

However, management reported that they would be able to maintain their margins given factors such as the API pricing shift and production efficiency.

AWAC has also signed multiple bauxite supply contracts worth a value of more than $350 million over the next two years from existing mines with customers in China, Europe and Brazil. Accordingly, AWC stock recovered over 14.54% during this year to date (as of April 06, 2016). We recommend a “HOLD” on this dividend yield stock at the current price of $1.305

.PNG)

AWC Daily Chart (Source: Thomson Reuters)

Whitehaven Coal Limited

.png)

WHC Details

Targeting Asian opportunity: Whitehaven Coal Limited (ASX: WHC) enhanced its net profit after tax by $85.7 million to $7.8 million for the first half of 2016, partly driven by its Maules Creek production and decreasing unit cost per tonne to 58 as compared to 63 in the prior corresponding period (pcp). Given these strong results, WHC stock recovered over 3.97% in the last four weeks alone (as of March 31, 2016). Meanwhile, the group is targeting the booming opportunity for electricity demand in Asia and has accordingly positioned itself by producing few highest quality coals for premium Asian seaborne markets.

.png)

High quality for Asia (Source: Company Reports)

Management upgraded guidance and now expects Saleable Coal Production in the range of 19.5Mt to 20.1Mt for the full year of 2016. WHC estimates the Narrabri’s wider longwall production commencement and a full production from Maules Creek by FY2019. We believe that the stock has the potential to rise further in the coming months and accordingly give a “speculative buy” at the current price of $0.625

.PNG)

WHC Daily Chart (Source: Thomson Reuters)

OZ Minerals Ltd

.png)

OZL Dividend Details

Expansion of resource base: OZ Minerals Limited (ASX: OZL) rallied over 29.90% in the last six months (as of April 06, 2016), driven by its ongoing expanding resource base and prospects, stock buyback and positive financial performance. Recently, the group reported that its first phase drilling at Prominent Hill ore bodies generated positive results. The first phase drilling program started in the fourth quarter of 2015 and delivered 68.5m @ 3.2 percent copper, 0.5 grams per tonne gold; 29.3m @ 2.5 percent copper, 0.7 grams per tonne gold; 16.8m @ 3.4 per cent copper, 0.7 grams per tonne gold; 15.2m @2.0 per cent copper, 1.0 grams per tonne gold; and 32m @ 2.9 grams per tonne gold.

Management is confident that its production capacity of the Prominent Hill underground operation would increase up to 4mtpa and OZL intends to expand the life of the mine beyond 2026. Despite generating such strong stock returns, OZL is still trading at a reasonable P/E and has a good dividend yield. Based on the foregoing, we give a “Hold” recommendation at the current price of $5.15

OZL Daily Chart (Source: Thomson Reuters)

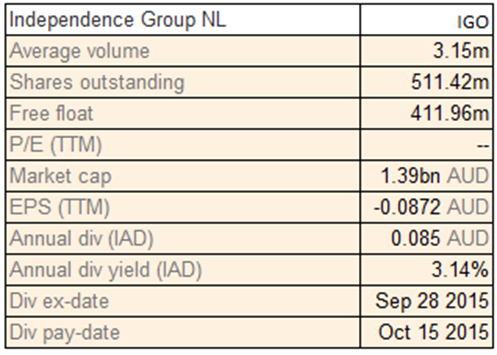

Independence Group NL

IGO Dividend Details

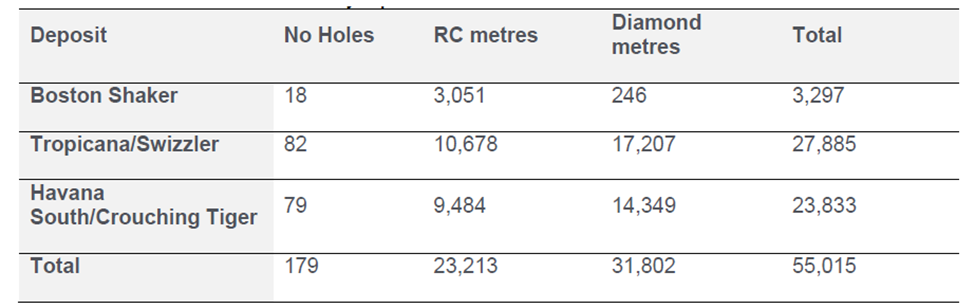

Promising Tropicana Gold mine potential: Independence Group NL (ASX: IGO) recently revealed the potential of its Tropicana Gold Mine, as its extensive drilling program in 2015 generated positive results, promising similar grades and continuity at par with its current resource. The drilling results indicated the strike as well as depth extensions of the mineralization.

Deposit Drill meters results from June 2015 (Source: Company Reports)

Accordingly, IGO stock rallied over 18.5% (as of April 06, 2016) in the last three months and we believe that the stock has more scope for growth given its long term Tropicana Gold Mine prospects. IGO has formally withdrawn from the Darlot JV agreement with no retained interest in the tenements. On the other hand, IGO has awarded two underground diamond drilling contracts to Swick Mining Services at Jaguar and Nova mine sites. We still remain bullish on this stock and recommend a “BUY” at the current price of $2.70

IGO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.