Company Overview : - Sirtex Medical Limited is a medical device company with primary objective of manufacturing and distributing liver cancer treatments utilizing small particle technology to markets in Asia-Pacific; Europe, the Middle East and Africa (EMEA), and North and South America. The Company segments include Asia Pacific, Americas and EMEA. Its lead product is SIR-Spheres Y-90 resin microspheres, which is a targeted radioactive treatment for liver cancer. The treatment is called Selective Internal Radiation Therapy (SIRT) and consists of a minimally invasive surgical procedure performed by an interventional radiologist. The SIR-Spheres microspheres lodge in the small blood vessels of the tumor where they destroy it from the inside while sparing the surrounding healthy tissue. The Company is also engaged in conducting other studies, which include SIRFLOX and FOXFIRE Global for liver metastases, and RESIRT for primary renal cell carcinoma. SIR-Spheres is available in over 40 countries.

SRX Details

Ongoing growth in SIR-Spheres in FY16: Sirtex Medical Limited (ASX: SRX) has continued to deliver growth and reported a 32% growth in the total revenue to $232.5 million during the fiscal year of 2016 as compared to the prior corresponding period. This performance is driven by the group’s ongoing rise in dose sales of SIR-Spheres® Y-90 resin microspheres product and a 16.4% growth in the global dose sales to 11,931 units. The growth came from the double-digit growth in the Americas region and within the Europe, Middle East and Africa region (EMEA). Moreover, the favorable impact from the depreciation of the Australian Dollar against the US Dollar and Euro also drove the performance. In addition, the group’s efforts in sales and marketing infrastructure boosted the dose sales. The group generated a five year CAGR in dose sales of 23.2% as of fiscal year of 2016. Moreover, the net profit after tax has increased by 32.8% to $53.6 million during the period and is in-line with reported revenue growth. The adjusted net profit after tax on the constant currency basis, has increased by 17.3%.

.png)

FY 16 Financial Performance (Source: Company Reports)

Boosting cash flow to position itself for future:The group has reported a strong organic five-year compound annual growth rate (CAGR) of 35.4% in earnings per share (EPS). In FY 16, SRX has reported a 31.3% growth in EPS to 93.7 cents as compared to the prior corresponding period. This has led SRX to increase its annual dividend to shareholders, and the dividend per share (DPS) grew 50% against the prior period. Additionally, the DPS of SRX has grown at a CAGR of 33.8% for the five-year period. Given its strong performance, the group was able to boost its net cash flow which rose at a five-year CAGR of 20.1% and in FY 16, the net cash flow grew on a solid basis by 44.7%. This is despite the fact of the group being in an aggressive investment phase of its growth particularly in the sales and marketing and clinical studies function. Sirtex has a cash of $107.02 million as of fiscal year of 2016 as compared to $73.94 million from fiscal year of 2015. Having a zero debt, the group’s capital position is very strong. Sirtex is aiming to retain two thirds of the earnings for growth initiatives, and commensurate with the 2020 Vision strategy. The group intends to return over one third to the shareholders by way of dividends.

.png)

EPS, DPS and Cash growth (Source: Company Reports)

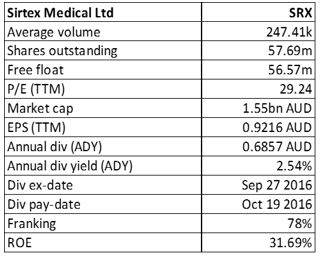

Strengthening focus on EMEA and APAC other than America:SRX has a five-year global dose sales at a CAGR of 19.1% in which over 71% of the dose sales volume is from the Americas. In EMEA, the good growth markets are Belgium and the UK. SRX has received reimbursement in the Netherlands and South Africa in FY 16, and expects a further reimbursement in FY 17. Moreover, in APAC, the major growth came from Australia and also from the solid performance in Taiwan, Singapore and Thailand. In addition, SRX has appointed a new distributor in order to re-establish supply into South Korea in FY 16 while achieved regulatory clearance in Canada.

Regional Growth (Source: Company Reports)

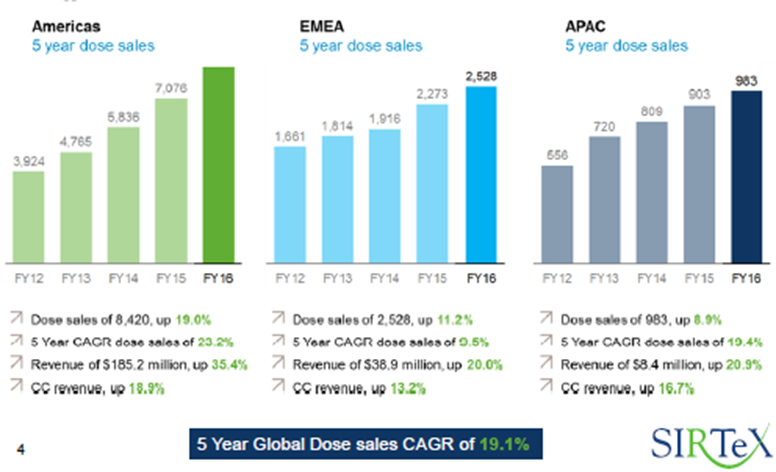

Long-term growth strategy:SRX has given 12 consecutive years of positive dose sales growth and the group forecasts to continue this trend even for the coming years. But, what’s more exciting is that the group has an excellent long term growth potential as they are now penetrated only 2% of their potential market till date. SRX intends to expand into new markets and there are three major clinical studies to report their results. The group is also making efforts to maximize while totally realizing their potential of SIR-Spheres microspheres in both primary and secondary liver cancer and other cancers. This is the first pillar, while research and development is the second pillar. Mergers & acquisitions is the third pillar of the growth strategy of SRX.

2020 Vision Growth Strategy (Source: Company Reports)

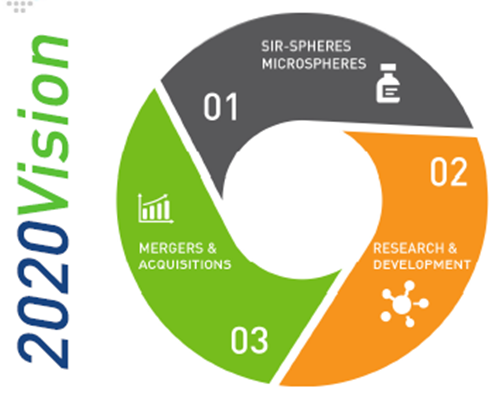

Clinical studies’ highlights:SRX has finished patient recruitment of the large clinical studies, SIRveNIB and SORAMIC clinical studies in FY 16 which means completing the patient recruitment in all five of the major clinical studies in a timely manner and this represents over 2,340 patients globally. Overall, SRX has made the total clinical investment of $20.6 million in FY 16, which represents 8.9% of sales. Moreover, combined SIRFLOX, FOXFIRE and FOXFIRE Global studies in CY 17 the, along with the SARAH and SIRveNIB studies, all have been expected to report Overall Survival data in the first half of the year. SRX intends to undertake a combined prospective meta-analysis on the two studies SARAH and SIRveNIB, which is called VESPRO while the results are forecasted by CY 17. Additionally, SRX continues to support a range of other clinical studies across multiple disease indications with kidney cancer pilot study, RESIRT, and a new study, called SIRCCA targeting rarer form of primary liver cancer called cholangiocarcinoma. Sirtex is trying to gain competitive edge by targeting niche markets which could lead to lucrative opportunities. The group launched a prospective US patient registry, called RESIN wherein the registry is targeting enrolment of over 500 patients per annum across all types of primary and secondary liver cancers. The group anticipates their RESIN registry to offer them wide range of benefits including further clinical evidence, clinician education and data to potentially support regulatory submissions and reimbursement. The group has initiated 18 sites while enrolled 150 patients till date.

Clinical Investment (Source: Company Reports)

Outlook for FY 17: SRX is expending its core SIR-Spheres microspheres business globally and expects their double-digit dose sales growth to continue even for fiscal year of 2017 given their potential market penetration opportunity. Moreover, there is an investment undergoing into sales and marketing, clinical and medical for long term growth, but we believe that the group could bear this burden given its solid cash position. Additionally, there is an anticipation of SARAH, SIRveNIB and SIRFLOX / FOXFIRE / FOXFIRE global results to be out in the first half of CY17. Positive results could further trigger further opportunities for the group.

Stock Performance:The shares of SRX stock fell over 15.28% in the last one month (as of November 04, 2016) as the investors were expecting a higher dose sales growth for fiscal year of 2016. Moreover, Gilman Wong, the CEO of the group offloaded shares worth over $2 million recently which also added to the stock pressure. On the other hand, we believe that the group is well positioned to maintain their dose sales growth in the long term and any further regulatory approvals in new markets (including China, Japan and Canada) could further drive the stock. CEO still has substantial holding in the stock indicating their long-term confidence on the stock. Accordingly, we believe long term investors need to leverage the recent correction in the stock given the stock fall of over 33.9% during this year to date (as of November 04, 2016). With major clinical results being expected in fiscal year of 2017, any positive result could trigger the bullish momentum in the stock while the company is also working for a long-term vision of 2025 growth. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of – $27.11

.PNG)

SRX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.