Company Overview - Mineral Deposits Limited (MDL) is an Australia-based company focused on the mineral sands sector through the joint venture interest in TiZir Limited (TiZir). MDL and ERAMET SA each own 50% of TiZir, which owns the Grande Cote Mineral Sands Project in Senegal, and the Tyssedal ilmenite upgrading facility in Norway. The Grande Cote Mineral Sands Project is located on the coast of Senegal starting approximately 50 kilometers north of Dakar and extends northwards for more than 100 kilometers. The main Heavy Mineral (HM) deposits identified to date are Diogo, Mboro, Fass Boye and Lompoul. In January 2014, Mineral Deposits Limited disposed its interest in Teranga Gold Corporation. In June 2014, the Company announced that AMP Ltd and its related bodies corporate has ceased to be the substantial holder of the Company.

Analysis - Mineral Deposits (MDL) reported its result for full year ended 31 December 2014 which was found to be slightly weaker than what we expected. Mainly, the result was impacted by the operating cash flow. The progress at Grande Côte (GCO) is on track for September completion without any instant funding concerns given the US$41 million ($52 million) accessible on the Tyssedal working capital facility and the US$50 million GCO working capital facility undrawn. Then, US$25 million also can serve as a buffer if required from shareholder perspective. Further, there is no debt and no expected future cash commitments to TiZir in 2015. TiZir is expected to remain funded through the progress at GCO and the furnace reline at Tyssedal in the September quarter. The GCO is estimated to be free cash positive by mid-year. MDL also conveyed that although the demand for slag and zircon continued to be solid, the pricing has been soft. There has been a drop in demand and pricing for ilmenite in view of the impact of Chinese supply.

.png) Financial Summary (Source – Company Reports)

Financial Summary (Source – Company Reports)

The results primarily entailed underlying net loss of $18.5 million with MDL’s share of TiZir’s underlying loss totaling $21.2 million. This reflects lower contribution from TiZir Titanium and Iron ilmenite (TTI) in view of the lower titanium slag prices coupled with the operating losses from GCO.

.png) Dredge and Wet Concentrator Plant (Source – Company Reports)

Dredge and Wet Concentrator Plant (Source – Company Reports)

However, TTI has been conveyed to remain profitable with EBITDA of $24.5 million despite current market conditions. TiZir witnessed an impairment loss of $110.8 million and MDL reported a net loss after tax of $71.7 million after taking account the non?cash impairment charge of $49.9 million against TiZir’s consolidated assets, a non?cash impairment charge of $1.8 million against the investment in World Titanium Resources Limited and the Company’s share of TiZir’s amortization of assets recognized on acquisition of $1.5 million (after tax).It is to be noted that irrespective of the usual commissioning issues for TiZir, dredge ramp?up is witnessing momentum, and wet plant and ilmenite circuit are operating at design feed rates. The Company stated that impact on TiZir’s results emanate from adverse market conditions alongside the commencement of the commissioning of GCO. Specifically, the weak titanium feedstock market played a great role with average prices for titanium slag dropping in first half of 2014 before stablising throughout the second half of the year. The lower prices with lower volumes of titanium slag and lower volumes of high purity pig iron following planned maintenance shutdown of the smelter in March cumulatively led to the 61% dip in TTI EBITDA as compared to that of 2013. GCO also recorded an EBITDA loss of $24.2 million. However, the mining rates at GCO amplified 44% to 6.4Mt in 4Q14 exiting the year at about 60% of nameplate. The impellor issues which impacted production have been resolved.

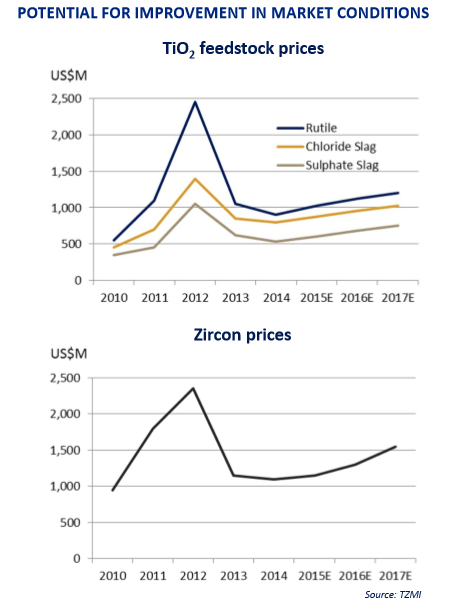

Market Dynamics (Source – Company Reports)

Market Dynamics (Source – Company Reports)

As part of the 2015 updated GCO mineral resource and ore reserves, it has been reported that GCO’s life of mine has been extended to 2043. The rise in mineral resource has been estimated to 27.3 million tonnes of heavy minerals and the increase in ore reserve has been indicated to 21.7 million tonnes of heavy minerals.

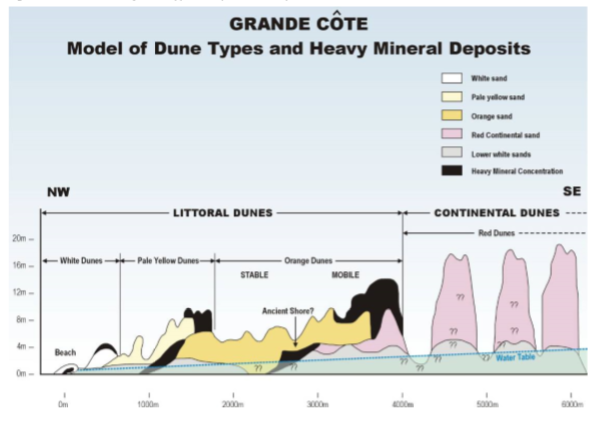

Cross Section of Dune Type Heavy Mineral Deposits (Source – Company Reports)

Cross Section of Dune Type Heavy Mineral Deposits (Source – Company Reports)

As per the Company’s outlook, ramping-up of operations at GCO will continue during 2015. However, the full operating capacity is expected to be reached in the third quarter of 2015. During the same quarter, the electric furnace at TTI is planned to be relined with the existing roof to be upgraded with a water?cooled copper ceramic roof. This upgrade will help enhance smelting capacity by about 15% and will help manage lengthened time frames between scheduled shutdowns. The Company further conveyed that the cost of the furnace expansion will amount to about $70–$80 million and the plant will be shut down for three months during the time of maintenance. This entire project is expected to create an opportunity for producing both chloride and sulphate titanium slag within the same furnace, i.e., TiZir will be a fully integrated producer then. In order to produce chloride titanium slag, the required ilmenite will be supplied by GCO. This will help having supply of ilmenite from within the group while reducing the requirement of engaging any third party for the sales of ilmenite. It is expected that with the completion of relining of the furnace, TiZir will have the ability to supply a range of titanium feedstock to global customers and the tractability to produce different feedstocks based on varied market demand.

The key points still entail MDL’s efforts to pass through the transition successfully and have higher margins from production flexibility; maintain production of vital by?products (premium zircon and high purity pig iron); have immense advantages in strengthening flexibility subject to market conditions; and exploring logistical advantages from Senegal to Norway to key customers in Europe and the eastern seaboard of the US. Further, a security of off-take for GCO and ilmenite supply for TTI is expected to be provided by the vertical integration effort. The progress at GCO will enable TiZir to be a cost?competitive producer with competitiveness at all stages of the mineral sands pricing cycle.

.png) 2015 Year of Transition (Source – Company Reports)

2015 Year of Transition (Source – Company Reports)

On 03 March 2015, the Company also announced about US$16.2 million government grant for the TTI ilmenite upgrading facility. More particularly, TiZir which is jointly owned by MDL and Eramet has received advice that its application for funding, by its wholly owned subsidiary TTI totaling NOK122m (about US$16.2m) has been approved by Enova, a Norwegian government agency that promotes energy efficiency and the use of environmentally friendly energy technology. The funds will be received upon final approval by the European Free Trade Association Surveillance Authority.

.png) 2015 and 2016 Sales Volume (Source – Company Reports)

2015 and 2016 Sales Volume (Source – Company Reports)

Some bottlenecks do include fluctuations in AUD, ramp-up risk at GCO and further weakening in mineral sands prices. However, other results emanating from transition efforts will help the Company attain momentum. For instance, chloride slag and zircon are expected to have a considerable contribution to revenue and EBITDA from CY15 onwards. It is also expected that buying with respect to sulfate ilmenite which has seen a lot of turbulence, will pick up soon given the possibility of ramping-up of industrial activity in China. The medium term which is likely to bring stability in prices. Further, an expected increase in exposure to US TiO

2 demand will altogether be supportive.

.png) MDL Daily Chart (Source - Thomson Reuters)

MDL Daily Chart (Source - Thomson Reuters)

In view of the above, we reinstate a

BUY recommendation for this stock at the current price of $0.80.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.