Company overview - Healthscope Limited is a healthcare provider. The Company is engaged in the provision of healthcare services through the ownership and management of hospitals and medical centers, and the provision of pathology diagnostic services. The Company's segments include Hospitals Australia, Pathology New Zealand, and Other. The Hospitals Australia segment is engaged in the management and provision of surgical and non-surgical private hospitals. The Pathology New Zealand segment is engaged in the provision of pathology services in New Zealand. The Other segment is engaged in the provision of pathology services in Malaysia, Singapore and Vietnam, and the provision of practice management services in medical centers in Australia. The Company operates approximately 45 private hospitals with over 4,800 beds. The Company owns and operates approximately 40 medical centers, over four skin cancer clinics and a breast diagnostic clinic in Australia.

.PNG)

HSO Details

Rise in revenue and operating EBITDA for first half 2017: Healthscope Ltd (ASX: HSO) has reported a 3.9% growth in the group revenue to $1,192.0 million during the first half of 2017. Accordingly, the group reported a 5.1% growth in the group operating EBITDA to $216.8 million during the period. Moreover, the Hospitals Operating EBITDA delivered a growth of 2.2% despite the softer operating environment, driven by strong growth in New Zealand pathology while the group made efforts to enhance flexibility in the Hospitals cost base in light of ongoing market variability. On the other hand, the Statutory NPAT fell 7.0% to $90.5 million. However, HSO has posted an increase in depreciation due to completion of three major hospital expansion projects in 2HFY16, as well as increased investment in New Zealand pathology and investment in theatre technology. There is an increase in the net interest expense primarily due to the Gold Coast Private project finance converting to senior debt post-completion. The non-operating expenses relate to appointment of liquidators for a supplier group, corporate restructuring and commissioning costs. On the other hand, New Zealand Pathology Operating EBITDA grew 31.5% to $30.5 million.

.png)

First half of 2017 Financial Performance (Source: Company Reports)

Hospital expansion plan: In Hospital expansion plan, HSO has finished two projects in 1HFY17 while intends to finish two more major projects in the remaining half of the year. The two projects which were finished in 1HFY17 include Darwin Private (two theatres) and Northpark Private (emergency department). There is ongoing commitment to hospital expansion strategy based on the strong fundamentals of chosen markets and performance to date relative to the market and underlying portfolio. The company has invested $247 million in growth projects during the first half of 2017, including Northern Beaches Hospital development.

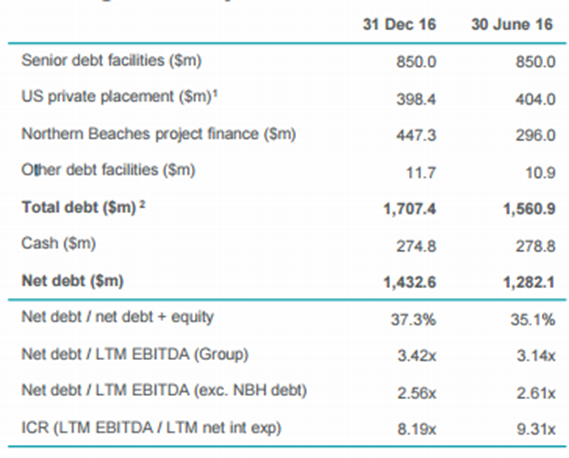

Funding capacity:The hospital expansion program continues to be funded through a combination of cash reserves, operating cash flow and available debt facilities. HSO’s existing facilities are sufficient to fund current hospital expansion program. The Gold Coast Private project finance debt are converted to senior debt 2HFY16 after the project completion. There is an increase in net debt in the 1HFY17 predominantly related to Northern Beaches hospital project financing (which is excluded from all bank covenants) and the capital payment for public portion of hospital and shared facilities would be received from NSW Government post transfer of patients from the existing hospitals.

Funding Summary (Source: Company Reports)

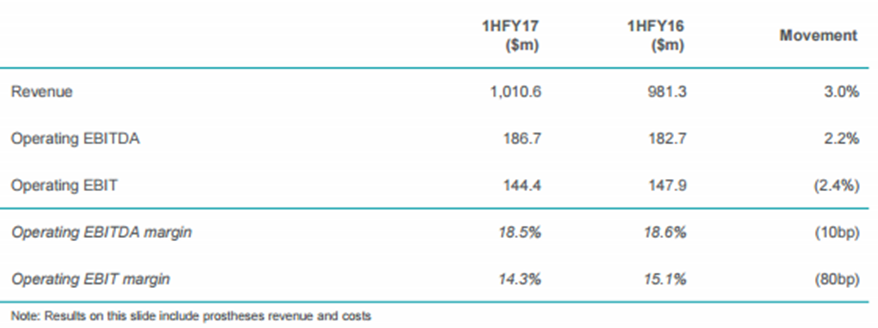

Performance of the Hospitals in 1HFY17: In the first half of 2017, there is a sound result despite lower volume growth and increased volatility in case mix A compared to historical long term trends. The group had implemented several initiatives to enhance marketing and business development activities as well improved the flexibility of the cost base to better respond to ongoing market variability. The company has increased focus on information technology in strengthening referrals, expanding services and driving more efficient business processes. This is through the continued investment to increase scope of robotic surgery offered at key sites, commencement of pilot of digitized medical records and enhancement of Healthscope Assist application to improve specialist search functionality. With regards to underlying portfolio performance, the slower revenue growth and reduced operating EBITDA margin across the portfolio are driven by the lower volume growth and increased volatility in case mix. Most states and territories are experiencing similar conditions and hence the company has undertaken site by site review to develop action plans in order to improve responsiveness to more variable market conditions. HSO has also successfully renegotiated multi-year contracts with health fund partners that includes NIB and the Australian Health Service Alliance. With regards to major hospital expansion portfolio performance, HSO has outperformed the market and underlying HSO portfolio during 1HFY17 with strong revenue growth and higher operating EBITDA margin. The Hospital expansion projects are expected to increase volume and optimize case mix by year three following completion of each project. HSO has completed major expansion projects in 2HFY16 that includes Gold Coast Private (QLD), National Capital Private (ACT) and Knox Private (VIC).

Hospitals’ Performance in 1H 2017 (Source: Company Reports)

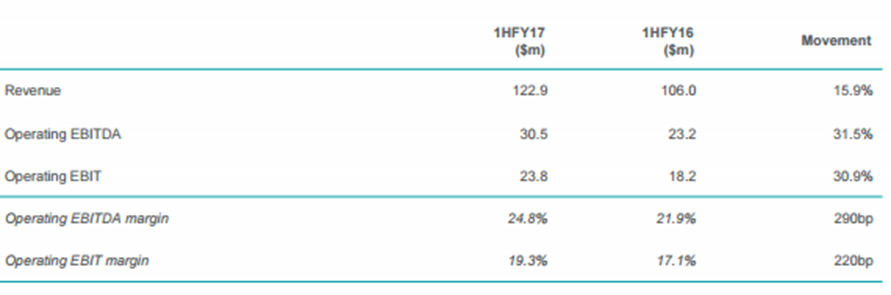

Performance of the New Zealand Pathology in 1HFY17: During the first half of FY 17, the New Zealand Pathology continues to deliver strong revenue while operating EBITDA growth is forecasted to be stronger than expected. This performance is driven by the non-government community pathology revenues in Wellington after the commencement of new DHB services in the region, greater penetration of the veterinary market and continued economies of scale being achieved with investment in new technology and new services. HSO has begun World Anti-Doping Agency (WADA) testing after the successful accreditation in 2HFY16. The company has started rollout of electronic doctor ordering system to improve data collection and increase efficiencies. The group has successfully renewed three DHB contracts in advance of maturity. Moreover, HSO’s focus remains on maintaining strong relationships with government, delivery of efficiency improvements benefiting both HSO and the DHB partners, as well as expanding commercial revenue streams.

New Zealand Pathology Performance (Source: Company Reports)

Performance of the Other Segments in 1HFY17:In 1HFY17, Singapore pathology’s revenue grew 4.7% and the EBITDA grew 6.6%. There is a robust revenue growth with continued growth in specialist and commercial contract markets. The company is investing in next-generation technology and tracking system to drive further automation and efficiencies. Moreover, the Malaysia pathology revenue grew 6.8% and the EBITDA grew 6.8%. This is due to the volume growth recovered in 1HFY17 after an 18-month period of subdued activity and an established three new laboratories in private hospitals, in line with strategic priority of increasing penetration of hospital and specialist markets. However, the Medical centers revenue declined 5.7% and EBITDA declined 13.5%. This is due to the ongoing impact of Medicare fee freeze that continues to negatively impact performance and review of increased private billing model and alignment of cost base to activity levels.

Outlook:The group expects market variability to continue in the short term and if current trends continue, Hospital operating EBITDA growth in 2HFY17 is expected to be similar to 1HFY17. However, the medium to long term fundamentals remain unchanged. Moreover, the group expects FY17 depreciation and amortization to be in the range of $113 million to $115 million and the FY17 net interest expense is estimated to be in the range of $55 million and $57 million.

Stock Performance:HSO stock fell over 23.6% in the last six months as at March 03, 2017, given the weaker performance across the segments. The group expects a similar performance if the conditions prevailed. On the other hand, the stock has consolidated and rose over 2.71% in the last three months (as of March 03, 2017) with operating EBITDA improvements. The group is now securing long-dated contracts, and has renegotiated multi-year contracts with NIB and the Australian Health Service Alliance. The company has successfully renewed three DHB contracts in New Zealand in advance of maturity. Nine projects are under construction that would generate a further 792 beds and 49 operating theatres by the end of FY19. Overall, HSO’s hospital expansion program is believed to increase capacity and to help generate operating leverage for earnings growth over the medium term. Further, positive industry fundamentals for private hospitals, favorable insurance membership trend and government policy can boost the performance going forward. We give a “Buy” recommendation at the current price of – $ 2.25

.png)

HSO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.