Asciano Ltd

.png)

AIO Dividend Details

Performance pressure despite cost cutting initiatives: Asciano Ltd (ASX: AIO) revenues fell by 4.3% year on year (yoy) to $1,863.4 million in the six months ended on December 2015, impacted by declining volumes on the back of slowdown in the economy. Despite delivering a decent Queensland coal volumes, AIO’s volumes in the Western Australian were moderate. But the group made efforts to offset its top line impact to a certain extent by undertaking BIP initiatives which contributed over $39.7 million leading to a total of over $298 million. Accordingly, Underlying EBITDA rose by 0.8% while Underlying NPAT improved by 6.6% yoy to $214.3 million during the period.

.png)

Overall BIP Savings Under five year plan in $millions (Source: Company Reports)

Meanwhile, AIO stock has been consolidating since the last one month and slightly declined by 1.66% (as of March 09, 2016) and we believe that the stock would be under pressure in the coming months given its low single digit underlying EBIT growth guidance for fiscal year of 2016.

The timelines for acquisitions have also been suspended by ACCC. Moreover, the stock is trading at higher valuations with a high P/E and has a low dividend yield. Based on the foregoing, we give an “Expensive” recommendation for the stock at the current price of $8.88

AIO Daily Chart (Source: Thomson Reuters)

RCG Corp Ltd

.png)

RCG Dividend Details

Boosting capital position: RCG Corp Ltd (ASX: RCG) surged over 4.22% in the one month (as of March 09, 2016) driven by its successful capital raising of over $50 million via fully underwritten placement at $1.50 per share, which is a discount of over 7% to the volume weighted average price of the group’s shares for the five days before the 24

th February 2016. The group is issuing over 33.3 million new shares, which account over 7% of its present issued capital in capital raising. With this move, RCG would be boosting its balance sheet and positioning itself for potential growth. The group would repay its $28 million vendor note and intends to roll out over 35 to 40 stores in the coming eighteen months.

We believe that the stock has more potential to generate returns. Accordingly, we give a “HOLD” recommendation to investors at the current price of $1.64

RCG Daily Chart (Source: Thomson Reuters)

SEEK Ltd

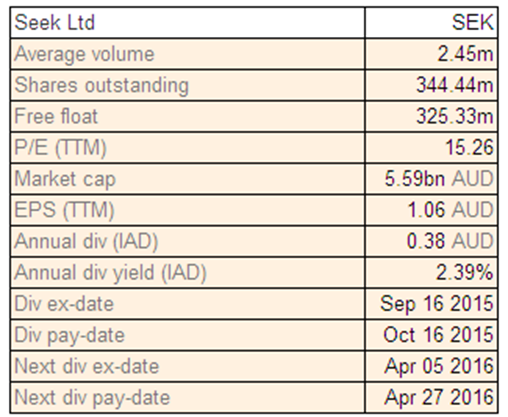

SEK Dividend Details

Maintaining market leadership: SEEK Ltd (ASX: SEK) continued to maintain its leading position in first half year of fiscal year of 2016, reporting over 33% of placements and 8x lead as compared to its closest competitors.

The group’s Australia and New Zealand division reported a revenue increase of 15% on a yoy basis during the first half of fiscal year of 2016 while EBITDA rose by 18% yoy. The group delivered better performance in its international segment with revenue and EBITDA rising by 34% and 36%, respectively. The group forecasts to maintain its overall revenue growth in the range of 15% to 18% for FY16. Seek’s Premium Talent Search has also been performing well during the period, while SEEK profiles rose over 41% yoy to 7.1 million. SEEK stock surged over 32.03% in the last six months (as of March 09, 2016), but still trading at attractive valuations with a reasonable P/E. We give a “HOLD” recommendation on the stock at the current price of $16.17

SEK Daily Chart (Source: Thomson Reuters)

Gentrack Group Ltd

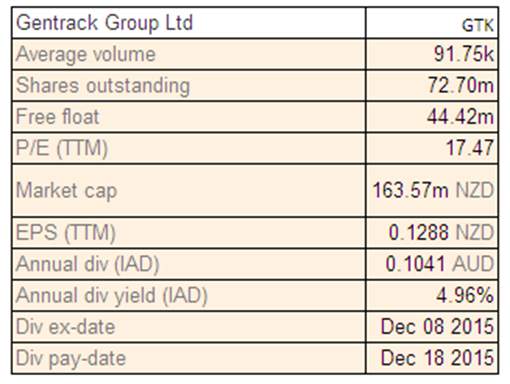

GTK Dividend Details

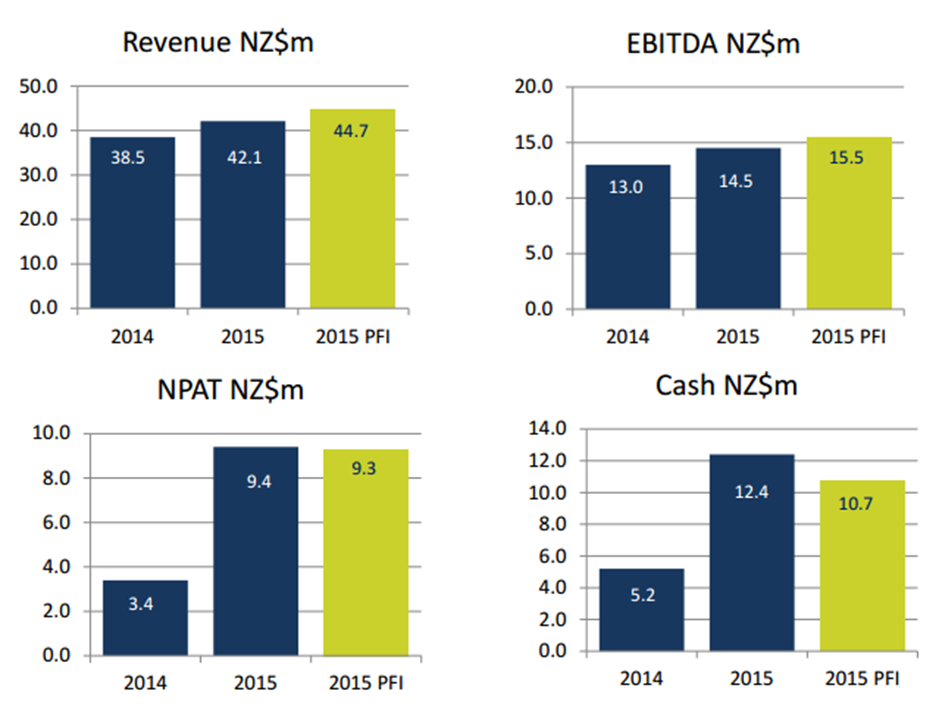

Revenue numbers fall short of forecasts: Gentrack Group Ltd (ASX: GTK) delivered below estimated fiscal year of 2015 results. The company’s revenues for FY15 were New Zealand dollar (NZ$) 42.1 million, falling short of prospectus forecast by NZ$2.6 million but an increase of about 9% over the previous year revenue of NZ$38.5 million. The company witnessed an increase in operating expense of 8.3%. Net profit after tax (NPAT) was NZ$9.4 million, marginally higher than the forecasted NZ$9.3 million. Utility division, which constitutes about 84% of the total revenue, grew by only about 8.1% over last year. As for FY 2016 forecasts, Gentrack has some large projects ongoing that are expected to contribute to a strong 2016 revenue.

Fiscal year of 2015 performance (Source: Company Reports)

The company’s Airports division is currently doing well with an increase of 15.7% over previous year and is well placed to continue a strong growth in FY16. In another development, the CEO of the company, James Docking, who was with the company for over 20 years has stepped down. In view of these parameters and the market scenario for the company, we maintain an “Expensive” rating on the stock.

GTK Daily Chart (Source: Thomson Reuters)

Scentre Group

.png)

SCG Dividend Details

Strong operating financial numbers: Scentre Group (ASX: SCG) has announced funds from operations (FFO) of AUD $1.199 billion, which amounts to 22.58 cents per security. This represents an increase of about 3.8%, which is slightly above the previous market guidance of 3.5%. There was a negative impact on FFO earnings due to asset sales but the underlying operating performance has covered up for that. The company will pay a distribution for full year of 20.9 cents per security. Net operating income (NOI) grew at the rate of 2.6%, marginally higher than the forecasted range of 2.0%-2.5%.

.png)

Retail Sales Growth (Source: Company Reports)

The company maintains total assets of over AUD 31 billion with net assets over AUD 19 billion. It has 10693 retail outlets in Australia and 977 in New Zealand. All of these data points indicate a stable performance of the company. For the 2016 full year forecast, funds from operations are expected to grow by about 3%, while the distribution per security is expected at 21.3 cents per share, or a 2% growth. The corresponding NOI growth is forecasted in the range of 2.5% to 3.0%. We recommend a “HOLD” for this stock at the current price of $4.41

SCG Daily Chart (Source: Thomson Reuters)

Macquarie Atlas Roads Group

.png)

MQA Dividend Details

Improving toll revenues: Macquarie Atlas Roads Group (ASX: MQA) announced a full year net profit after tax (PAT) for the year ended December 31, 2015 of AUD 85.1 million. This was a turnaround from the previous year’s loss of AUD 50.6 million. A significant portion of this profit was because there were no new performance fees for the 12 months ended June 30, 2015. The same fees last year were AUD 58.2 million. This resulted in a decreased operating expense of AUD 30.8 million in 2015 from AUD 83.8 million in 2014. Further revenue from operations increased significantly by about 22% from 2.1 million in 2014 to 2.6 million in 2015. The company owns about 20.1% stake in Autoroutes Paris-Rhin-Rhône (APRR), which witnessed a rise in traffic (about 2.7%) that gave increased toll revenues, partly due to the improving economy of France. The company is also looking for acquisition opportunities to complement the revenue stream from Europe.

.png)

Consistent growth through economic cycles (Source: Company Reports)

Macquarie Atlas also gained net proceeds of US $120 million due to divestment of non-core assets. The company paid fiscal year of 2015 distributions of 16 cents per share and has raised the distribution guidance to 18 cents per share (up 12.5 %) for FY 2016. The stock price has surged 40.06% in the last one year (as at March 09, 2015). We recommend a “HOLD” at the current price levels $4.60

MQA Daily Chart (Source: Thomson Reuters)

Caltex Australia Ltd

.png)

CTX Dividend Details

Record profits in an inconsistent oil market: Caltex Australia Ltd (ASX: CTX) reported record profit after tax (PAT) of AUD 628 million, which is an increase of about 27% from the last year’s profit of AUD 493 million. The profit number falls in the estimated guidance range of AUD 615-635 million that was announced in December 2015. This significant increase in profit was despite the revenue falling by about 17% from AUD 24.23 billion in 2014 to AUS 20.03 billion in 2015. This decrease can be attributed to the impact of significant fall in global crude oil prices. The weighted average Brent crude oil price in 2015 was US $51 per barrel as against US $101 per barrel in 2014. This was offset by the decrease in total expenses by about 19% primarily due to lower replacement cost of goods sold owing to the lower price of refined product. The profits were also driven by a good demand for premium fuel products, including Vortex Diesel at the company’s service stations that offsets the long term decline in demand for unleaded petrol.

This growth in penetration of premium products is due to targeted investment, new retail service stations, refurbishment of existing stations and the increase in marketing spends. Owing to the increased profits, the company announced an off-market share buyback of AUD 270 million. The company stock dropped about 13.13% in the last one month (as at March 09, 2016). We give a “HOLD” recommendation on this stock at the current price of $32.01

CTX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.