Carsales.Com Ltd

.PNG)

CAR Details

Strong revenue growth expected in FY17: Carsales.Com Ltd (ASX: CAR) has reported a growth of 10% in operating revenue to $344.0 million for FY 16 as compared to FY15 and the adjusted net profit grew 9% to $110.5 million. Moreover, CAR’s dealer revenue increased by 10% year on year (yoy). The private seller revenue grew by 19% and the display revenue grew 9% year on year. The Finance and related services showed strong growth with gross profit up 29% year on year. Brazilian and South Korean international investments reported strong local currency revenue growth. Additionally, CAR had acquired 83% of Chileautos in Chile during the second half of FY 16 and had acquired 65% of SoloAutos during the first half of FY 16. In addition, the Domestic core business performance in the first month of FY17 was strong. The company is continuing to build scale and breadth with a number of promising opportunities. CAR is expecting FY17 revenue and EBITDA growth to remain strong due to stable market conditions.

Internationally, CAR is expecting no further deterioration in market conditions and the trialing of the lead model into Brazil to be a good growth contributor to local currency revenue and earnings in FY 17. Korea is expected to see continued solid local currency revenue and earnings growth.

.png)

Revenue & EBITDA Performance (Source: Company Reports)

In addition, CAR is expecting the ongoing integration of core carsales IP and technology into Chilean and Mexican businesses which would offer solid uplift in revenue and earnings in FY 17. On the other hand, investors have been recently concerned over the limited potential of Australian division growth. Investors are worried over a further double digit growth on Australia by the group.

The group is holding its AGM on October 28, 2016. Still the stock is trading at a higher P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $12.36

.png)

CAR Daily Chart (Source: Thomson Reuters)

Freelancer Ltd

.PNG)

FLN Details

Acquisition of assets of Escrow Angel and its automotive brand Protecti: Freelancer Ltd (ASX: FLN) has acquired Australian online escrow service Escrow Angel and its automotive brand Protecti. Moreover, FLN reported a 56% increase in the net revenue to $26.2 million in 1H 2016 as the Gross Payment Volume grew 453% to $354.9 million on prior corresponding period. FLN has achieved positive operating EBITDA of $0.1 million. Moreover, FLN is focusing on an increased investment in talent and on repositioning the newly acquired Escrow.com business for growth.

FLN stock rose over 9.93% in the last six months (as of October 07, 2016) and we believe the momentum would continue in the coming months. We maintain a “Buy” recommendation on the stock at the current price of $1.50

.png)

FLN Daily Chart (Source: Thomson Reuters)

Nextdc Ltd

.PNG)

NXT Details

Capital Raising: Nextdc Ltd (ASX: NXT) recently completed $150 million placement and entitlement offer ($45 million raised via retail entitlement offer). The capital is being raised to fund the second Sydney data center. NXT was under a trading halt until the opening of trade on September 07, 2016.

Meanwhile, the revenue surged 52% to $92.8 million in FY 16 beating the guidance of $85 million to $90 million. EBITDA has increased 247% to $27.7 million, meeting the top of its guidance range of $25 million to $28 million.

.png)

FY 16 Financial Performance (Source: Company Reports)

NXT has reported a statutory net profit of $1.8 million, as compared to a net loss of $10.3 million in FY 15. In addition, NXT expects the revenue to be in the range of $115 million to $122 million for FY17, which is an increase of 24% to 31% against FY 16. The EBITDA is expected to be in the range of $46 million to $50 million, an increase of 66% to 80% on FY 16.

Meanwhile, NXT stock rose 48.95% in the last six months (as of October 07, 2016) and still we give a “Hold” recommendation on the stock at the current price of $4.05

.png)

NXT Daily Chart (Source: Thomson Reuters)

CogState Limited

CGS Details

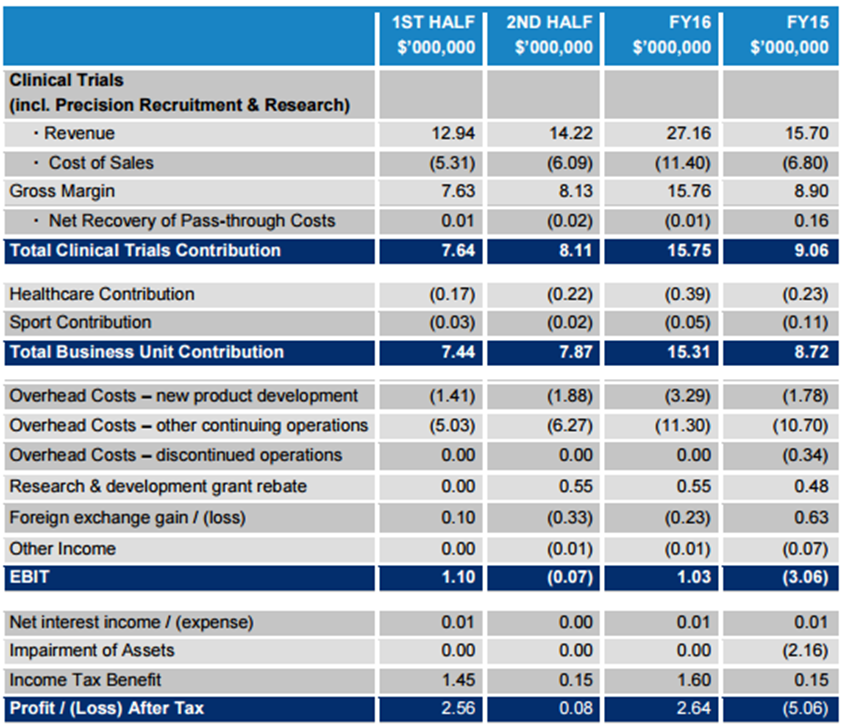

Concerns over cost rise in FY 17: CogState Limited (ASX: CGS) reported a 69% growth in the revenue to A$27.3m in FY 16 as the Clinical Trials revenue grew 68% to A$25.6m.

As per the guidance, CGS has reported positive Earnings before Interest & Tax (EBIT) in FY16 of A$1.03 million as compared to the loss of $3.06m in FY 15 and a Net Profit after Tax (NPAT) of A$2.6 million against the loss of $5.06m in FY 15. Moreover, CGS expects the revenue to grow 60% to A$17.5 million in FY 17.

FY 16 Financial Performance (Source: Company Reports)

However, CGS expects that the overhead costs related with new product development would increase beyond the $3.29 million costs incurred in the FY 16. The total cost of new technology development is expected to increase in the range of A$5.5 - A$6.0 million in FY 17.

Moreover, CGS stock has already risen 27.01% in the six months (as of October 07, 2016) placing them at slightly higher levels and accordingly, we give an “Expensive” recommendation on the stock at the current price of $0.87

CGS Daily Chart (Source: Thomson Reuters)

Hansen Technologies Limited

.PNG)

HSN Details

Growth rates in FY 17 to be lower than FY 16: Hansen Technologies Limited (ASX: HSN) reported a 40% yoy increase in the operating revenue to $148.9 million in FY 16.

The net profit after tax grew 54.4% yoy to $26.1 million and the earnings per share is up 42.7% yoy to 14.7 cents on FY 2015. Moreover, HSN would finish the integration of PPL Solutions, acquired effective 1st July 2016 in FY 17.

FY 16 Financial Performance (Source: Company Reports)

On the other hand, the growth rates for FY 2017 have been forecasted to be limited, wherein the revenue is expected to be in the range of $165 million to $175 million while the EBITDA margin is expected to be between 25% and 30%.

Moreover, HSN stock already rose over 24.59% in the last three months (as of October 07, 2016), placing them at a higher P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $4.58

HSN Daily Chart (Source: Thomson Reuters)

Xero Ltd

.PNG)

XRO Details

Growth of the subscribers and the global revenue: Xero Ltd (ASX: XRO) is growing with the addition of 242,000 new subscribers in FY16 to 717,000 globally versus 222,000 for the year to September 2015. At this current rate, XRO should exceed 1 million global subscribers in the next year.

Moreover, XRO in FY 16 has reported operating revenue of $207.1 million, which is an increase of 67% on FY15. The global revenue grew 95% in international markets on year-on-year basis and 57% growth in Australia and New Zealand.

.png)

Subscription Growth (Source: Company Reports)

Meanwhile, Xero has crossed quarter billion annualized revenue. Moreover, with the increase in subscription, XRO can add roughly NZ$100 million of annualized revenue. XRO’s annualized committed monthly revenue is $257.9 million, which is an increase of 62% on year-on-year basis.

Meanwhile, XRO stock rose 19.76% in the six months (as of October 07, 2016). Accordingly, we give a “Buy” recommendation on the stock at the current price of $17.56

XRO Daily Chart (Source: Thomson Reuters)

Altium Limited

.PNG)

ALU Details

Weak operating cash flow in FY 16: Altium Limited (ASX: ALU) reported a revenue growth of 17% to $93.6M in FY 16 and 29.3% of EBITDA margin growth, while achieved $100.4M sales. There is a 20% increase in number of new AD licenses sold and 11% increase in subscribed seats to 31,134.

On the other hand, ALU has reported weak operating cash flow of US$14.1 million in FY 16 versus US$20.4 million in FY 15, which is affected by the termination of an onerous lease for US$1.5 million related to the relocation to the US last year as well as US$10.8 million build in receivables over the year 2016.

.png)

Financial Performance over the years (Source: Company Reports)

The tax paid has also jumped up to US$5.4 million from US$0.7 million that was paid last year. The group is forecasting >$100M revenue in FY17. ALU stock rose 43.98% in the last six months (as of October 07, 2016), and currently trading at a high P/E.

We give an “Expensive” recommendation on the stock at the current price of $8.83

ALU Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our

Terms & Conditions has been provided please go through them and also have a read of the

Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.