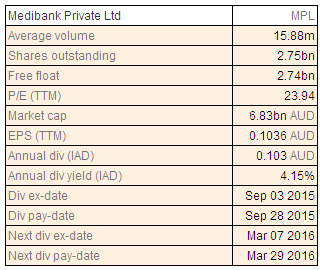

Medibank Private Ltd

MPL Dividend Details

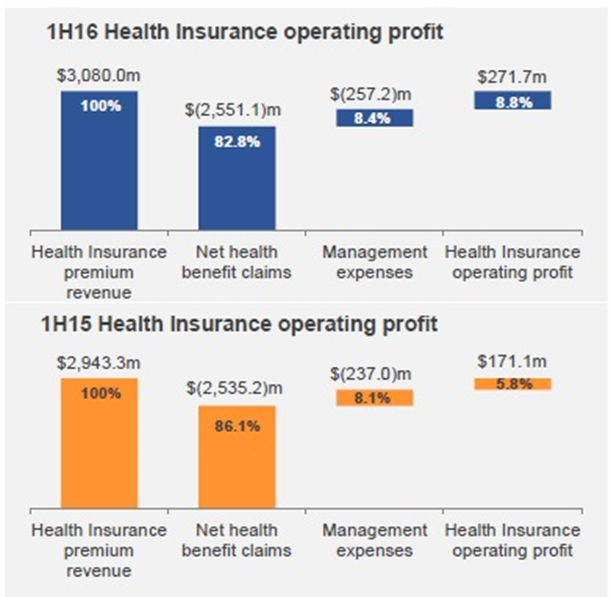

Strong financial results: Medibank Private Ltd (ASX: MPL) reported its first half financial year 2015 results with group net profit after tax of $227.6 million compared to $143.8 million in same period a year ago. This was mainly driven by improved profit from the health insurance business with operating profit of $271.7 million compared to $171.1 million in year ago.

Health insurance driving growth (Source: Company reports)

The board declared an interim dividend of 5 cents per share representing a first half dividend payout ratio of 64%. However, the Board remains committed to a full year target payout ratio of 70% to 75% of underlying NPAT. Looking ahead, for the health insurance business the board estimated premium revenue growth between 4.5% and 5%, management expense ratio of 8.5% and operating profit above $470 million. Having a solid dividend yield, we rate the stock "HOLD" at the current market price of $2.50

MPL Daily Chart (Source: Thomson Reuters)

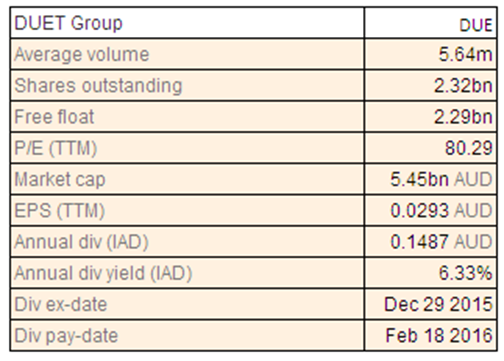

DUET Group

DUE Dividend Details

Rising revenue and profits: DUET Group (ASX: DUE) reported first half financial year 2015 group net profit after tax of $108.5 million compared to net loss after tax of $11.1 million in the same period a year ago. Revenues from ordinary activities stands at $809.7 million, an increase of 31.4% from same period a year ago. Net cash flow from operations increased to $403 million from $357 million in year ago period.

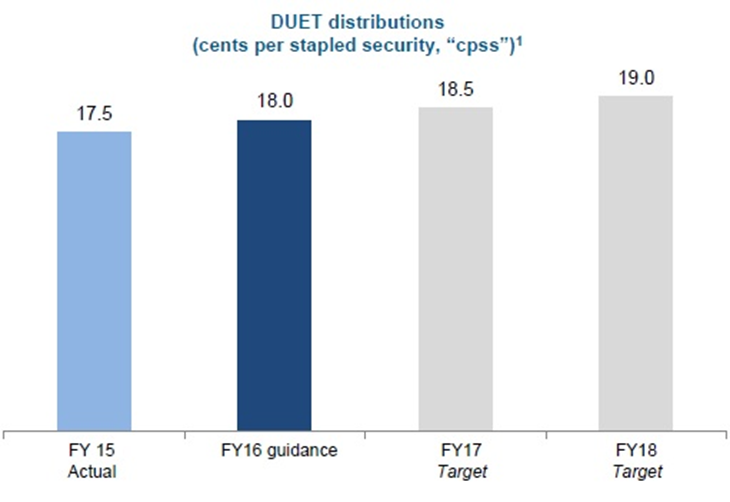

Dividend guidance (Source: Company reports)

For financial year 2016, distribution guidance stands at 18 cents per stapled security with 9 cents per share paid in February 2016. This guidance is expected to be fully covered by DUE's forecast operating cash flows. Duet group has a strong dividend yield, and we place a "HOLD" at the current share price of $2.28

DUE Daily Chart (Source: Thomson Reuters)

Automotive Group Holdings Ltd

.png)

AHG Dividend Details

Strong automotive growth driving profits: For the first half financial year 2015, Automotive Group Holdings Ltd (ASX: AHG) recorded operating net profit after tax of $49.4 million, an increase of 7.3% on prior comparable period. Driven by strong performance in automotive, the group recorded revenue of $2.75 billion, an increase of 7.2% on prior comparable period. AHG increased its interim dividend to 9.5 cents per share fully franked compared to 9 cents per share earlier, payable April 2016.

Management commented that they are confident of further growth in the Automotive division through targeted acquisitions and the continued performance of its existing dealerships. Further, 1.16 million new vehicle sales has been forecasted for Australia automotive industry in CY16, AHG foresees to maintain and grow its market share in new and used vehicles, and in service and parts. Based on the foregoing, we reiterate our "BUY" recommendation on this dividend yield stock at the current share price of $4.29

AHG Daily Chart (Source: Thomson Reuters)

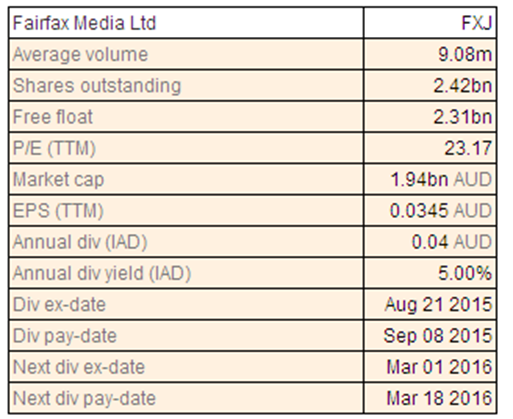

Fairfax Media Ltd

FXJ Dividend Details

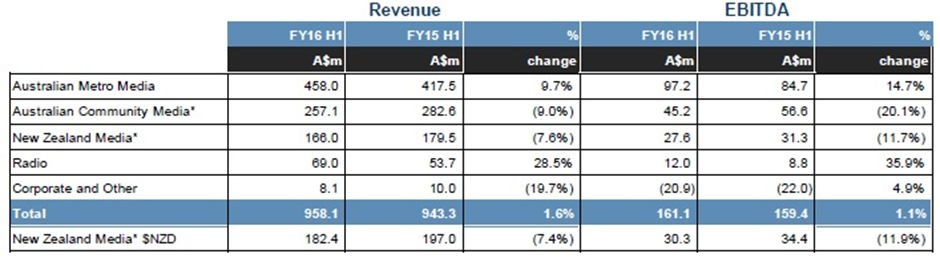

Cost reductions supporting revenue growth: Fairfax Media Ltd (ASX: FXJ)recorded group revenue for continuing operations of $958.1 million, an increase of 2.8% from the prior comparable period, for the first half financial year 2016. EBITDA was up 2% to $161.1 million for the same period. Net profit after tax stood at 79.8 million, dip of 2.2%. Led by continued focus on cost reduction and efficiency in publishing businesses, the group's publishing costs were down by 6% to $38 million.

Excluding significant items segment result (Source: Company reports)

Post its $111.8 million share buyback, FXJ reported net cash of $6.2 million. An interim dividend of 2 cents per share (50% franked) is to be paid in March 2016, a payout ratio of 59% of reported net profit for continuing businesses excluding significant items. With a strong dividend yield and rising revenue, we rate the stock "BUY" at the current share price of $0.775

.PNG)

FXJ Daily Chart (Source: Thomson Reuters)

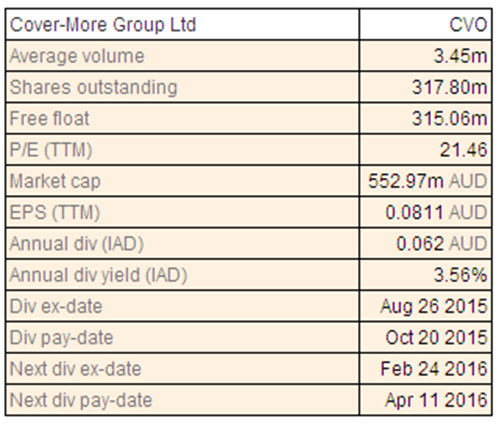

Cover-More Group Ltd

CVO Dividend Details

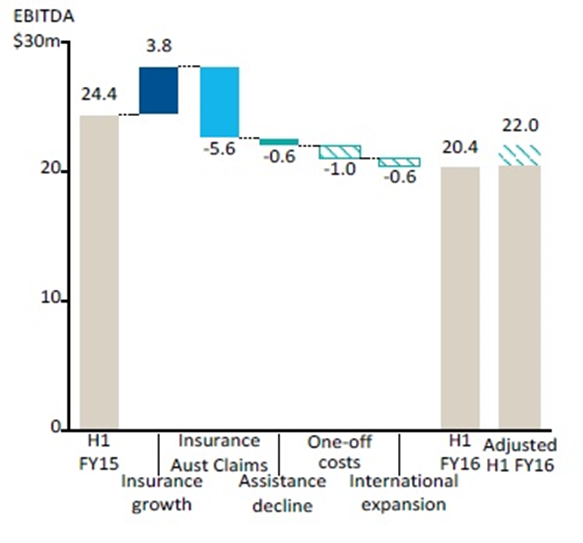

Outperformance in Australia and Asia: Cover-More Group Ltd (ASX: CVO)reported strong revenue growth of 6.6% on prior comparable period basis led by outperformance of Australia and Asian markets. Australian insurance segment revenue growth stood at 7.1% with conversion rates in key partners continuing to increase. EBITDA dipped 16.4% to $20.4 million mainly dented by increased underwriting premium payable due to higher claims costs.

EBITDA analysis (Source: Company reports)

Operating free cash flow before CAPEX stood at $18.8 million ($14.3 million after CAPEX) displaying strong conversion of EBITDA into cash flow. The Board declared an interim dividend of 2.1 cents per share fully franked, thereby totalling to 8.38 cents per share total cash return to investors. Given the growing Australian travel insurance business with continuing international business momentum, we rate the stock "BUY" at the current share price of $1.64

CVO Daily Chart (Source: Thomson Reuters)

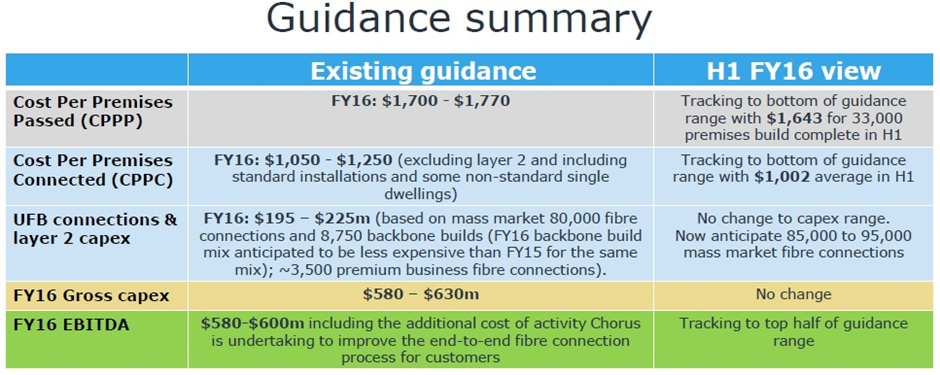

Chorus Ltd

Weaker fixed line but increased broadband connections: Chorus Ltd (ASX: CNU) reported first half financial year 2016 results with net profit after tax of $33 million compared to $64 million in the first half a year ago. EBITDA dipped to $275 million from $321 million. Total fixed line connections decreased by 33,000 connections from 1,794,000 to 1,761,000.

Guidance summary (Source: Company reports)

However, total broadband connections increased from 1,207,000 to 1,223,000 for the period, driven by the increase in demand for mass market fibre connections. For financial year 2016, CNU expects to pay a dividend of 20 cents per share with an interim dividend of 8 cents per share payable in April. Recently, Moody’s Investors Service has also upgraded CNU’s issuer and senior unsecured ratings to Baa2 from Baa3 with a stable outlook. Despite the above result but given a possibility of future potential, we rate this stock a "SPECULATIVE BUY" at the current share price of $3.57

CNU Daily Chart (Source: Thomson Reuters)

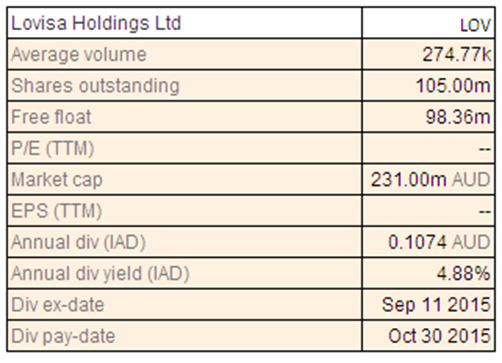

Lovisa Holdings Ltd

LOV Dividend Details

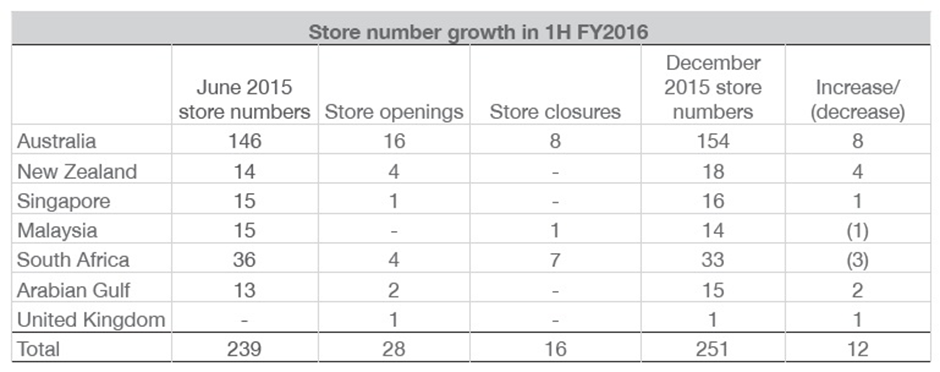

Store growth driving revenue and profits: Lovisa Holdings Ltd (ASX: LOV) recorded first half financial year 2016 revenue of $82.6 million, an increase of 13% from the year ago period. Store numbers for the period increased by 12 to 251 with a like-for-like sales growth of 4.1% on a constant currency basis. Net profit after tax increased 8% to $13.5 million.

Store growth statistics (Source: Company reports)

Strong balance sheet, solid cash flow and attractive growth opportunities drove the company to declare financial year 2016 interim dividend of 6.67 cents per share. Cash position increased by $6.2 million in the first half. Looking ahead, the company expects to generate full year 2016 Earnings before Interest and Tax in the range between $23.5 million and $25.5 million. With a good dividend yield and strong financials, we rate the stock a "BUY" at the current share price of $2.34

LOV Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.