SEEK Ltd

.png)

SEK Dividend Details

Record results & positive developments: For financial year 2015,Seek Ltd (ASX: SEK) reported record full year results and some major accomplishments highlighting company's growth across overseas markets. Despite global macroeconomic subdued conditions, SEEK achieved sales revenue growth of 20% and EBITDA growth of 15% from continuing operations, along with total dividends growth of 20% in FY15 over the previous year. In 2015 fiscal year, the company also recorded an average of more than 35 million monthly visits in domestic employment segment while through SEEK International there were more than 340 million visits and over 3 million job ads. SEK is a market leader in 14 countries across Australia, China, South East Asia and Latin America. In its full year 2015 results, Seek announced that it has decided to sell its entire 50% ownership in IDP Education for $332 million as the business is not in synergy with any of Seek group’s businesses. However, IDP investment proved beneficial for SEK with high dividends received, attractive post tax IRR, high cash return of original investment and establishment of credible participant in education sector.

.png)

Core drivers of earnings growth (Source: Company reports)

The company reaffirmed its guidance for financial year 2016 with reported revenue growth across SEEK group for FY16 vs FY15 expected to be in the range of 15% to 18% while EBITDA growth for the same is seen in the range of 5% to 8%. Underlying FY16 net profit after tax (excluding negative impact of early stage losses) is expected to be around $ 195 million. Seek expects to generate strong growth in cash flows in the upcoming year.

Also, Seek Ltd has deployed capital in some early stage opportunities like strengthening online marketplace, early stage international markets and introducing online education models into new markets. With strong shareholder returns and dividends, we give this stock a “HOLD” rating at the current share price of $13.99.

.png)

SEK Daily Chart (Source: Thomson Reuters)

Cabcharge Australia Ltd

.png)

CAB Dividend Details

Moderate financial results: For financial year 2015, Cabcharge Australia Ltd (ASX: CAB) reported record fleet growth in taxi services with total fleet standing at 7,259 cars an increase of 7.9% from previous year. There was a continued growth in taxi fares processed at $1,118 million, higher by 8.6%. Revenue for the year stood at $188 million compared to $197.3 million due to tariffs slash led by competitors’ moves. Net profit after tax stood at $46.5 million, a dip of 16.6%. Despite government regulations applying a 5% cap (inclusive of GST) on service fees for non-cash taxi payments impacting Cabcharge revenues, the company focuses on increased transactions, expanding capabilities in its payments technology and application expertise. In a challenging environment, Cabcharge is redefining itself through leveraging its leading proprietary technology and know-how in electronic contactless payments and App development and design by providing technology solutions and services both within and outside the traditional boundaries of the taxi and transport industry.

.png)

Profit after tax - Twelve month movement (Source: Company reports)

Despite, CAB trading at a low P/E ratio and decent dividend yield, the company’s revenues and earnings are under high pressure from competitors and recent legislative changes in taxi payments service fee. This makes it difficult for CAB to come back to growth levels. We thus rate the stock as "Expensive" at the current share price $2.92

CAB Daily Chart (Source: Thomson Reuters)

Downer EDI Ltd

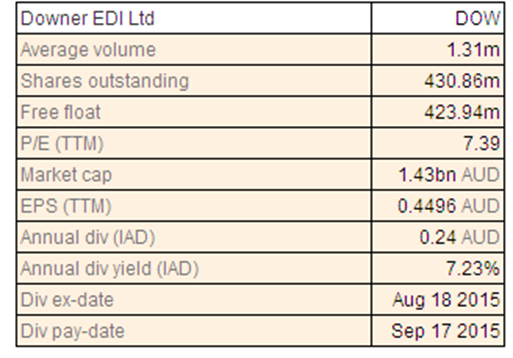

DOW Dividend Details

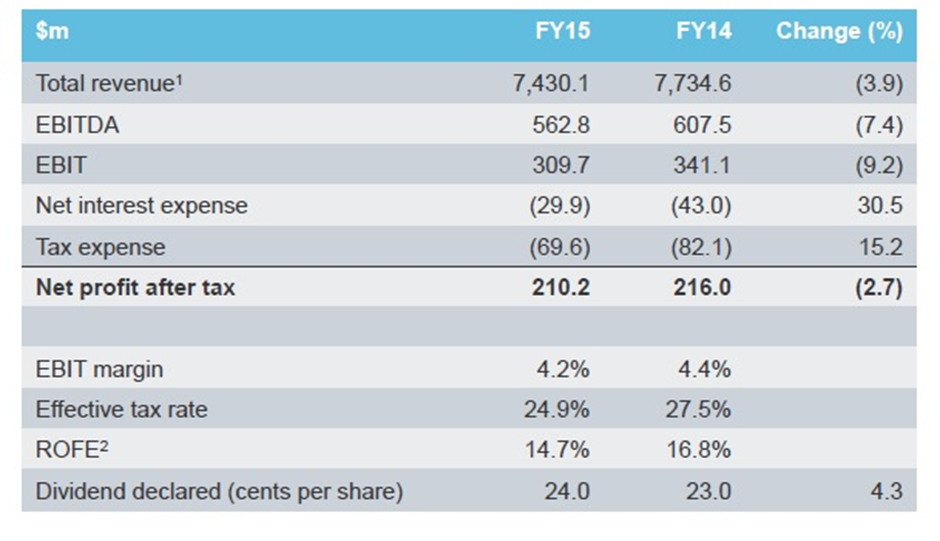

Positive developments: For the year 2015, Downer EDI Ltd (ASX: DOW) reported net profit after tax of $210.2 million, 2.7% lower than previous year while EBIT was also down 9.2%. Revenue was down 3.9% to $7,430.1 million. The company had strong performances from transport services and technology and communications services. During the year, Downer EDI was awarded an expanded contract with Fortescue Metals Group at Christmas Creek, a two year contract extension with BMA at Blackwater in Queensland and a two year contract for underground mining services at the Cobar copper mine in New South Wales. For the Rail business, DOW signed a 10 year, $1 billion locomotive maintenance agreement with Pacific National earlier during 2015 and also the company is tendering for two substantial passenger rail opportunities.

Financial Performance (Source: Company reports)

Downer is also in the early stages of bidding to supply 37 next generation, high-capacity trains for the Victorian government. This contract is expected to be awarded in late 2016. For the 2016 financial year, Downer is targeting NPAT of around $190 million. There is weakness and a high degree of uncertainty in a number of the company's end markets, particularly resources based construction and mining.

Downer comments that it will continue to build while investing in its existing businesses, including the major rolling stock and light rail opportunities. It looks to expand through well targeted acquisitions or joint ventures. With a mix of these developments, decent dividend yield and low P/E, we rate this stock a “BUY” at the current share price of $3.33.

DOW Daily Chart (Source: Thomson Reuters)

Mcmillan Shakespeare Ltd

.png)

MMS Dividend Details

Solid bottom line growth:For financial year 2015, Mcmillan Shakespeare Ltd (ASX: MMS) recorded consolidated net profit after tax of $67.5 million, a growth of 23% from previous year. It recorded annualised return on equity of 25% and return on capital employed of 24%. During the year, the company secured additional contracts from new clients with a good pipeline of new business extending into FY16.

Strong NPAT growth in FY15 (Source: Company reports)

Recently, MMS acquired 100% of the shares in the privately owned UK asset finance broker, Anglo Scottish Asset Finance for an upfront cash payment of £7.7 million and a potential earn-out payment of a maximum of £7.0 million based on the achievement of a three year cumulative EBITDA target up to 31 December 2018. Looking ahead, the company expects ongoing profitable growth and maintain industry leading service levels. Given the prospects, we rate this stock a “BUY” at the current share price of $12.31

MMS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.