SomnoMed Ltd

.png)

SOM Details

Outstanding Devices Performance driven by US and Europe markets: Somnomed Ltd (ASX: SOM) reported a strong revenue rise of 30.3% year on year (yoy) to $18.05 million in the first half of 2016 by the sale of SomnoDent devices. The US and Europe solid direct sales during the second quarter drove the quarterly MAS device revenues by 27.2% yoy to $9.8 million. SomnoDent devices global direct sales delivered outstanding performance in the second quarter leading to a surge by 21.3% as compared to the prior corresponding period (pcp). US Direct sales rose 22.1% during second quarter, and management estimates this positive momentum to continue even in the third quarter given a strong performance across all of its segments including dental and medical business. Even Europe delivered a positive performance, with the region’s volumes rising by 23.4% and 21.2% during second quarter of 2016 and first half of the financial year 2016, respectively. As a result, the Europe region’s share accounted over 36.9% of SomnoMed’s global business during the second quarter of 2016 while North America and APAC represented 54.5% and 8.6%, respectively, during the quarter. Sales from APAC improved by 11.1% and 8.7% in the first half of the financial year 2016 and second quarter of 2016 respectively. Meanwhile, the new signature line device, SomnoDent® Fusion is undergoing smooth transition while the new mid-price products are generating solid demand in the US markets. Products which were launched in second half of 2014, are representing over 36.1% of sales in the United States as of half year period to December 2015. Accordingly, management estimates that its current new line of products to continue to perform further in the coming periods. With the acquisition of Strong Dental, the group’s Canadian performance would also improve in the coming periods.

We believe that the recent stock correction of over 10.85% (as of February 02, 2016) in the last six months can be leveraged as an entry opportunity in the stock while we place a “Speculative Buy” recommendation at the current price of $2.62

SOM Daily Chart (Source: Thomson Reuters)

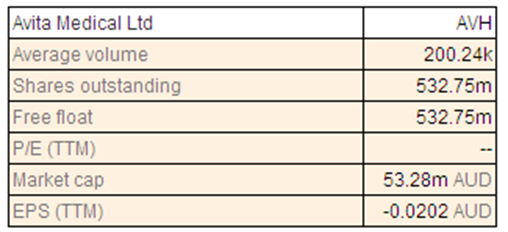

Avita Medical Ltd

AVH Details

Solid potential opportunity for the group’s ReCell®

device: Avita Medical Ltd (ASX: AVH) stock has rallied over 25% in last one year (as of February 02, 2016) driven by the improving prospects of its ReCell® device. The group recently signed distribution agreements in Japan and South Korea. The group would be signified by INDEE Medical in Japan which focuses on the regenerative medicine sector. With regards to the South Korea distribution, the group would be represented by TRM Korea which has expertise in distribution of several products related to wounds, aesthetics and reconstructive surgery for more than 25 years. Meanwhile, the group also finished the FDA patient recruitment for ReCell® Trial indicating an early regulatory approval in the US for ReCell®. FDA reported that ReCell® device might offer “major, clinically meaningful advantages” as compared to the present alternatives in the US for burns treatment indicating the strong opportunity ReCell® devices could have in the US. Moreover, the group reported that based on the results of a series of 12 cases, the duration of the hospital stay for patients with extensive burn injuries decreased by 63% after treating with ReCell®. The company’s second quarter results for FY16 indicated 17% rise in Total ReCell® for the first six months of fiscal 2016 over the previous year period with 9% drop in Respiratory sales for the first half of the fiscal year over last year while quarterly sales dipped by 1% compared to the second quarter of FY15.

Sales in France and Germany surged in the first half fiscal 2016 by 54% and 213%, respectively, over the earlier year; however, growth in UK sales could not be witnessed. AVH’s net operating cash out flow for the second quarter surged 11% over the previous quarter. Company reported cash on hand of AUD$7.7 million at end of the second quarter of FY16. On the other hand, we believe that the stock rally have placed AVH at higher valuations despite positive prospects. We give an “Expensive” recommendation to Avita at the moment and would review the stock at a later date.

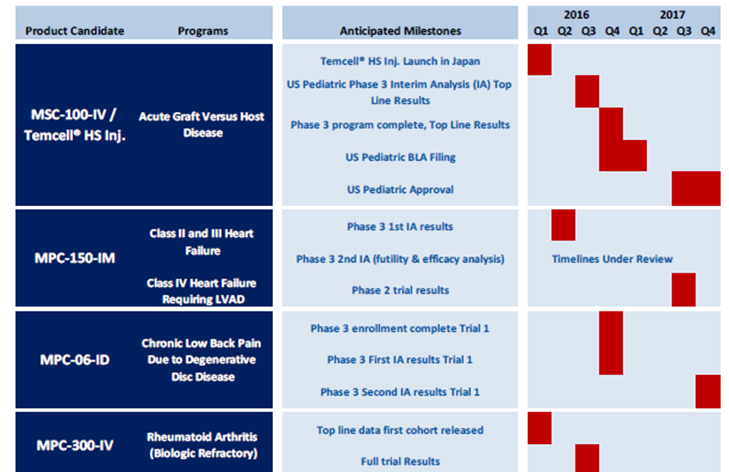

Mesoblast Ltd

.png)

MSB Details

Building strong pipeline: Mesoblast Ltd (ASX: MSB) stock was beaten down by over 63.17% in the last six months (as of February 02, 2016) due to lower than expected capital raising through its NASDAQ listing in November 2015 and MSB received net proceeds of $63.5 million via this issue. On the other hand, MSB is building a strong project pipeline during this year. The group reported a revenue increase to $7.5 million for the first quarter of 2016, against $7.0 million in the earlier corresponding period. MSB operational efficiency focus led to a decrease in loss after income tax by 15% to $13.2 million during the quarter against $15.5 million for the three months ended on September 30, 2014. Meanwhile, MSB recently reported that the size of its Phase 3 trial in chronic heart failure (CHF) of its proprietary cell-based medicine MPC-150-IM is estimated to be lowered.

Tier 1 Product Candidate Deliverables (Source: Company Reports)

MSB is also focusing on FDA filing for its first US Product approval in Acute Graft Versus Host Disease (aGVHD). MSB also forecasts results from its interim analysis of a Phase 3 trial of its product candidate for steroid refractory aGVHD. MSB forecasts a contribution from the first and second cohort in the Phase 2 trial of its product candidate for biologic-refractory rheumatoid arthritis in this year. MSB would launch TEMCELL® which is a mesenchymal stem cell product for aGVHD in Japan during first quarter of 2016. First interim analysis of safety and efficacy from its Phase 3 trial of product candidate for advanced chronic heart failure is expected in 1Q2016 with its partner, Teva Pharmaceutical.

The first Phase 3 trial of its product candidate for chronic low back pain on the back of degenerative disc disease is forecasted to be finished by third quarter of 2016. Cash flows related to operating activities for the quarter ended December 31, 2015 indicated cash of USD 120,783,000. Given the strong pipeline this year, the recent correction serves to be an opportunity to enter the stock and accordingly we give a “Buy” recommendation on the stock at the current price of $1.40.

MSB Daily Chart (Source: Thomson Reuters)

Virtus Health Ltd

.png)

VRT Dividend Details

Efforts to enhance volume growth: Virtus Health Ltd (ASX: VRT) stock surged 8.40% (as of February 02, 2016) during this year to date. Recently, the group reported that Singapore activity delivered only 20 cycles per month as compared to the group’s estimates of a volumeof 30 cycles per month. The group incurred over $1.9 million related to its clinic set up in Singapore. Singapore operations delivered an EBITDA loss of $206,000 during the first quarter of 2016. On the other hand, VRT delivered a rise of 6.6% in its fresh cycle activity in Australia which includes contribution from its acquisitions.

.png)

Operations overview (Source: Company Reports, as of October 2015 report)

Underlying Sims Clinic in Ireland rose by 10.2% as compared to the pcp. Since the Singapore operations are new, the performance might improve gradually despite short term pressures. VRT is also focusing on its diagnostics business which generated a double digit revenue growth since the last two years. The application of genetic testing delivered favorable success rates and consequently enabled ARS for more complex patients to deliver healthy babies.

We believe that investors need to leverage the recent correction as an entry opportunity. Virtus is also trading at a reasonable P/E and has a decent dividend yield. Accordingly, we recommend a “Buy” on Virtus at the current price of $6.27

VRT Daily Chart (Source: Thomson Reuters)

Sirtex Medical Ltd

.png)

SRX Dividend Details

Ongoing focus on SIR-Spheres microspheres while extending into Kidney products: Sirtex Medical Ltd (ASX: SRX) continues to focus on its core of SIR-Spheres microspheres and leverage its further potential opportunity. SIR-Spheres microspheres along with traditional chemotherapy was able to hold back further progression of liver tumors by an extra 7.9 months as compared to only chemotherapy, which is an enhancement of over 63% in patients with metastatic colorectal cancer. Sirtex Medical intends to expand its SIR-Spheres microspheres into major markets like China and Japan, as primary liver cancer in China is around ten times more than the incidence witnessed in the United States as per GLOBOCAN, indicating a huge potential opportunity for SRX. Meanwhile, the group delivered favorable progress across all of its five clinical studies during fiscal year of 2015. The group finished recruitment for FOXFIRE and FOXFIRE Global studies during January 2015 and finished recruiting for SARAH study in March 2015 with results forecasted by end of 2016. SORAMIC and SIRveNIB studies generated over 85% of recruitment in 2015 and the company expects to finish recruitment this year. The group would combine the overall survival data from the SIRFLOX clinical study with survival data from the FOXFIRE and FOXFIRE Global studies and expects the data to be available by 2017. On the other side, Sirtex Medical is also targeting Kidney products and accordingly focusing on the RESIRT pilot clinical study which would shortly complete the patient recruitment.

Sirtex dose sales as of 2015 (Source: Company Reports)

As per the stock performance highlights, SRX surged over 20.66% in the last six months (as of February 02, 2016) and we believe there is more upside to be witnessed. Based on the foregoing, we give a “Hold” recommendation for the stock at the current price of $36.43

SRX Daily Chart (Source: Thomson Reuters)

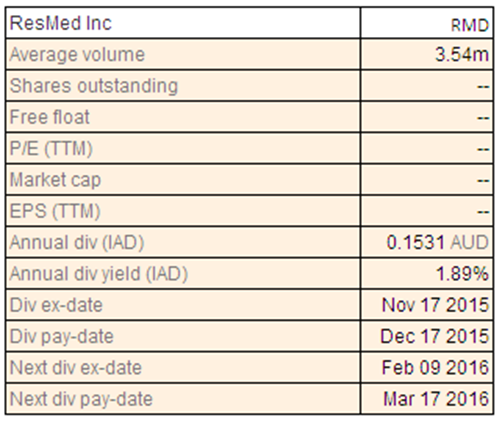

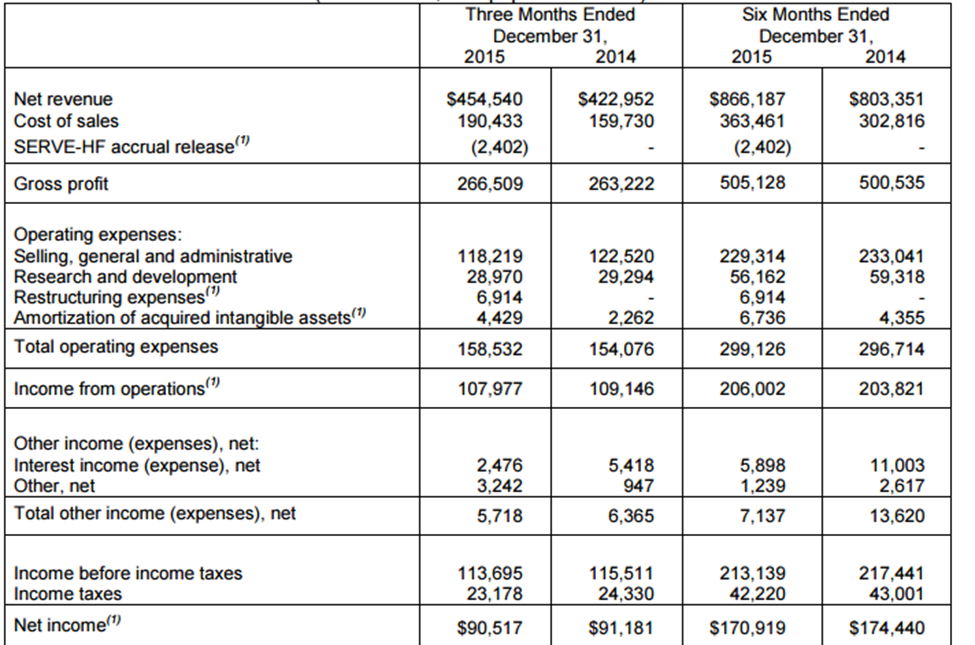

ResMed Inc

RMD Dividend Details

Major contribution from Americas Region: ResMed Inc. (CHESS) (ASX: RMD) reported a revenue increase of 7% yoy to $454.5 million during the second quarter of fiscal year of 2016, and a 13% rise on a constant currency basis driven by its solid respiratory care and sleep-disordered breathing business performance. RMD is also expanding its respiratory care business to long-term oxygen therapy and accordingly announced acquisition of Inova Labs in Austin at Texas to leverage Inova’s portable oxygen concentrators. These portable oxygen concentrators along with the group’s non-invasive ventilators would enable a better therapy option for patients with chronic obstructive pulmonary disease, or COPD. The Americas region revenues rose by 17% yoy to $269.5 million as customers preferred the group’s offerings like Air Solutions cloud-based software, AirSense devices, and AirFit patient interface systems.

Second quarter of 2016 performance (Source: Company Reports)

Meanwhile,

RMD delivered a Gross margin of 58.6% during second quarter driven by $2.4 million of one-time benefit from accrued expenses related to SERVE-HF field safety notice. However, gross margin decreased to 58.1% during the quarter without the one-time benefit on the back of decrease in average selling prices. Net income reduced by 1% to $90.5 million during the quarter as compared to the pcp. ResMed bought 700,000 shares at $40.1 million in the second quarter of 2016 and reported a quarterly dividend of $0.30 per share. However, we believe that the stock is “Expensive” at the current price.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.