Stocks’ Details

Commonwealth Bank of Australia

Traded at Reasonable PE Level: Commonwealth Bank of Australia (ASX: CBA) is a large-cap banking sector entity with the market capitalization of circa $122.09 Bn as of October 11, 2018. The group has recently announced its plan to initiate further improvement in its wealth management business. However, the highlight of the story was its review and redemption program. Over the past six years, CBA has spent around $580 million to improve its advice business processes, administering and assuring advice remediation and implementing its Future Advice Model. As per the release, the initiative involves such as taking action to remove certain fees on legacy wealth products from January 2019 which save customers approximately $25 million annually; rebating all grandfathered commissions to CFP customers from January 2019 which benefited around 50,000 customer accounts by approximately $20 million annually, etc. On the analysis front, net interest margin came in at 2.15% in FY18 which is above the Industry median of 1.94%. Its efficiency ratio, which measures the cost to the bank of each unit of revenue, has been maintained in the range of around 42% to 44% over the past few years while the industry average touches the figure of 52.0%; and as lower values are considered to be better because it signifies that the bank’s earnings are more than their spending, thus, CBA seems to be in a decent zone despite sectorial headwind ahead.

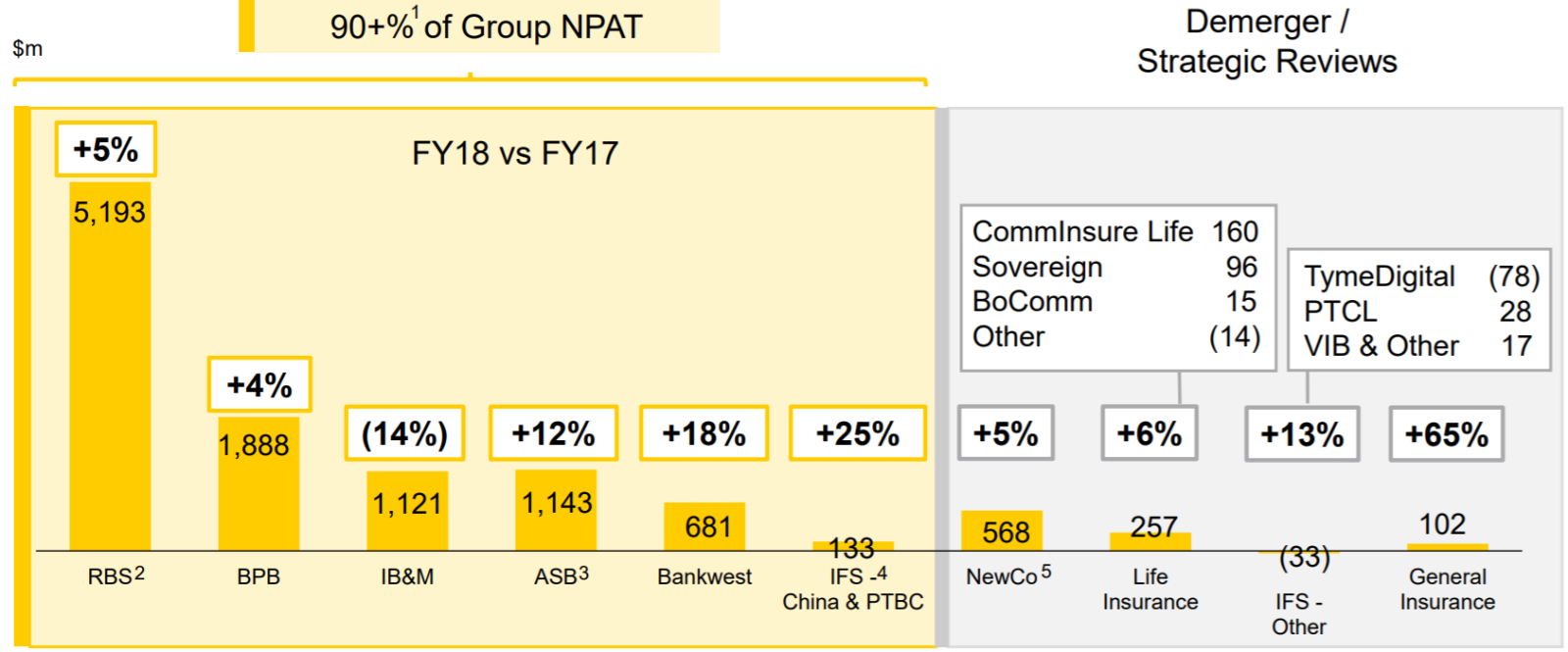

Good Contribution Across Portfolio (Source: Company Reports)

Moreover, the bank has recently released Promontory Australasia’s first independent report into the progress of CBA’s Remedial Action Planfor the purpose of strengthening governance, culture, accountability and customer outcome. Meanwhile, CBA has fallen 7.34% in past three months as on October 10, 2018 and is trading at a reasonable P/E of 12.91x. Moreover, the outlook for the Australian economy is positive with GDP growth expected to be around 2.7% for the remainder of 2018 and 2019. The Australian banking industry has performed well over the past decade, underpinned by favourable credit market conditions and stable economic conditions. CBA has historically posted strong total shareholder returns and has outperformed the Australian market and peer banks. Based on the foregoing and the prevailing low levels, we maintain our “Buy” recommendation on the stock at the current price of $67.00 (down 2.8% on October 11, 2018).

Westpac Banking Corporation

Decent Fundamentals: Westpac Banking Corporation’s (ASX: WBC) stock tumbled 2.557 per cent on October 11, 2018 on the back of negative market sentiment in relation to WBC’s CEO facing parliamentary questioning over misconduct. It is the first time where CEO of one of the biggest financial institutions in Australia is questioned about the misconduct by federal politicians at a parliamentary hearing in Canberra that was eventually uncovered by a royal commission. During the hearing, Westpac chief executive Brian Hartzer has admitted that the banks have their work cut out for them to regain the public's trust. Further, he accepted that WBC was too slow to grapple the customer issues, particularly in its financial advice services area. From analysis standpoint, its net interest margin for FY18 has slightly reduced to 2.06% compared to 2.10% in FY18 as compared to the prior year, due to higher funding costs and lower contribution from Group’s Treasury. WBC’s Common Equity Tier 1 (CET1) capital ratio of 10.4 percent as of 30 June 2018 marked a de-growth of 10 bps from March 2018. It was mainly impacted by the conversion of $566 Mn of preference shares to ordinary shares while it was offset by the determination of FY18 Dividend (net of DRP). In our view, heightened volatility, and risk aversion will continue in the Markets because of several factors such as trade tension, banking sector headwind, etc.

Common Equity Tier 1 Capital ratio (Source: Company Reports)

Meanwhile, the share has fallen 8.51 percent in the past three months as of October 10, 2018 and traded at a lower level. The bank has P/BV of 1.43x and beta of 1.33x as on 5-Year (monthly basis), signifying decent fundamentals at the current juncture. Hence, by looking at its fundamentals, stability, and capability to manage risks, we maintain our “Buy” recommendation on the stock at the current market price of $26.29.

Australia and New Zealand Banking Group Limited

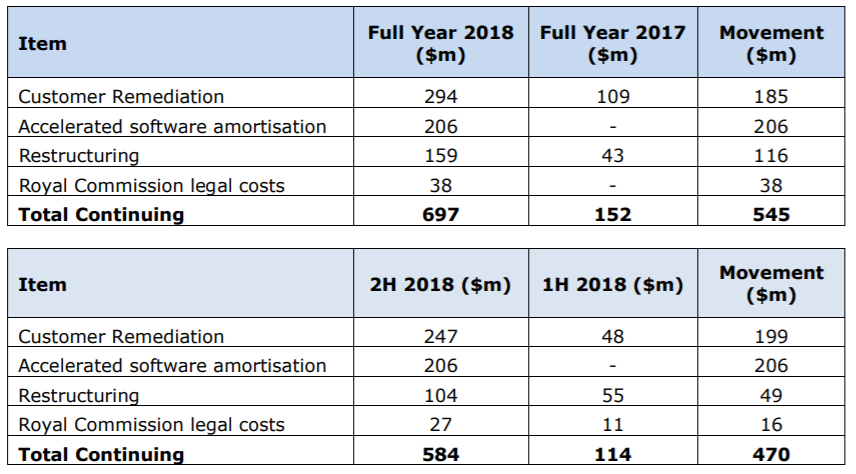

Strong Capital Position:Australia and New Zealand Banking Group Limited (ASX: ANZ) has recently announced a number of additional charges which will be recognized in its FY18 result. These further charges relate to software write-offs, restructuring costs, and legal costs for the royal commission. As per the release, these charges will have an impact of $697 Mn (post-tax) on profit from continuing operations and $127 Mn (post-tax) to be included in discontinued operations for the full year. These charges are: (1) customer remediation costs of $294 Mn in total, with $247 Mn included in continuing operations while $127 Mn will be reported in discontinued operations (the wealth business to be sold); (2) accelerated software amortisation of $206 Mn; (3) restructuring costs of $159 Mn, relating to the move towards agile ways of working; and (4) legal costs related to the royal commission of $38 Mn. However, the management believes that the impact of these additional charges on ANZ’s Common Equity Tier 1 capital position compared to 1H FY18 is expected to be less than 10 basis points. In our view, the bank has a strong capital position and the impact from these incremental charges looks to be manageable by the bank.

Estimated Impact to Continuing Operations profit after tax (Source: Company Reports)

Meanwhile, ANZ’s Common Equity Tier 1 (CET1) capital ratio of 11.07 percent as of 30 June 2018 marked a growth of 3 bps from March 2018. It was mainly driven by an organic capital generation of +50bps and receipt of reinsurance proceeds from the One Path Life (OPL) sale of +25bps while being offset by the FY18 Interim Dividend of -59bps and the share buyback of -8bps. From technical standpoints, the stock has generated YTD return of -5.95% owing to challenging environment and legal proceedings. However, the chart structure of the stock price looks strong as the long-term support level of $21.35 has been held on to. Among the indicators, RSI is near to oversold zone suggesting that the stock can revamp in near term as the stock is losing its bearish strength. Hence, we give our “Buy” rating on the stock at the current price of $ 26.010.

National Australia Bank Limited

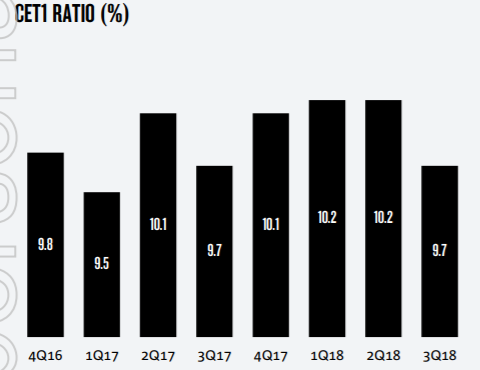

Traded at 52-Week Lower level: National Australia Bank Limited (ASX: NAB) has recently announced the distribution payment of AUD 1.20060000 with dividend distribution rate of 1.9295 % per annum for NABPD - CAP NOTE 3-BBSW+4.95% PERP NON-CUM RED T-07-22 and it will be paid on January 7, 2019 with the record date of December 28, 2018. Besides this, National Australia Bank Limited and its associated entities, a substantial holder of APN Outdoor Group Limited changed its holding from 8.081% of interest to 6.601% of the voting power. On the financial front, NAB delivered a Q3 FY18 CET1 ratio of around 9.7%, down by approximately 50 bps from 1H FY 18 at the back of interim 2018 dividend declaration (-63bps net of DRP) and seasonally stronger loan growth in the June quarter. Additionally, the bank has Liquidity Coverage Ratio of 132% as of June 30, 2018 and is well above the regulatory minimum of 100%.

CET1 Ratio Trend (Source: Company Reports)

Meanwhile, the share price has fallen 4.24% in the past three months as at October 10, 2018 and currently traded close to 52-week low level of $25.900. Hence, we maintain our “Hold” recommendation on the stock at the current market price of $ 26.00 as we await for better and stable growth drivers.

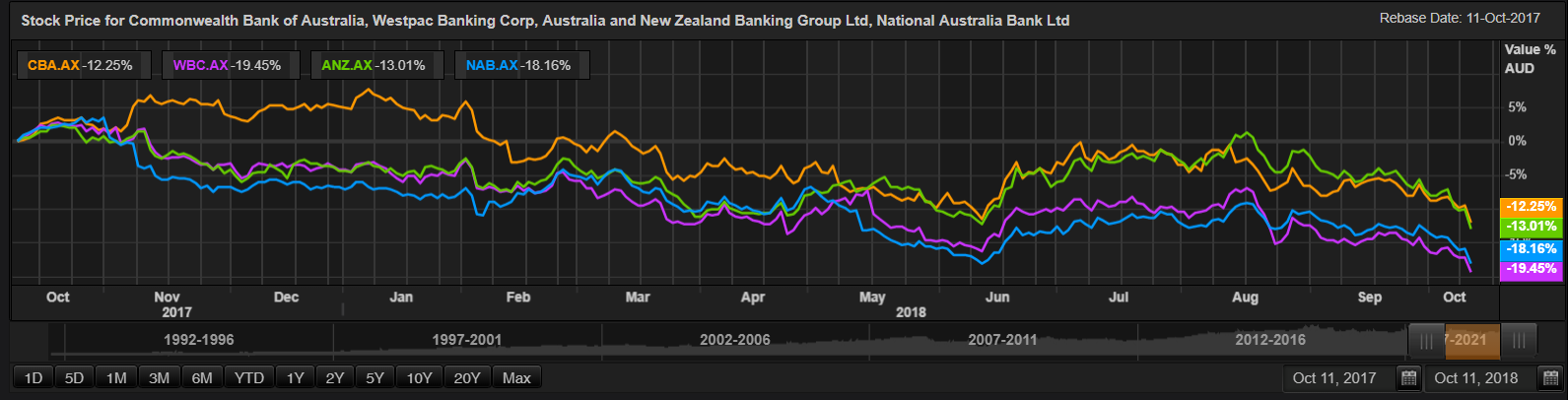

Comparative Price Movement (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...