Nearmap Ltd

.png)

NEA Details

US business performance at par with the expectations: Nearmap Ltd (ASX: NEA) was able to achieve an annualized contract value (ACV) of $1 million in the US market and delivered a subscription revenue of $0.2 million during first half of 2016. NEA had also successfully delivered an Australian ACV of $30M million, at par with its expectations driven by solid penetration across industries. The group’s Australian subscription revenue improved by 21% to $13.6 million during first half of 2016 as compared to $11.2 million in the prior corresponding period (pcp). Gross profit improved by 22% to $12.3 million in Australia during the period against $10.1 million in the first half of 2015.

.png)

First half of 2016 performance (Source: Company Reports)

Meanwhile, the group built a solid capital position having cash balance of $14.4 million and has no debt. Nearmap had developed a strong client base, and accordingly reported a 23% rise in its subscription revenues to $13.8 million.

The group invested $4.5 million in sales and marketing for its US markets, which would drive the region’s business in the coming periods. NEA’s next generation HyperCamera 2 technology launch in the second half of fiscal year of 2016 would also drive its performance further. We remain bullish on NEA and accordingly reiterate our “BUY” recommendation at the current price of $0.335

NEA Daily Chart (Source: Thomson Reuters)

IMF Bentham Ltd

.png)

IMF Dividend Details

Solid dividend yield: The shares of IMF Bentham Ltd (ASX: IMF) corrected more than 46.62% (as of February 22, 2016) in the last one year as the group lost many of the cases it funded during 2015, especially in the second half. But, investors need to note that IMF has a strong historical track record and accordingly settled and won 130 cases, out of a total of 175 cases since its listing (IMF withdrew over 35 cases and lost 10 cases out of these 175). Recently, the group is funding for a matter in the United States via its Bentham Capital subsidiary which has an initial claim value of $70 million. Another matter with an initial claim value of $47 million is reported to be funded in the US. Recently, the group is funding for a matter in the United States via its Bentham Capital subsidiary which has an initial claim value of $70 million. Management also reported that they are focusing to generate a future growth through their portfolio diversification strategy during the December quarter and implemented ten new funded matters. IMF’s European Joint Venture undertook three major funding matters which might lead to a rise in the portfolio claim value of over $200 million.

.png)

IMF Case Investment Portfolio as at 31 December 2015 (Source: Company Reports)

The group also reported that they are forecasting an average gross revenue of 15% of the portfolio value when the matters are finished. Meanwhile, the heavy correction also generated an outstanding dividend yield in the stock. We believe that IMF has the potential to recover from the current levels and accordingly give a “BUY” at the current price of $1.22

.PNG)

IMF Daily Chart (Source: Thomson Reuters)

AUB Group Ltd

.png)

AUB Dividend Details

Optimizing portfolio by making strategic acquisitions as well as divestments: AUB Group Ltd (ASX: AUB) recently offloaded its 50% share in Strathearn Insurance Group to Arthur J. Gallagher & Co. to focus on its core operations, which would contribute to the after tax profit of around $5.9 million and over 9 cents per share to the reported NPAT for the year.

The group intends to use the proceeds to repay its debt which would reduce its gearing ratio to over 17.5%. AUB is making efforts to optimize its portfolio and pursue growth opportunities and accordingly acquired Runacres and Associates Limited. Management reported that the collective result of the above two recent transactions would be positive, as well as enhance portfolio returns. Despite selling Strathearn Insurance Group stake, AUB reiterated the 5% rise in its adjusted NPAT for FY16 (excluding the realized cash profit). We believe that AUB stock is also trading at an attractive valuations with a reasonable P/E. Based on the foregoing, we give a “HOLD” recommendation on this dividend yield stock at the current price, ahead of its half year results to be released on February 25, 2016.

AUB Daily Chart (Source: Thomson Reuters)

Liquefied Natural Gas Ltd

.png)

LNG Details

Building contracts: Liquefied Natural Gas Ltd (ASX: LNG) recently reported that its subsidiary, Magnolia LNG made an agreement with Meridian LNG Holdings Corp for providing LNG of an annual capacity of 1.7 mtpa, while 0.3 mtpa additional capacity might be delivered based on Magnolia’s decision. The group made a 20 year agreement and has an option to extend for five more years. Moreover, Magnolia LNG even made a huge turnkey EPC contract with KBR lead KSJV, while the group has strategic alliance agreements with Siemens, Chart and EthosEnergy. The company has also reported for final authorization being issued by the US Department of Energy for Bear Head LNG to export LNG to Non-FTA countries.

.png)

Greater Magnolia LNG Project and greater Bear Head LNG Project (Source: Company Reports)

On the other hand, the shares of LNG had heavily corrected over 47.19% in the last three months (as of February 22, 2016) and over 73.71% in the last six months attributed to the ongoing decline of oil prices. But, we view this decline in the stock as an attractive opportunity to entry for investors seeking for long term value stocks, driven by the group’s long term agreements, strong cash position of $114 million (as of January 2016) and cost management initiatives. Based on the foregoing we give a “BUY” recommendation on the stock at the current price of $0.595

LNG Daily Chart (Source: Thomson Reuters)

Syrah Resources Ltd

.png)

SYR Details

Strong Marketing efforts for Balama Project: Syrah Resources Ltd (ASX: SYR) stock surged 13.13% (as of February 22, 2016) in the last three months as the group’s strong marketing efforts for its Balama Project have been paying off. As a result, Syrah entered into several agreements indicating strong prospects for the Balama Project and consequently to the group. Accordingly, the group entered into a Statement of Sales Intent with Hiller Carbon for buying and reselling 25,000 tpa to 35,000 tpa of Balama recarburiser only in the United States, Canada and Mexico regions. SYR earlier entered into a Statement of Sales Intent with a major refractory producer for ten years to deliver up to 15,000 tonnes per annum (tpa). Syrah Resources even made a Product Sales Agreement with Morgan Hairong to offer 2,000 tpa of uncoated spherical graphite.

The group entered into a three year marketing Agreement with Morgan Hairong to offer 5,000 tpa of uncoated spherical graphite as well as 2,000 tpa of coated spherical graphite. Meanwhile, Syrah Resources reiterated that its Balama Project progress is on track and even started the pre-stripping of the Balama West orebody. Based on the foregoing, we give a “HOLD” recommendation on the stock at the current price of $4.01

.PNG)

SYR Daily Chart (Source: Thomson Reuters)

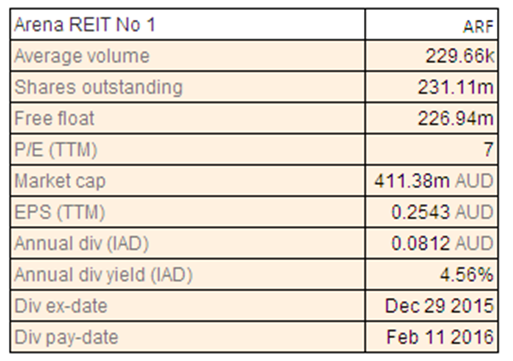

Arena REIT No 1

ARF Dividend Details

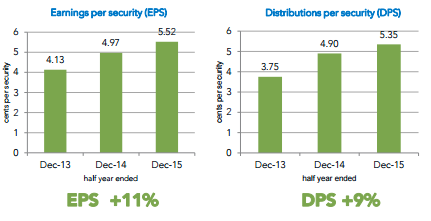

Solid performance: Arena REIT No 1 (ASX: ARF) reported an upgrade to FY16 distribution guidance to 10.9 cents a share indicating a 9% surge on previous year with half year distributable income per security of 5.52 cents, i.e., 11% on HY15. The company reported a 20% rise in net operating profit of $12.6m over HY15 while statutory profit of $41.4m surged 93%. This result was majorly driven by the strong property revaluations.

Earnings per security and Distributions per security (Source: Company reports)

With gearing reduced to 27.3% from 29.1%, the company has a solid business platform. We maintain our positive stance on ARF and rate the stock a “HOLD” at the current share price given the trading of the stock close to its 52-week high price.

ARF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...