Suncorp Group Ltd

.png)

SUN Details

New strategy and operating model to deliver growth: Suncorp Group Ltd (ASX: SUN) received storm claims in the range of $60-$80 million on account of East Coast storm impact. Suncorp Bank reported to have flat lending assets at $52.9 million while its impairment loss decreased to $4 million. Its gross non-performing assets are at $606 million. Retail lending was flat at $43.4 billion with 87% new loans written at an 80% or less loan to value ratio. For the first half of 2016, Suncorp reported 10% growth in earnings for bank while both general and life insurance reported drop of 29% and 39% respectively.

.png)

Approach to delivering value for customers (Source: Company Reports)

The group’s net profit fell 16% from $631 million to $530 million. The stock rose over 5.06% in the last four weeks (as of July 19, 2016) while the group announced for a provision for natural hazards and has an allowance of $670 million for FY16.

SUN reported an interim dividend of 30 cents and guided for dividend payout of 60%-80% of cash earnings. We believe that the bank’s new strategy and changes to its operating model would deliver cost efficiencies and enhance the company’s profitability in the future. The focus in new model is customer satisfaction which would help add more customers to the portfolio as well as improve retention level. We recommend a “Buy” on the stock at the current market price of $13.00

.PNG)

SUN Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

.png)

IAG Details

Issuance of unsecured subordinated convertible notes: Insurance Australia Group Ltd (ASX: IAG) estimates around $60-80 million net claim from East Coast low-pressure weather system. IAG expects to incur over $600 million net natural peril claim cost for FY16. IAG has given lower end of 14-16% insurance margin guidance. Meanwhile, IAG has recently issued an unsecured subordinated convertible notes worth NZ$350 million. The margin has been set at 2.6% giving fixed interest rate until the first optional redemption date (15 June 2022) of 5.15% per annum. On the other side, IAG is also a good dividend player. The company had delivered interim dividend of 13 cents and special dividend of 10 cents.

The company has dividend reinvestment plan (DRP) according to which interim and special dividends would be operated by acquiring shares on market without any discount. Market speculates IAG to come up with a sizeable share buyback plan with its fiscal 2016 result. IAG has been surging over 18.17% in the last six months (as of July 19, 2016) and we maintain a “Buy” on the stock at the current market price of $5.85

.PNG)

IAG Daily Chart (Source: Thomson Reuters)

AMP Ltd

.png)

AMP Details

Weak first quarter results:AMP Ltd (ASX: AMP) reported an overall AUM of $112.6 billion in the first quarter of 2016, down 2% from fourth quarter of FY15. Retail and corporate superannuation net cash flows on AMP platforms were $383 million in Q1FY16 while wrap platform resulted into net cash flows of $820 million, down 11% from Q1FY15. AMP’s flexible super reported cash flow of $84million down from $347 million in Q1FY15.

Corporate superannuation net cash flows were at $109 million and external platform had cash flows of $174 million. AMP’s wealth protection business is being impacted by claims experience losses of $18 million, which is softening the cash flows in Australian wealth management business. We give an “Expensive” recommendation on the stock at the current market price of $5.77

AMP Daily Chart (Source: Thomson Reuters)

QBE Insurance Group Ltd

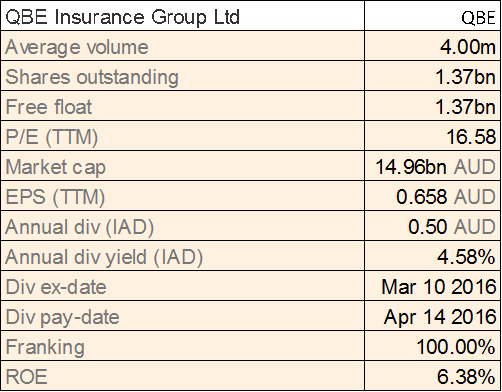

QBE Details

Brexit outcome impacted stock sentiment: The shares of QBE Insurance Group Ltd (ASX: QBE) plunged over 8.76% in the last four weeks (as of July 19, 2016) impacted by the Brexit outcome. The group reported that they might need to have a revised approach with regard to its GBP500 million insurance and reinsurance premium from EU member countries. With the Brexit outcome, QBE might have to renew this business into newly established licensed EU entities. On the other side, QBE issued US$ 524,124,000 of new notes to HSBC, bearing 5.875% p.a. interest.

QBE had also issued subordinated notes with interest of 6.5% for the first interest payments and the same will be reset for subsequent interest period at mid-market swap rate plus margin of 5%. However, we believe that the stock would continue to face pressure due to weak investor’s sentiment. Based on the foregoing, we give an “Expensive” recommendation at the current market price of $10.96

QBE Daily Chart (Source: Thomson Reuters)

Pepper Group Ltd

.png)

PEP Details

Investing in long-term growth: Pepper Group Ltd (ASX: PEP) reported a better than estimated NPAT of $48.6 million in CY15 against prospectus guidance of $47 million for the full year. Even, assets under management (AUM) were up 59% to $45.5 billion by CY15 ahead of prospectus forecast. PEP reported $44.4 billion of AUM as at March 31, 2016. The Group has invested into auto finance in Australia, began residential lending in the UK and picked up 12% stake in Hong Kong and Shenzhen consumer finance as well as invested in Travel Service and York Capital, China. The contract with the large Lloyds Banking Group would add close to $9 billion in AUM in 2016. The loan portfolio increased to $1.86 billion while lending income surged 27% to $105.9 million. In 2016, the company has launched Pepper Money as a lending brand used for all direct and B2B activities. The Group has also invested $25 million into new lending platforms in past three years, which would drive business in coming period. The group guided for NPAT of ~$59 million for CY16. On the other side, in March 2016, the company has completed $400 million whole loan sale transaction.

.png)

PEP’s presence across the world (Source: Company Reports)

Furthermore, Pepper Group has committed US$1.25 million in equity funding to the US based global innovation network 1776. Innovation network 1776 would support startup business and through this investment, Pepper would gain access to new and innovative ideas from range of industries. We give a “Speculative Buy” on the stock at the current market price of $2.40

PEP Daily Chart (Source: Thomson Reuters)

Macquarie Group Ltd

.png)

MQG Details

Currency movements could impact the stock sentiment: Macquarie Group Ltd (ASX: MQG) stock fell over 2.85% (as of July 19, 2016) in the last four weeks on the back of softness in investor’s sentiment due to Brexit impact. The group’s performance seems to be impacted by the ongoing turmoil in the global markets coupled with unfavorable movements in the currencies.

On the other side, MQG announced that they have made consortium acquisition of Onthehouse Holding Ltd for cash consideration of $0.85 per share. In June, the group has issued 1,828 fully paid ordinary shares at a price of $73.27 each upon exercise of deferred share units, and 5,663 and 944 fully paid ordinary shares at a price of $80.30 each on retraction of 7000 exchangeable shares, and 9,438 fully paid ordinary shares at a price of $50.80 each on retraction of 10,000 exchangeable shares. However, we believe that MQG stock sentiment would continue to be under pressure in the coming months due to ongoing market conditions. We rate the stock as “Expensive” at the current market price of $73.24

MQG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...