Sydney Airport

.JPG)

SYD Details

Strong half year result and upgrade in distribution: Sydney Airport (ASX: SYD) witnessed a stock price surge of 3.4% on August 22, 2017 as the group released its half year 2017 results. The group reported a 4% growth in interim net profit to $167 million from $160 million of prior corresponding period (pcp) while earnings before interest tax depreciation and amortisation (EBITDA) jumped up 7.7% in the six months. Revenue also surged to $714.2 million from $661.9 million, indicating a 7.9% rise. Group’s revenues found support from stronger aeronautical revenues and retail sales and better revenues from property and car parking. The group also reported a strong inbound growth of 10% over pcp over a rolling 12-months at the back of growth from Asia.

.png)

Operational Growth (Source: Company Reports)

SYD has now indicated for increased confidence in its business outlook and raised its full-year dividend guidance. The 2017 dividend is now forecasted to be of the order of 34.5 cents per share, against the previous guidance of 33.5 cents per share. This is nonetheless subject to aviation industry shocks and forecast changes. Going forward, the group expects to get a revenue boost from its new Mantra hotel and the acquisition of an Ibis airport hotel. The stock has risen 13.22% this year to date (as at August 21, 2017) and looks to be slightly on the higher side. We maintain our “Expensive” recommendation at the current price of $ 7.08

.png)

SYD Daily Chart (Source: Thomson Reuters)

MG Unit Trust

.JPG)

MGC Details

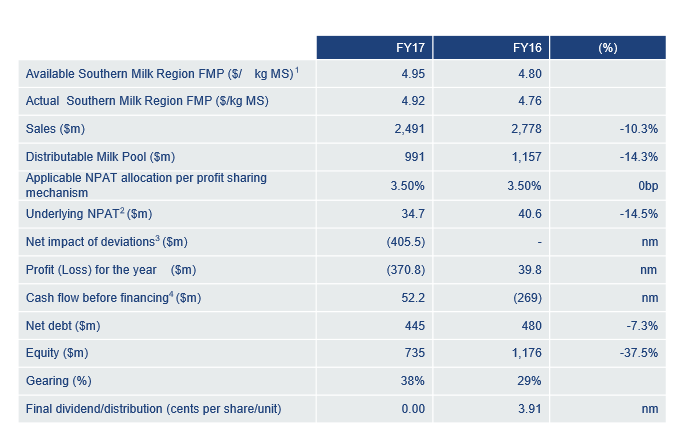

Challenging year at the back of lower milk intake and seasonal changes: MG Unit Trust (ASX: MGC) reported that Murray Goulburn Co-operative (MG), Australia’s biggest dairy processor, has announced financial results for the full year ended 30 June 2017 with $370.8 million of loss from profit of $39.8 million of FY16 at the back of many write-downs. Revenue was of the order of $2.491 billion, down 10.3% from $2.778 billion of last year. Material impairments led MG’s gearing level go up to 37.7% from 29% in FY2016. However, the net debt after cash reduced by $35m to $445m. The group also reported that there was a 21.8% drop in milk volumes to 2.7 billion litres. Overall, the result was impacted by milk intake and adverse seasonal conditions. In fact, milk supply is further expected to drop in the current financial year to about 2 billion litres. MG still aims to maintain its opening farmgate milk at $5.20 per kilogram of milk solids for the 2017/18 season. The group has not declared any final dividend against the 3.91 cents per unit paid last year.

FY17 Results (Source: Company Reports)

Given the scenario, the group has initiated a strategic review of the business and aims to now focus on manufacturing footprint, de-recognising the contentious Milk Supply Support Package (MSSP), and delivering on previously announced cost out initiatives. The group has also cancelled major capital projects. It will be prudent to watch how MGC recoups from the current challenging scenario. We give an “Expensive” recommendation at the current price of $ 0.64

.png)

MGC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...