.png)

Stocks’ Details

Elders Limited

Diversified Business Model: Elders Limited (ASX: ELD) is involved in providing retail products, livestock and wool agency services, financial and digital and technical services to rural and regional customers. As on 4 May 2020, the market capitalization of the company stood at $1.35 billion. In FY19, Elders Limited delivered on its earnings guidance, recording an underlying Earnings Before Interest and Tax of $73.7 million and an underlying after-tax profit of $63.6 million. The strength of these results is attributed to diversified business model of the company, along with the highly disciplined approach of the management to allocate costs and capital.

.png)

FY19 Financial Highlights (Source: Company Reports)

Future Expectations and Growth Opportunities: The company is focused on meeting its strategic targets. It will continue to grow its business organically and also through disciplined acquisitions which will allow the company to meet its strict financial criteria, ensuring value creation for shareholders. ELD seeks to expand its technical and digital services. The company is targeting quality growth of 5-10% p.a. while maintaining a return on capital between 15-18%.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

.png)

Price to Earnings Multiple Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of ELD gave a return of 39.23% in the past one year and a return of 10.05% in the last one month. The stock is also trading very close to its 52-week’ high level of $9.100. The company will announce its half-year results on 18 May 2020. During FY19, gross margin of the company stood at 20.7% as compared to the industry median of 40.2%. Considering the high returns, trading levels, and growth targets, we have valued the stock using price to earnings multiple approach and have arrived at a downside of lower double-digit (in percentage terms). For the said purposes, we have considered Select Harvests Ltd (ASX: SHV), United Malt Group Ltd (ASX: UMG) and Inghams Group Ltd (ASX: ING) as peers. Hence, we suggest investors to book profits and give a “Sell” recommendation on the stock at $9.070, up by 4.855% on 4 May 2020.

Afterpay Limited

Accelerated Growth in the US And UK: Afterpay Limited (ASX: APT) provides technology-driven payments solutions for consumers and businesses through its Afterpay and Pay Now services and businesses. As on 4th May 2020, the market capitalization of the company stood at $7.78 billion. During the quarter ended 31 March 2020, underlying sales of the company witnessed an increase of 97% and stood at $2.6 billion with active customers of 8.4 million. In the same time span, the company had 48.4k global active merchants and reported net transaction margin of approximately 2% on the YTD basis. This was mainly due to accelerated growth in the US and UK.

.png)

Quarterly Operating Highlights (Source: Company Reports)

What to Expect: The government enforced lockdown has resulted in moderation of underlying sales across the various regions. The company, however, is on track to achieve its objective of 9.5 million customers by 30 June 2020.

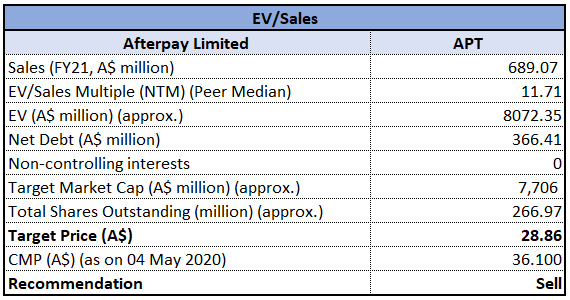

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The unprecedented circumstances from the breakout of COVID-19 are causing significant concerns in financial markets and APT has not been immune to these market concerns. This is evident from the volatility in its share price over recent weeks. However, it is managing its losses in real time by identifying leading indicators early. As per ASX, the stock of APT gave a return of 6.23% in the past six months and a return of 41.14% in the last one month. The stock is also trading very close to its 52-weeks’ high level of $41.14. During 1H20, gross margin of the company was in line with the industry median and stood at 74.8%. Considering the uncertain environment, high returns in the past six months and trading levels, we have valued the stock using EV/Sales based illustrative multiple approach and have arrived at a downside of lower double-digit (in percentage terms). For the said purposes, we have considered Perpetual Ltd (ASX: PPT), WiseTech Global Ltd (ASX: WTC), Challenger Ltd (ASX: CGF) etc. as peers. Hence, we suggest investors to book profit and recommend a “Sell” rating on the stock at the current market price of $36.1, up by 23.8% on 4 May 2020.

Family Insights Group Limited

Reduction in Cash Burn: Family Insights Group Limited (ASX: FAM) is a developer of software technology that delivers customized algorithms that enable the recreation of data flow between two geographical points. As on 4 May 2020, the market capitalization of the company stood at $2.44 million. The company has recently announced that its frugl grocery comparison application is market-ready and the company is likely to experience surge in online grocery scales. During the quarter ended 31 March 2020, the company witnessed a decline in monthly operational expenditure by approximately $93,000 per month.

During 1H20, the company reported a net loss of $432k on the revenue of $853k. In the same time span, the group had negative cash flows from operating activities of $544k.

.png)

1H20 Financial Highlights (Source: Company Reports)

Future Expectations: The company is currently developing two major features for the next release of the frugl grocery comparison app. It has also undertaken a structure to reduce its costs base.

Stock Recommendation: As per ASX, the stock of FAM gave a negative return of 31.48% on the YTD basis but a positive return in the past one month. During 1H20, the EBITDA margin of the company was substantially lower than the industry margin. In the same time span, the current ratio of the company stood at 1.18x, as compared to the industry median of 1.72x. Considering the volatility in returns, uncertain financial markets and decline in financial metrics, we recommend a ‘Sell’ rating on the stock at the current market price of $0.037 on 4 May 2020.

Sportshero Limited

Quarterly Update: Sportshero Limited (ASX: SHO) is a gamified social sports prediction platform where users can predict, interact, and compete on major sports virtually and in real-time. As on 4 May 2020, the market capitalization of the company stood at $8.53 million. During the quarter ended 31 March 2020, the company reported a reduction of $1,000,000 pa in operating expenses and undertook upgrades to the Kita Garuda apps e-store site.

H1FY20 results Highlights: During 1H20, the revenue of the company took a major hit and stood at US$1,151 and reported a loss of US$842k. This was mainly due to a conservative accounting stance and all development expenditure of the half year has been expensed. In the same time span, the company reported a strong balance sheet with an increase in cash balance to US$517k and a growth in total assets to US$734k.

.png)

1H20 Financial Position (Source: Company Reports)

Stock Recommendation: As per ASX, the stock of SHO gave a negative return of 16.13% on the YTD basis and is trading close to its 52-week’ low level of $0.003. The outspread of COVID-19 has resulted in all sporting fixtures being suspended. During 1H20, EBITDA margin and net margin of the company witnessed a substantial decline over the previous half. Considering the negative returns, trading levels and suspension of sporting activities, we recommend a ‘Sell’ rating on the stock at the current market price of $0.026 on 4 May 2020.

Comparative Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...