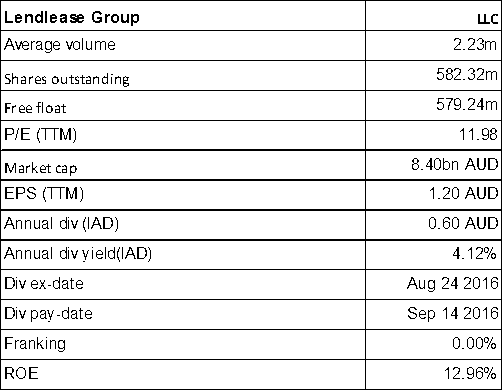

Lendlease Group

LLC Details

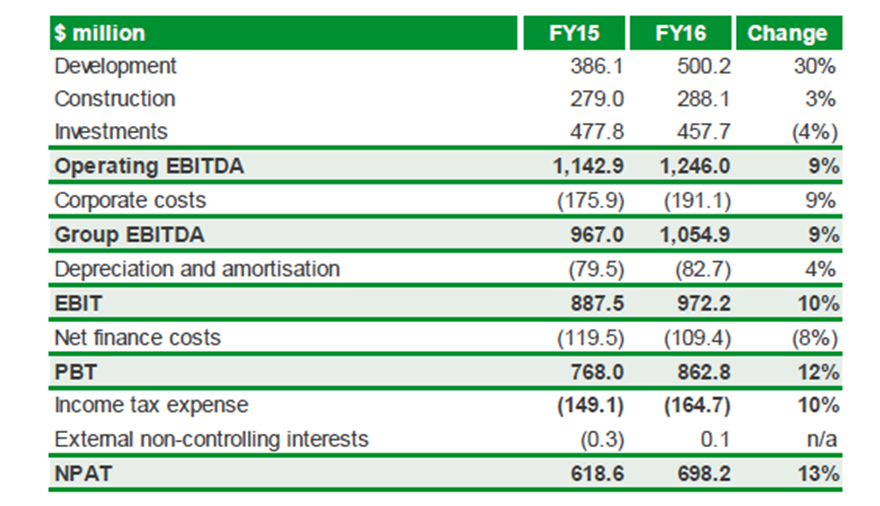

Strong backlog growth: Lendlease Group (ASX: LLC) reported a solid pre sold residential revenue rise of 13% to $5.9 billion for fiscal year of 2016, while the Construction backlog revenue improved by 20% to $20.7 billion. The group’s Funds under Management enhanced by 11% to $23.6 billion and created a $400 million managed investment vehicle. LLC was able to build a Development pipeline growth of 9% to $48.8 billion, despite tough market conditions indicating their expertise. Meanwhile, LLC reported an EPS growth of 120 cents, up by 12% while ROE rose 13%. LLC also declared that their final dividend of 60 cents would be distributed in September 16, 2016.

Key Metrics of LLC annual Results 2016 (Source: Company Reports)

Moreover, the group enhanced their operating cash flow to an inflow of $853m which was achieved by settlement on the first wave of apartment project completions and also from proceeds received on Tower Two and Tower Three at Barangaroo South in Sydney following completion. During the year, group partially disposed off their units in Lend Lease One International Sydney Trust.

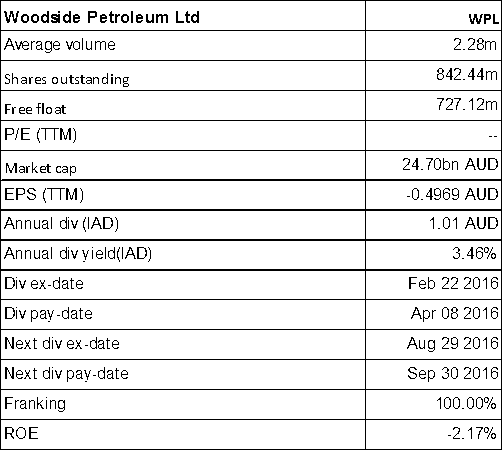

Woodside Petroleum Limited

WPL Details

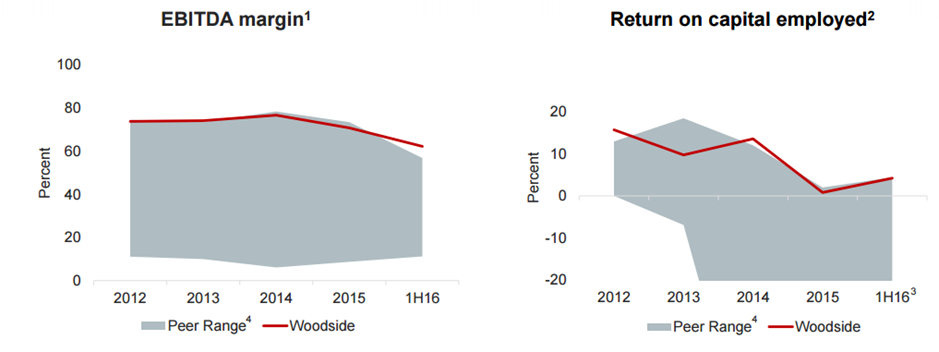

Controlling costs: Woodside Petroleum Limited (ASX: WPL) came up with solid performance in half yearly result. The group reported a production growth of 9% while controlled the unit production costs which fell over 38% as compared to the prior corresponding period. WPL also declared an interim dividend of 34 cents per share. The group agreed to acquire ConocooPhillips Senegal B.V which holds 35% of interest in 560 MMbbl SNE deep water oil discoveries.

WPL peer competitiveness (Source: Company Reports)

WPL also increased cash flow from operating activities of US$1.1b up by $4% from1H of FY15. Moreover, WPL has discovered 2.4Tcf of recoverable gas from uninterrupted discoveries in Myanmar. The group got Greater Enfield Project approval and is developing 2P oil reserves of 41 MMbbl.

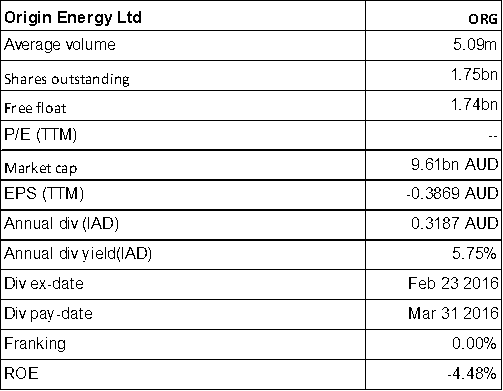

Origin Energy Ltd

ORG Details

Boosted capital position: Origin Energy Ltd (ASX: ORG) underlying profit from its operations decreased by 41% on year on year (yoy) basis to $354m. In FY16, ORG reported statutory loss of $589m from total operations. This decline is mainly due to $322 million upstream impairment in the second half coupled with $51 million reversal of prior impairment for geothermal interests (following sale of Origin’s interest in OTP).

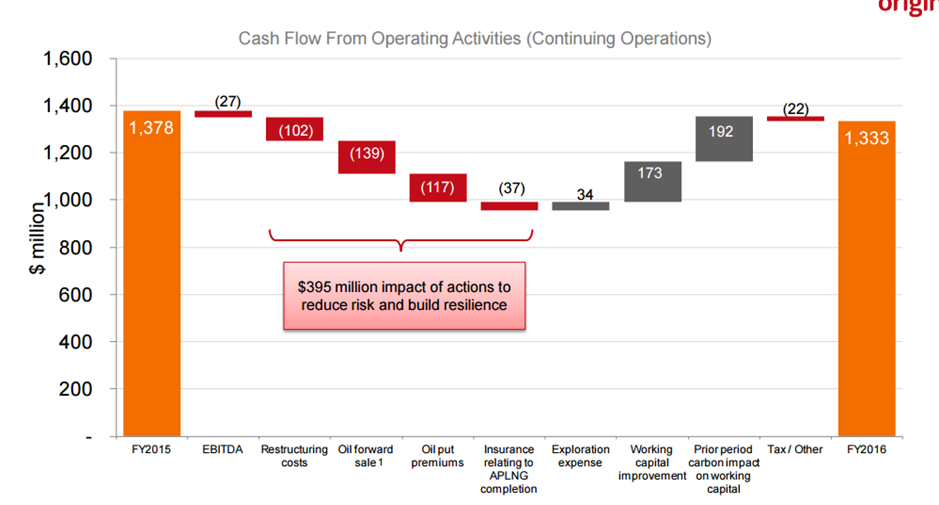

Cash flow performance (Source: Company Report)

On the other hand, the group enhanced cash flows while controlled their adjusted net debt from $9.1b to $4b. Origin’s conventional 2P reserves enhanced 111 PJe net of production of 74 PJe while downward revisions of 102 PJe were on the back of revised development plans in Cooper Basin and due to the impact of performance data for Otway and Bass basins.

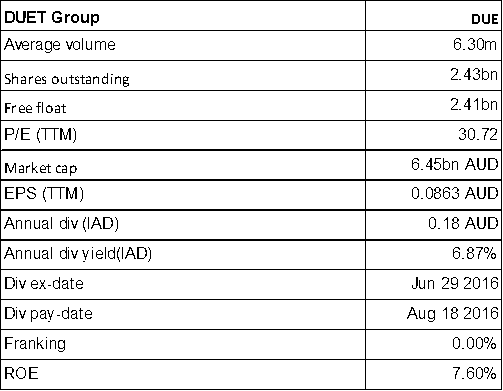

DUET Group

DUE Details

Strong results with proportionate earnings: DUET Group (ASX: DUE) reported an increase in earnings by 35.4% on yoy basis to $ 476.3 million for FY16. Revenue from ordinary activities surged 29.1% while NPAT excluding significant items grew 153.5%. The group is planning to expand after successful integration of EDL. United Energy network performance has been improving while business transformation project is underway at United Energy and Multinet Gas. Meanwhile, the group raised over $1.92b of equity to fund EDL and DBP acquisitions. The group delivered 18.0 cpss FY16 distribution guidance while expects over 18.5 cpss distribution for FY17.

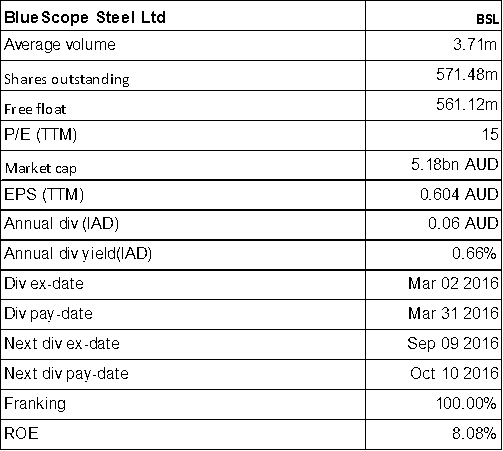

BlueScope Steel Ltd

BSL Details

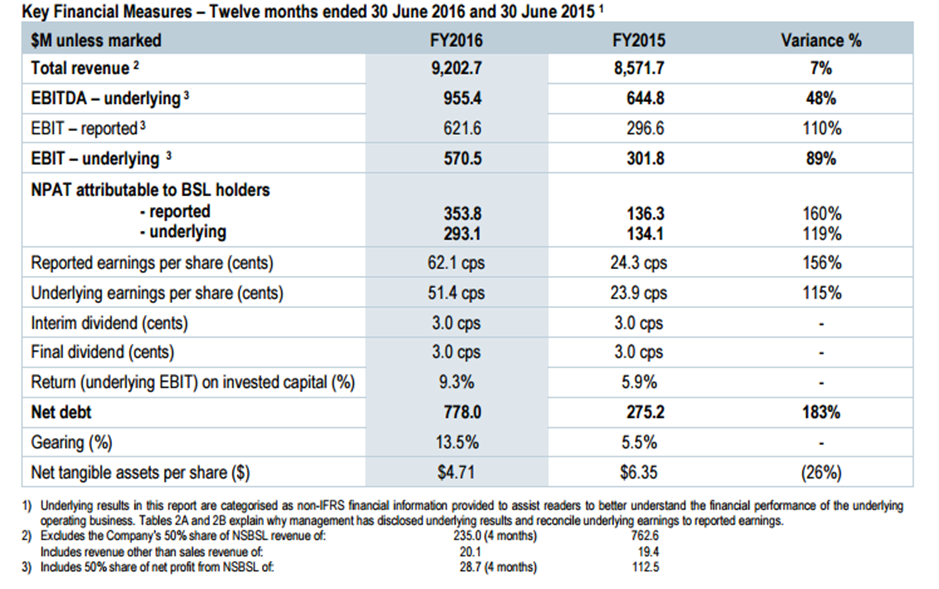

Solid bottom line growth: BlueScope Steel Limited (ASX: BSL) reported NPAT surge over 160% to $353.8million while underlying NPAT grew by 119% to $293.1m. Underlying EBIT grew by 89% to $570.5m which was achieved by combination of sales growth, cost reduction and recent acquisition of North Star. Sales revenue rose 7% yoy to $9,182.7m driven by 100% ownership of North Star from the end of October 2015 on the back of favourable impacts of a weaker AUD exchange rate and better domestic demand within Australian Steel Products.

BSL Results summary (Source: Company Report)

BSL has also decreased debt of group from $778m to $595.4m in FY16. The group declared for fully franked dividend of 3 cents per share. BSL forecasts EBIT to be over 50% higher in the first half of 2017 as compared to the second half of 2016 which was $340.4M.

Northern Star Resources Ltd

NST Details

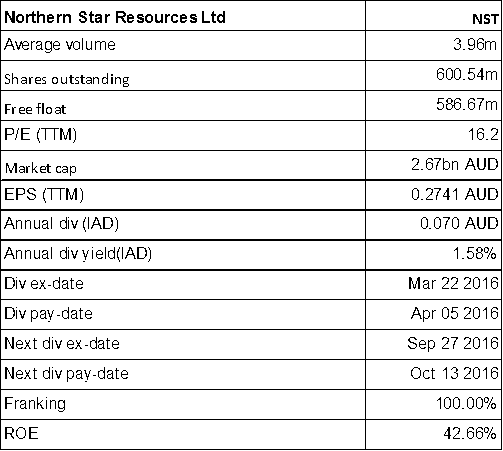

Delivered decent performance: Northern Star Resources Ltd (ASX: NST) reported for NPAT growth of 65% on yoy basis to A$151.47m. Apart from asset sold naming Plutonic gold mine, NST confirmed net profit from continuing operations was up by 80% to A$165.3m. ROE of NST grew by 39% and return on invested capital grew by 28%. NST’s full year dividend was increased 33% to 4 cents. Meanwhile, the group added over 0.5Moz at a cost of just A$50/oz leading to overall reserves of 2Moz (all revised estimates are after mining depletion of 611,000oz in FY16). Overall resources enhanced 9.25Moz in FY16 while measured and indicated resources rose 4.9Moz boosting mine lives.

Fortescue Metals Group Limited

FMG Details

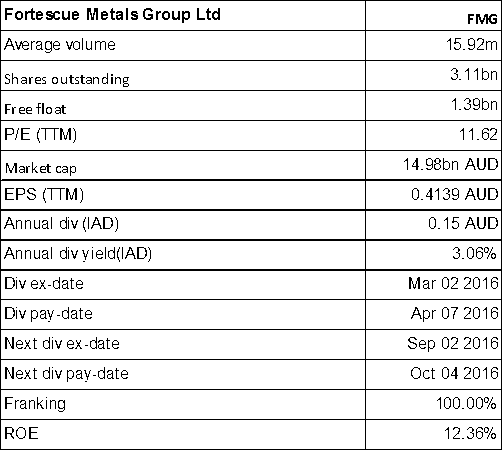

Upgraded credit quality: Fortescue Metals Group Limited (ASX: FMG) reported for 212% of NPAT of US $985m as compared to FY15. FST’s average realised price in FY16 was US$45.36/dmt and reported a decline in cost by 43% to US$ 15.43/wmt cost.

FMG’s Financial Highlights (Source: Company Report)

The group has declared fully franked dividend of 12 cents per share. Meanwhile, Moody’s Investors enhanced the credit rating to Ba2 as compared to Ba3. Moody’s even upgraded the senior secured credit rating to Ba1 and the senior unsecured credit rating to B1. The group delivered over 169.4 million tonnes (mt) during the year. On the other hand, the top line of FMG faces some pressure and reported a decline of over 17% on a yoy basis.

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...