Suncorp Group Limited

Strong reinsurance program & adequately capitalized:Suncorp Group Limited (ASX: SUN) had recently disclosed its natural hazard update evaluating the financial impacts of the hazardous events for the period ended on the 31st of December 2018. The Company’s current estimates for natural hazard costs across Australia and New Zealand for the six-month period to 31 December 2018 is at around $600-610 Mn, pre-tax. Against this, the natural hazard allowance which is to be provided is only $360 Mn. Thus, $240 million-$250 million is the hazard cost which is slated to be above the allowance already made. The firm’s reinsurance program is further supported by an additional cover of $300Mn for the events greater than the $10Mn.

.png)

SUN’s FY 2018 Financial highlights (Source: Company Reports)

The reported NPAT came in at $ 1,059Mn was marginally down by 1.5 percent in FY18 against FY17 due to one-off investment in the acceleration of the marketplace component of the strategy during the same period and a four-fold increase in the regulatory costs. Also, at the end of the previous fiscal, the group maintained a robust capital position, with all its business segments holding a CET1 ratio above the targets. The group’s excess to CET1 target (ex-div) was $448 Mn.

What to Expect from Suncorp Moving Forward: Going forth, for FY 2019, the company has targeted to achieve a cash ROE of 10%, underpinned by top line growth of ~3%-5%. The company also intends to distribute ~60%-80% of their cash earnings in the form of dividends and remain committed to returning the excess capital to the shareholders.

Meanwhile, the stock has fallen by 13.17% in the past six months as on 23 January 2019 and is trading at decent PE multiple of 15.52x. Hence, considering the strong reinsurance program & robust capitalization, we maintain our ‘Hold’ rating on the stock at the current market price of $12.960 (up 1.647% on 24 January 2019).

Insurance Australia Group Ltd.

Subdued rate performance coupled with an anticipated decline in commercial volumes: Insurance Australia Group Ltd (ASX: IAG) has recently finalized its catastrophe reinsurance program which would be providing increased gross reinsurance protection of up to $9 billion from the earlier $8 billion which was in the FY 2018. IAG has raised the limit of its main catastrophe cover to $9 billion in order to provide an added protection above the modelled exposure. The overall credit quality of the 2019 program happens to be robust with above 92% placement with the entities rated A+ or higher.

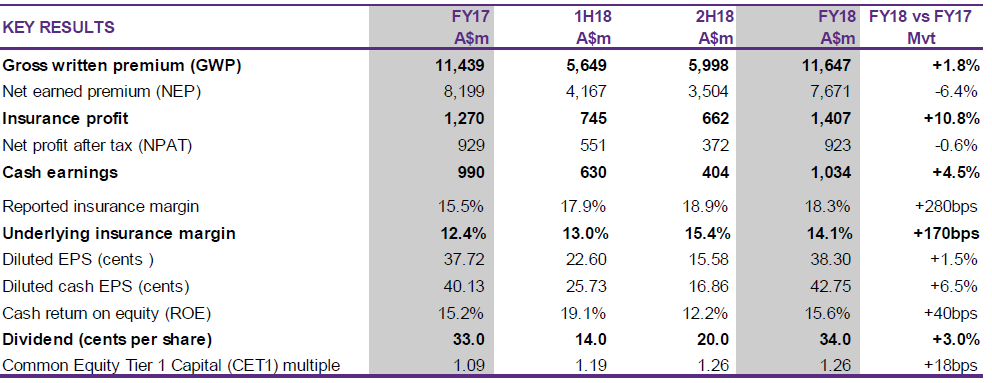

The company had posted subdued numbers for the F.Y. 2018 on account of a marginal increase in reported gross written premium of 1.8% to $11,647 Mn. This rise in GWP was predominantly rate driven. The underlying insurance margin also saw a minor rise of 1.7% while the Net profits after tax saw a dip of 0.6% & stood at $923Mn.

IAG’s Key results & comparatives (Source: Company Reports)

What to Expect from IAG Moving Forward: Going further, for FY 2019, the company had provided a GWP growth guidance ranging from 2-4% & margin guidance ranging 16%-18%. The GWP growth is expected on the back of the rate increase across personal & commercial classes offset by a slight decline in commercial volumes. The margin growth is anticipated on account of an improvement in the pre-tax profit and no material movement in exchange rates.

The company is trading at a TTM P/B multiple of around 2.50x, while the industry median is 1.70x; thus, we consider that the stock is expensive at this juncture considering the book asset that it has on its balance sheet. Meanwhile, the stock price has fallen over the past six months by 8.72% as on 23 January 2019 and is trading PE multiple of 17.79x. Hence, considering subdued rate performance on the premium front as well as the anticipated decline in commercial volumes going forth, the market players should avoid the stock at the current market price of $7.130.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...