Stocks’ Details

Myer Holdings Limited

Changes as per March 2018 Quarterly Rebalance:Myer Holdings Limited’s (ASX: MYR) stock will be removed from S&P/ASX 200 Index effective March 19, 2018 as per the March 2018 Quarterly Rebalance of the S&P/ASX Indices. On the other hand, there is a speculation that MYR could be a takeover target from groups including Solomon Lew’s Premier Investments, the major shareholder of MYR. Meanwhile, the company reported for a weak second quarter trading update after a subdued performance during the first quarter. MYR expects further deterioration in trading and has projected 1H 2018 NPAT to be between $37 million and $41 million pre-implementation costs and individually significant items. Therefore, in the second half, there will be no improvement in retail trading conditions due to the recent sales volatility. As a result, MYR stock has fallen 34.11% in three months as on March 15, 2018. However, there is an expectation of the turnaround as Chief Executive Officer and Managing Director, Richard Umbers has resigned from the company. We give a “Hold” recommendation on the stock at the current price of $0.425

G8 Education Limited

Positive growth in FY17 despite a challenging environment: G8 Education Limited’s (ASX: GEM) stock plunged 20.98% in three months as on March 15, 2018 driven by challenging market conditions continuing from 2017 with significant levels of new supply and continued weak demand growth having an impact on occupancy levels. The final result of FY17 slightly fell short of previous guidance, driven by higher discounts and increased investment in resourcing for the recently acquired centres and the kindergarten rooms. However, the centre development and acquisition strategy is performing in line with the company’s expectations and providing positive signs of continued future growth. Moreover, in FY17, GEM delivered 2.4% growth in the topline to $795.8m, 2.2% growth in Underlying Earnings Before Interest and Tax to $156.0m, after adjusting for LDCPDP funding and Underlying Net Profit after Tax of $92.9m, in line with pcp. Additionally, the increase in Government funding is due to commence in July 2018, which is expected to drive increased demand in the sector. Further, GEM’s occupancy was noted to be stable during January, with committed forward bookings heading in the right direction. Meanwhile, GEM stock is trading at a reasonable P/E and we give a “Hold” recommendation on the stock at the current price of $2.75

FY 17 Highlights (Source: Company Reports)

Ramsay Health Care Limited

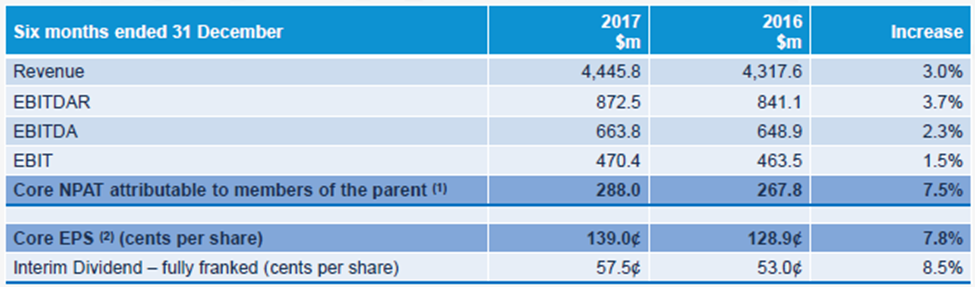

Strong performance in the Australian business in 1H 2018: Ramsay Health Care Limited (ASX: RHC) for 1H 2018 has reported 7.5% rise in Core net profit after tax to $288.0 million. The Group Revenue grew 3.0% to $4.4 billion and Group EBIT is up 1.5% to $470.4 million in 1H 2018. The EBIT grew due to the strong performance in the Australian business. The Australian operations posted 9.1% EBIT growth on the previous corresponding period due to above market volume growth and the benefits of recent cost efficiency programs. Further, there is a strong growth in admissions and procedural volumes in RHC’s Australian business, due to a rapidly ageing and growing population. The increasing proportion of people with chronic disease and mental illness is also boosting treatment volumes. However, RHC is facing a challenging environment in Europe but the company is investing in a major transformation project for the French operations that will centralise non-core hospital resources and distinguish this business for the long term. Additionally, RHC has reaffirmed the FY18 Core EPS growth of 8% to 10%. Meanwhile, RHC stock has fallen 9.01% in three months as on March 15, 2018. Given the potential and the stock price dip, we put a “Buy” recommendation at the current price of $63.32

1HFY18 Financial Performance (Source: Company Reports)

Vocus Group Limited

Removed from S&P/ASX 100 Index and reduced the underlying profit guidance for FY18: Vocus Group Limited’s (ASX: VOC) stock will be removed from S&P/ASX 100 Index on March 19, 2018 as per March 2018 Quarterly Rebalance of the S&P/ASX Indices. Further, VOC has reduced the underlying profit guidance for FY18 to be now in the range of A$125 million to A$135 million from its previous estimate of A$140 million to A$150 million. On the other hand, VOC in 1H 2018 reported for a 4% growth in the revenue to $973.6m on a constant currency basis, when compared to H1 FY17 Adjusted Pro forma Revenue. Meanwhile, VOC stock has fallen 17.8% in three months as on March 15, 2018. As the stock has been hammered in last one year, we give a “Hold” recommendation on the stock at the current price of $2.39, and would keep a watch for any catalyst for future momentum.

Fletcher Building Limited

Turnaround to loss from profit in 1H 2018: Fletcher Building Limited (Australia) (ASX: FBU) delivered operating loss of ($322) million, against $310 million profit before significant items for the first half of FY17. There was a 6% growth in revenue while net earnings before significant items of ($273) million, down from $187 million in HY17 were noted. The result includes ($631) million of Building + Interiors (B+I) losses, and an additional ($29) million of overhead and transition costs expected in 2H18, resulting in an expected full-year loss for B+I of ($660) million. The operating earnings have also fallen due to lower profits in the Construction Division, outside of B+I, as well as the Building Products Division. As a result, FBU stock has fallen 12.8% in three months as on March 15, 2018. Meanwhile, a waiver of the breach of covenants has been granted by US Private Placement noteholders at the back of losses incurred by B+I business. Looking at the challenging scenario, we give an “Expensive” recommendation on the stock at the current price of $6.01

Slater & Gordon Limited

Ongoing business transformation program & addition to All Ordinaries:Slater & Gordon Limited’s (ASX: SGH) stock will be added to All Ordinaries on March 19, 2018 as per March 2018 Quarterly Rebalance of the S&P/ASX Indices. On the other hand, 1H 2018 results reflect SGH’s ongoing business transformation program with a stronger capital structure, a simplified operating model and a clearly defined service offering. During 1H 2018, recapitalization of the Group was undertaken through the creditor’s Scheme of Arrangement, that provided SGH with a sustainable level of debt and additional liquidity. The company has separated All UK operations and UK subsidiaries and the same have been transferred to a new UK holding company wholly owned by the Senior Lenders. Moreover, in 1H 2018, SGH has reported statutory total revenue and other income from continuing operations of $96.3m compared to $117.8m corresponding period and a net loss from continuing operations after tax of $21.2m compared to $14.5m in 1H 2017. Meanwhile, SGH stock has risen 15.2% in three months as on March 15, 2018 at the back of recent developments and updates, post a 51.5% fall in last six months. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $3.64

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...