Woodside Petroleum Limited

.png)

WPL Details

Acquisition of half of BHP Billiton’s Scarborough area assets: Woodside Petroleum Limited (ASX: WPL) has entered into a binding sale and purchase agreement to acquire half of BHP Billiton’s Scarborough area assets in the Carnarvon Basin, located offshore Western Australia. The deal would complement WPL’s growth strategy and would leverage the company’s deep water production and LNG capabilities. The acquisition includes a 25% interest in WA-1-R for which ExxonMobil is the operator as well as a 50% interest in WA-62-R, which together contain the Scarborough gas field. WPL would also acquire a 50% interest in WA-61-R and WA-63-R which contain the Jupiter and Thebe gas fields.

.png)

Asset Overview (Source: Company Reports)

WPL has agreed the deal for $400 million which consists of US$250 million on completion of the transaction and a contingent payment of US$150 million upon a positive final investment decision to develop the Scarborough field. The Scarborough area assets including the Scarborough, Thebe and Jupiter fields, are estimated to contain the gross 8.7 trillion cubic feet of gas resources at the 2C confidence level. WPL’s net share of the resources is estimated to be 2.6 trillion cubic feet of gas. WPL is targeting completion of the transaction by the year-end 2016.

However, the acquisition is subject to the pre-emption rights, FIRB clearance and NOPTA approval and registration. The resources will then be booked by WPL as contingent resources after the completion. We give a “Buy” recommendation on the stock at the current price of $26.52

WPL Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

.png)

IAG Details

Buy Back program might support the stock: Insurance Australia Group Ltd (ASX: IAG) has announced the $300 million off-market share buy-back as part of the capital management program which is expected to be completed in mid-October 2016. We believe that this program could support the group’s stock price, which fell over 3.89% in the last four weeks (as of September 27, 2016) due to rising claims pressure.

.png)

FY 16 Financial Performance (Source: Company Reports)

In addition, IAG has reported 14.1% fall in the net profit after tax to $625 million in FY 16. On the other hand, the insurance profit grew 6.8% to $1.18 billion on FY15 and reported margin is of 14.3%. Moreover, IAG’s reported margin guidance for FY17 is 12.5-14.5%; and for FY17, IAG expects the GWP to be relatively flat. However, the group’s longer-term outlook is said to remain positive. Having a decent dividend yield, we give a “Buy” recommendation on the stock at the current price of $5.42

IAG Daily Chart (Source: Thomson Reuters)

Macquarie Group Ltd

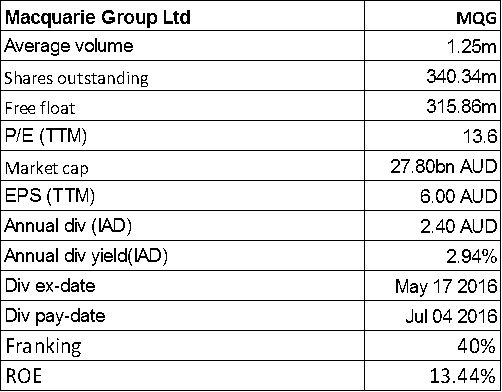

MQG Details

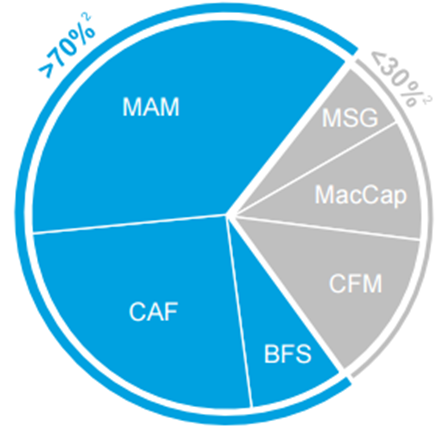

Weak short term outlook: Macquarie Group Ltd (ASX: MQG) expects 1H17 result to be broadly in line with the 2H16 result, subject to the conduct of period end reviews and the completion rate of transactions. MQG has over $A499 billion assets under management as at 30 June 2016. However, for first quarter of 2017, operating group contribution, which includes performance fees and asset disposals are down against prior corresponding period.

FY 17 Outlook (Source: Company Reports)

The capital markets are facing businesses less than 30% due to subdued market conditions. The stronger activity in Commodities and Financial markets (CFM) is also reflecting resilient trading across most of its businesses. In addition, the group’s short-term outlook is subject to the market conditions, including the impact of foreign exchange and the potential regulatory changes and tax uncertainties. We give an “Expensive” recommendation on the stock at the current price of $82.58

MQG Daily Chart (Source: Thomson Reuters)

CSL Limited

.png)

CSL Details

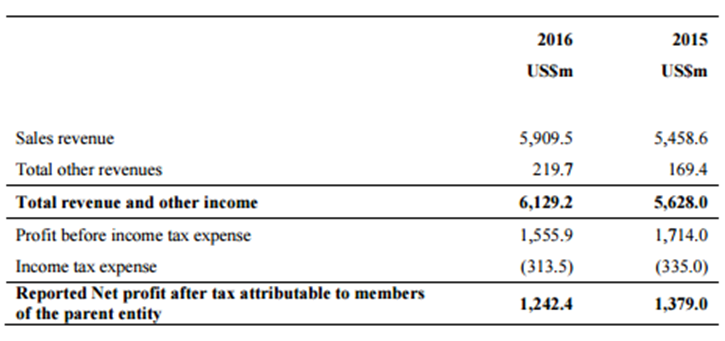

FDA acceptance of BLA: CSL Limited (ASX: CSL) had announced that the US Food and Drug Administration (FDA) has accepted for review of CSL Behring’s Biologics License Application (BLA) for its low-volume subcutaneous (SC) C1-Esterase Inhibitor (C1-INH) Human replacement therapy, CSL830, as prophylaxis to prevent Hereditary Angioedema (HAE) attacks. Moreover, CSL has reported a net profit after tax (NPAT) of US$1,242 million in FY 16, representing a fall of 11%.

FY 16 Financial Performance (Source: Company Reports)

After excluding the Novartis influenza vaccines business financials (acquired in FY 16), the underlying NPAT grew 5% and earnings per share (EPS) grew 7% on a constant currency basis. On the other hand, CSL stock fell over 3.5% in the last one month (as of September 27, 2016), on investors’ concerns over the group’s cash flow and its products progress. Moreover, the stock is trading at a high P/E. We still believe that the stock is “Expensive” at the current price of $108.87

CSL Daily Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Details

Senior secured notes: Transurban Group’s (ASX: TCL) financing vehicle Transurban Finance Company Pty Ltd has priced US$550 million of senior secured 10.5 year notes in the US 144A bond market. The group reported a proportional toll revenue growth of 17.5% to $1,946 million in FY 16 and the average daily traffic (ADT) grew by 8.0%. TCL has reported the statutory profit from ordinary activities of $22 million and the proportional earnings before interest, tax, depreciation and amortization (EBITDA) and before significant items grew by 14.8% to $1,480 million.

.png)

FY 16 Statutory results (Source: Company Reports)

Moreover, TCL has $9 billion of development projects to improve customers’ trips in Melbourne, Sydney, Brisbane and Greater Washington Area.

Meanwhile, TCL stock fell 5.3% in the last one month (as of September 27, 2016) due to concerns of a possible slowdown in toll revenue coupled with profit booking by investors. The stock is trading at an unreasonable P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $11.28

.PNG)

TCL Daily Chart (Source: Thomson Reuters)

Telstra Corporation Ltd

.png)

TLS Details

Moderate outlook for FY 17: Telstra Corporation Ltd (ASX: TLS) has lately responded to the Australian Competition and Consumer Commission (ACCC) regarding commencement of an inquiry to determine whether it would declare mobile roaming services. On the other hand, Telstra has already invested $3 billion over the next three years on its network for winning back its customer base but this can pressurize the balance sheet. TLS earlier reported 6.3% growth in revenues to $28.3 billion in FY 16 and 36% growth in the net profit to $5.8 billion including $1.8 billion from sale of Autohome shares compared to FY 15. TLS had resorted to the total of $1.5 billion of the share buyback in which $1.25 billion was off-market buyback and $250 million was on-market buyback. Moreover, TLS has added 560,000 mobile customers and 235,000 fixed broadband customers in FY 16. On the other hand, TLS’s outlook is ‘mid to high’ single digit revenue growth, and ‘low to mid’ single digit EBITDA growth in 2017.

.png)

FY 17 Guidance (Source: Company Reports)

The stock fell over 2.6% in the last one month (as of September 26, 2016) and we believe the pressure could continue in the coming months. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $5.10

TLS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...