Seafarms Group Ltd

.png)

SFG Details

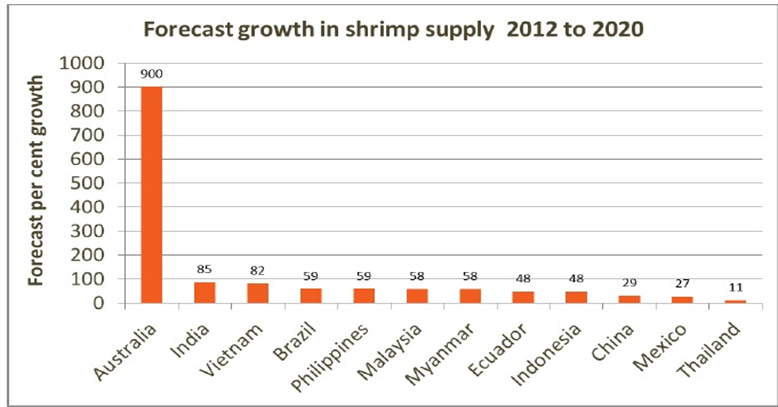

New Lead Advisor & Growing seafood market: Seafarms Group Ltd (ASX: SFG) sometime back signed a funding mandate with a leading global investment bank Pareto Securities to appoint it as its Lead Advisor. The bank will assist SFG to secure the required funding for Stage 1 of Project Sea Dragon - the 10,000 hectare tiger prawn aquaculture facility which the company is planning to develop in Northern Australia at an estimated cost of around $1.4 billion. Seafarms expects to complete more than 4-year developing project by late 2016. With the help of Pareto, which is the largest Nordic investment bank in the seafood sector, SFG is confident that an appropriate and flexible financing package for Stage 1 can be secured. In July 2015, the project was awarded as the major project status by the Northern Territory and Australian government.

Growth Opportunity - Seafood market (Source: Company reports)

The farm, which aims to begin exports in 2018, is expected to produce more than 100,000 tonnes of prawns a year - equivalent to more than 3 billion of the crustaceans and some 20 times Australia’s current annual production. The country's Minister for Infrastructure and Regional Development Warren Truss reported that the farm comes at the right time to meet surging global demand and takes advantage of northern Australia's inherent benefits of space, location and opportunity.

Meanwhile, SFG recorded $27.2 million in revenue in FY15 compared to $23.7 million in the previous year. The stock has surged 21.43% in the last five days and 30.77% in the last one month (as at January 06, 2016). We believe SFG stock has the potential for momentum and accordingly, we put a “BUY” rating to this stock at the current share price of $0.088

SFG Daily Chart (Source: Thomson Reuters)

Stockland Corporation Ltd

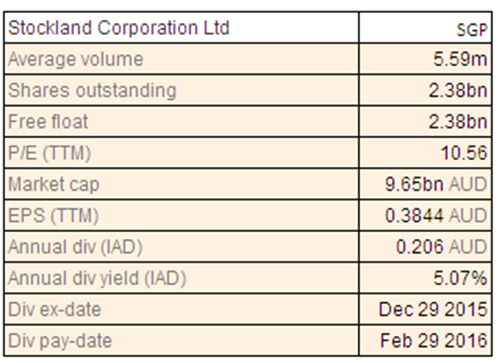

SGP Dividend Details

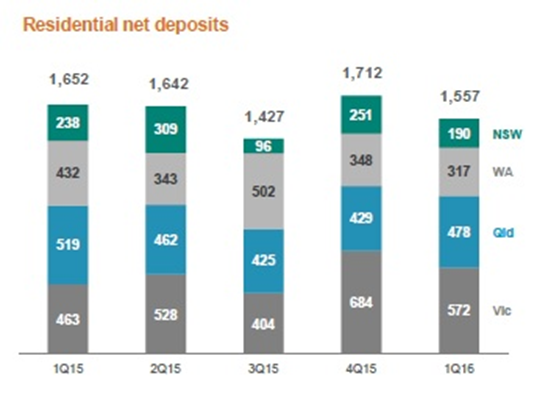

Strong quarterly performance and ongoing pipeline growth: In its first quarter 2016, Stockland Corporation Ltd (ASX: SGP) reported strong performance across all key business areas and is on track to achieve its target of around 6000 residential settlements this fiscal year. Residential sales remained robust with a further 1,557 net deposits for the quarter, with project release timing in Sydney influencing the NSW result. First quarter deposits combined with the deposits already on hand at the end of FY15, total 5,299 with majority settling in financial year 2016 and balance in financial year 2017. SGP's new projects continue to strengthen its returns with operating profit margins over 14%. Looking ahead, Stockland is well placed to achieve full year lot settlements of around 6,000with commercial property comparable Funds from Operations (FFO) growth of 3-4%and comparable Net Operating Income growth of 2-3%. For financial year 2016, the company is on track to achieve underlying EPS growth of 6% - 7.5% and FFO per security growth of 8.5% - 10% assuming no material change in market conditions. Meanwhile, annual distribution per security is targeted at 24.5 cents.

Residential net deposits (Source: Company reports)

Recently, SGP announced that it will acquire a 6.3 hectare Greenfield development site at Stamford Park, Rowville, 26 kilometres south east of the Melbourne CBD for $17 million in its drive to grow medium density pipeline. First settlements on new homes is expected in financial year 2019 with foreseen project financial returns above Stockland’s hurdle rates. Based on a strong foundation and outlook, good dividend yield, and reasonable P/E, we rate this stock a “BUY” at current share price of $4.05

SGP Daily Chart (Source: Thomson Reuters)

Aurizon Holdings Ltd

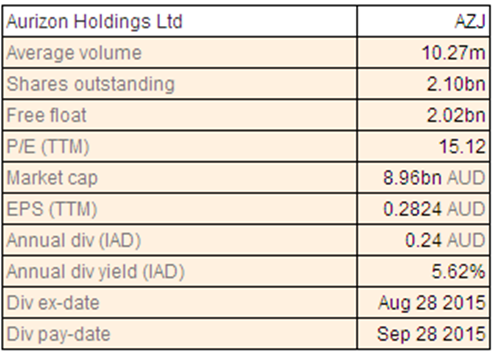

AZJ Dividend Details

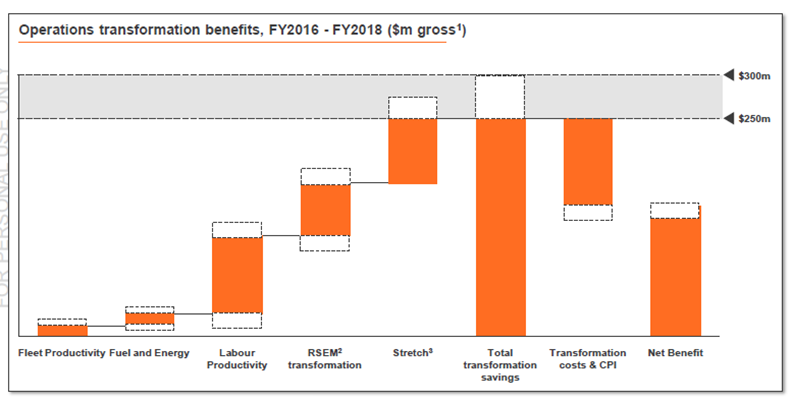

New agreement to drive opportunities:Recently, Aurizon Holdings Ltd (ASX: AZJ) signed a Heads of Agreement with NSW Ports to operate the Enfield Intermodal Logistics Centre (ILC) in Western Sydney and lease the land at the site, enabling the company to accelerate growth plans for its intermodal freight business. The agreement is non-binding at this stage but the parties expect a binding lease and terminal operator agreement to be signed in the first quarter of 2016. The move with regards to Enfield will be cost-neutral and offer new revenue opportunities for Aurizon’s intermodal business. This move is mainly driven by Aurizon recently adding 175 new wagons into its national intermodal operations, a commitment for a new intermodal terminal in Townsville and the introduction of a new freight management technology to improve customer service and grow the business. Australia’s domestic freight task is expected to triple from its current size by 2050 and there is a rigorous industry push to increase rail’s share of the growing freight transport task through productivity and customer focused initiatives. Meanwhile, for the financial year 2015, AZJ’s underlying EBIT increased 14% to $970 million while statutory NPAT was higher by 139% to $604 million. Underlying operating ratio in 2015improved to 74.3% from 77.7% in 2014. Operational transformation has delivered $195 million in gross savings in financial year 2014 and 2015, against a target of $160 - $200 million. Final dividend increased 64% to 13.9 cents per share.

Positive outlook (Source: Company reports)

Aurizon recently announced that the next phase of its transformation program will deliver further cost reductions and productivity benefits totalling $310 million -380 million for the three years from financial year 2016 –2018. In its recent share price fall, which was led by subdued commodity prices thus impacting volume and revenue growth outlook, the company believes that it needs to ramp up transformation program to ease these challenges. The softness in the commodities outlook made AZJ announcing its guidance for the 2016 financial year with first-half EBIT of A$390 million-A$410 million (down by 16%-20% relative to 1H15) and challenges with second-half haulage volumes (3-4% reduction). The company also planned to book an impairment hit given the investment in iron-ore miner Aquila Resources Ltd., surplus rolling stock and inventory, and uncertainty on the timing of an expansion of a coal network in eastern Australia. The stock has fallen about 20.04% in the last one month (as at January 06, 2016).

However, the company remains on target to achieve savings in operations. Further, management still has the capital management incentives such as raising the payout ratio and resuming the share buy-back program. Based on above stated factors, we rate this dividend yield stock a BUY at the current share price of $4.21

AZJ Daily Chart (Source: Thomson Reuters)

Spark New Zealand Ltd

.png)

SPK Dividend Details

Acquisitions driving growth: For full year 2015, Spark New Zealand Ltd (ASX: SPK) recorded an increase of 2.8% in its EBITDA levels. Net earnings after tax from continuing operations stood at $375 million, higher by 16.1%. Total mobile revenue share grew by 2% to 41% driven by excellent growth in consumer revenue, however the market remains very competitive. Broadband revenues returned to modest growth in FY15, driven by a focus on higher value plans. Broadband connections increased 1.6% despite intense competition. Recently, SPK announced that it has agreed to acquire 70MHz block of 2.3GHz spectrum from Craig Wireless and its related company Woosh Wireless (NZ) Limited for NZ$9 million.

Financial Performance and Outlook (Source: Company reports)

Besides, Spark New Zealand concluded the acquisition of privately?owned South Island based IT infrastructure and professional services company Computer Concepts Limited (CCL) for NZ$50 million.

This is mainly to boost its cloud capabilities which will add cloud and platform IT services and extend Spark’s business in the South Island. Upon the completion of the acquisition, the CCL brand will be retained and CCL will continue to run as a standalone business. Based on the above factors, we rate this dividend yield stock a “BUY” rating at the current share price of $3.05

.png)

SPK Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...