Oil Search Limited

.png)

OSH Details

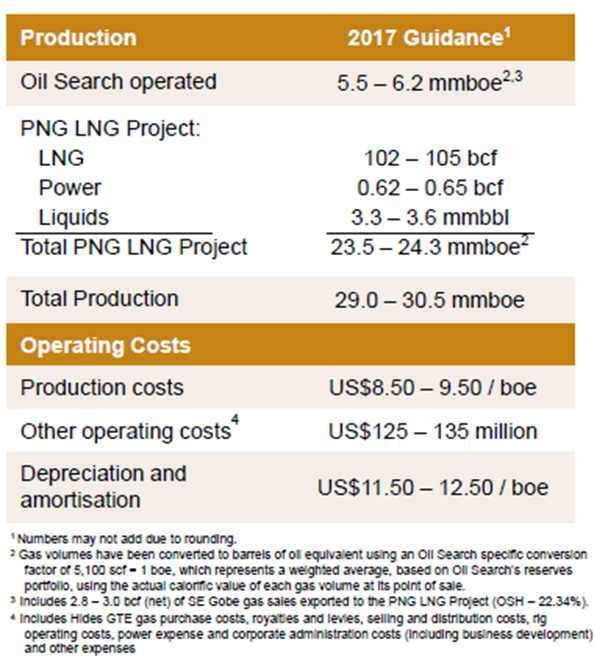

On track for 2017 Production:Oil Search Limited (ASX: OSH) has reported annualised production rate in 3Q17 of 8.6 MTPA, which is approximately 25% above nameplate after the compressor upgrades in May. The company has completed further work on compressors, which is anticipated to enable current higher levels of production to be maintained or exceeded. Moreover, OSH is on track to deliver 2017 production at upper end of guidance range of 29.0 – 30.5 mmboe, as the production for the nine months to 30th September 2017 is of 22.7 mmboe.

2017 Guidance (Source: Company Reports)

On the other hand, OSH is acquiring 25.5% interest in Pikka Unit and adjacent exploration acreage and 37.5% in Horseshoe Block located in Alaska’s North Slope, from Armstrong Energy LLC and GMT Exploration Company LLC for US$400m in cash. OSH will assume operatorship on 1 June 2018. It is anticipated that combined with world class PNG assets, Alaska will provide OSH with unprecedented platform for growth. Meanwhile, OSH stock has risen 10.02% in three months as on December 05, 2017. Further, on-track progress for PNG JVs to deliver a formal co-operation agreement to the PNG government soon might open up other channels for OSH’s interests. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $7.18

.png)

OSH Daily Chart (Source: Thomson Reuters)

Westpac Banking Corporation

WBC Details

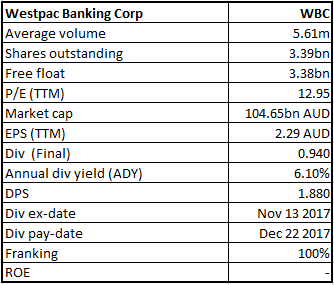

Banking sector challenges:Westpac Banking Corporation’s (ASX: WBC) stock was hammered as the government announced plans for a Royal Commission into the alleged misconduct of Australia’s banking and financial services sector. This step has been taken by the government to ensure that the financial system is working efficiently and effectively. On the other hand, Chief Risk Officer, Alexandra Holcomb will retire in 2018. WBC is expected to provide more insights on its performance during its upcoming AGM. Bank’s FY17 statutory net profit of $7,990 million was up 7% with 3% rise in cash earnings to $8,062 million. However, a mixed outlook with uncertainty of policies (such as energy policy, transport infrastructure, or fixing up the tax arrangements between the states) has been highlighted to impact investments from customers. While the bank might comfortably meet APRA’s unquestionably strong capital benchmark by virtue of undiscounted dividend reinvestment plans, the ongoing banking sector challenges are posing some pressure. WBC stock has fallen 1.47% in three months as on December 05, 2017 and we give an “Expensive” recommendation on the stock at the current price of $30.97

.png)

WBC Daily Chart (Source: Thomson Reuters)

Aventus Retail Property Fund

.png)

AVN Details

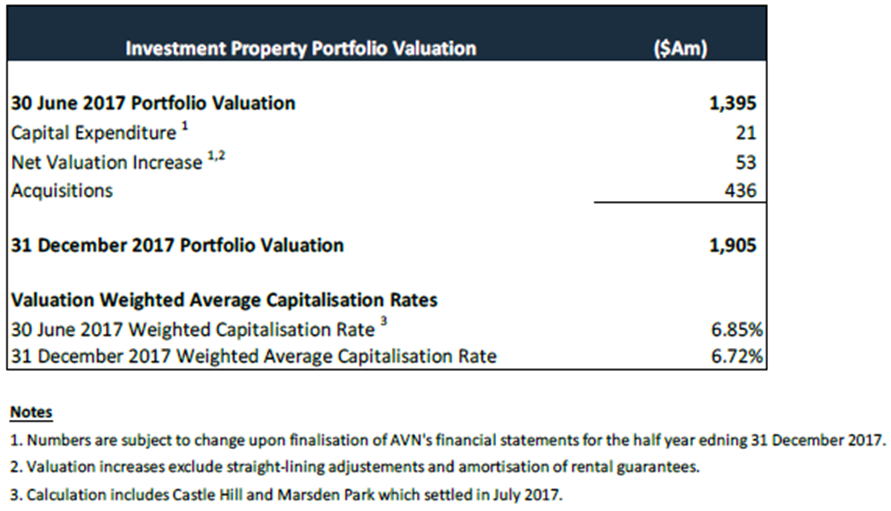

Increase in Portfolio Value:Aventus Retail Property Fund (ASX: AVN) reported for an enhanced portfolio value by $53 million, as at 31 December 2017. In this, the value of the AVN Portfolio has increased to $1.905 billion during the period. The capital expenditure and the acquisitions of Sydney centres at Castle Hill and Marsden Park that settled in July 2017 also led to the portfolio’s growth. The increase in the value of the portfolio reflects annual rent increases, market rent increases and the completion of value-adding developments that are accretive to both the amenity and value of the Centres.

Investment Property Portfolio Valuation (Source: Company Reports)

Moreover, the properties independently valued for the half has contributed approximately $44m of the $74m gross valuation growth, which reflects a circa 7% increase over the six months since 30 June 2017. Additionally, the weighted average capitalisation rate for the portfolio has been tightened by 20bps to 6.72% at 31 December 2017 compared to 6.85% at 30th June 2017, which also led to the net valuation gain in the portfolio. Given the trading scenario, we put a “Speculative Buy” recommendation on the stock at the current price of $2.35

.png)

AVN Daily Chart (Source: Thomson Reuters)

Bapcor Ltd

BAP Details

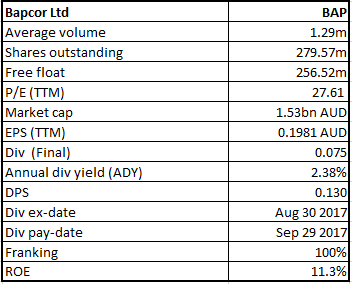

Deriving value from acquisitions: Bapcor Ltd (ASX: BAP) is in the process of integrating Hellaby Automotive, which is now known as Bapcor New Zealand. The company anticipates delivering between $8M to $11M EBIT of annual benefit per annum by 2020, that includes programs such as increased intercompany sourcing and private label programs. Moreover, as part of the Hellaby acquisition BAP has also acquired the non-core business of Resource Services, consisting of the Contract Resources and TBS, and also a non-core Footwear business. BAP has now successfully completed the sale of the Footwear and Contract Resources business (excluding North America), and signed a sale agreement for Contract Resources North America with progress on the divestment of the remaining non-core business, TBS. Additionally, BAP will consolidate the recent acquisitions in 2018. The company is on track for FY18 forecast of 30% NPAT growth on continuing operations. Meanwhile, BAP stock has fallen 1.26% in three months as on December 05, 2017 and is trading at a high level. Recently, BAP announced that CEO and Managing Director Mr. Darryl Abotomey has sold 600,000 shares at a price of $5.90, and this led the stock fall by about 7% in last five days. Given the potential arising from consolidation of acquisitions and continued performance, we put a “Speculative Buy” recommendation on the stock at the current price of $5.52

.png)

BAP Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...