Bingo Industries Ltd

Strong Growth Trajectory Continues: Revenue during 1HFY18 was recorded at $142.4 Mn vs $99.5 Mn in 1HFY17, marking a solid year on year (YoY) growth of 43.2% for Bingo. The sales spiked up due to increased operating footprint, exposure to strong market and increased market share across business during 1HFY18. The company reported lower EBITDA margin during the period, recorded at 30.8% against 31.5% in 1HFY17, i.e., down by 70 bps. This resulted from inclusion of acquired Victorian businesses and higher operating cost to support national expansion. However, pro-forma NPAT grew by 37.1% to $21.3 Mn in 1HFY18 from $15.5 Mn in 1HFY17. The Company continued to generate strong free cash flow and the operating free cash flow increased by 27.8% and moved from $27.8 million to $35.5 million. The company has witnessed an increase in post-collections network capacity from 1 Mn tonnes per annum to 1.7 Mn tonnes per annum and it is on track to record 3.4 Mn tonnes per annum in 2020. In addition to this, the company has laid focus on implementing cost effective measures and expects to deliver pro-forma EBITDA of approximately $93 Mn in full year of FY18.

.png)

Network Capacity (Source: Company Reports)

The positive business momentum has continued into 2HFY18 with greater contributions from completed acquisitions to be realised in the 6-month post December 2017. Meanwhile, In the past six months, the share price rose by 19.8% and up by 5.34% in last five days as on March 12, 2018. Lately, Commonwealth Bank ceased to be a holder of the stock, which seems to be trading at a higher level and looks “Expensive” at the current market price of $2.82

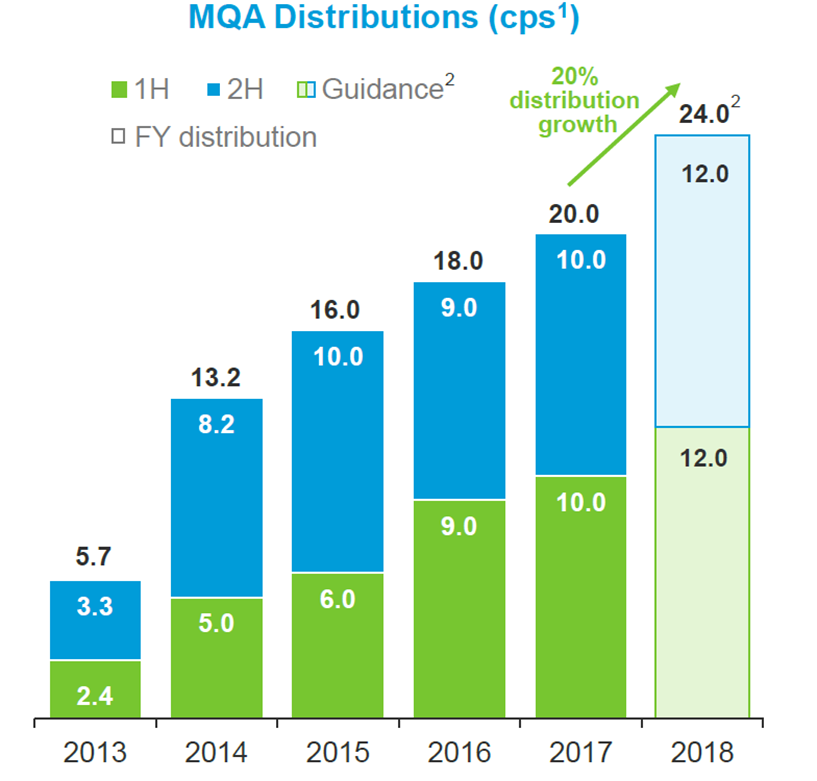

Macquarie Atlas Roads Group

Focus on distribution and enhanced portfolio: Macquarie Atlas Roads Group (ASX: MQA) is one of the largest developers and operators of private toll roads and its revenue and other income from operation was reported at $473 Mn in FY17 against $70.6 Mn in FY16, which is up by 570% on YoY basis. The revenue surged up due to gain on the revaluation of the original investment in Dulles Greenway of $375.6 Mn and consolidation of TRIP II’s (Toll Road Investors Partnership II) toll revenue of $75.7 Mn from TRIP II acquisition date. Proportionate EBITDA from assets stood at $652.8 Mn in FY17 as compared to $569.2 Mn in FY16, up significantly on a year on year basis. This EBITDA growth has been supported by revenue growth and cost control strategy during the same period. NPAT came at $519.6 Mn in FY17 from $225.1 Mn in FY16 on the back of revaluation gain which is related to the acquisition of an additional 50% economic interest in Dulles Greenway as well as the share of new profit from MCQ’s investment in APRR. Aggregate portfolio traffic grew by 2.7% as compared to the prior corresponding period and was underpinned by the continued traffic growth on the APRR network which was partially offset by the traffic performance at the Dulles Greenway.

MQA Value Proposition (Source: Company Reports)

Moreover, the company has continued its focus on growing distributions and enhancing portfolio via active asset management and disciplined capital management. The stock price declined by 9.27% in last three months; while it is up by 6.97% in last one month as on March 12, 2018. Hence, we give a “Hold” recommendation at the current price of $5.70

Stockland Corporation Ltd

Diversified Portfolio: Stockland Corporation Ltd (ASX: SGP) is one of the largest diversified property groups in Australia with more than $17.9 Bn of real estate assets and has delivered strong profit for the half year ended 31 December 2017, reflecting the benefits of the diversified business model. Statutory profit for the half was recorded at $684 Mn and the Group generated funds from operations (FFO) of $436 Mn, an increase of 18.2% on the previous corresponding period. Statutory EPS stood at 28.3 cents, down 3.4% as compared to 1HFY17. The company has more focus on generating strong demand across Residential business; consistent leads for Retirement Living business; vibrant resilient retail town centres; and employment hubs in Logistic and business parks. This strategy will help it to broaden customer base and support improved asset returns, operational efficiency and maintain capital strength going forward. We expect that the company will grow further on the back of favourable economic conditions. On the other hand, the company has appointed Mrs. Robyn Elliott to the new position of Chief Technology and Innovation Officer (CTIO), directly reporting to MD & CEO of the company. Moreover, the dividend and distribution payable for the half year ended 31 December 2017 was 13 cents per share, with a forecast full year distribution of 26.5 cents for the year to 30 June 2018. Population growth and associated infrastructure investment are key drivers of the business and with a strong balance sheet, good earning visibility, growing development pipelines, the company is well positioned to tap the market needs in Australia. However, the stock price declined by 6.8% in last six months as on March 12, 2018, and we have a “Hold” recommendation at the current price of $4.10

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...