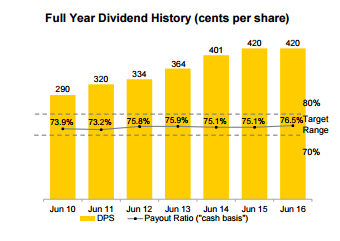

The dividends of Australia’s big four banks lately seem to be in the danger zone as they have been under pressure with overall cash profit from the big four banks dropping 3% to $14.8 billion in H1FY16 (KPMG report). Even share prices of these banks have been said to decline by 11% to 25% over the last one year. The fall in profit in H1FY16 is one of the indicators for full year profit to likely be impacted to some extent. Moreover, the National Australian Bank (NAB), Westpac Banking Corporation (WBC) and Commonwealth Bank of Australia (CBA) have kept their dividend steady during the first half 2016 but Australia and New Zealand Banking group (ANZ) had cut its dividend by 7% from 86 cents to 80 cents, and that gave a signal to the investors for likely cuts in dividends by other three banks going forward, with their final result announcement. Currently, Westpac Banking Corp (ASX: WBC) has an annual dividend yield of about 6.2% while National Australia Bank has about 7.2% dividend yield. Commonwealth Bank of Australia has about 5.7% dividend yield while Australia and New Zealand Banking group has about 6.5% dividend yield (as of August 24, 2016). The recent full year financial results for CBA however indicated that the bank has maintained a total dividend for the year to $4.20, flat over the prior year with the final dividend of $2.22 per share. This came at the back of the financial performance by the bank.

CBA’s full year dividend history (Source: Company Reports)

Nonetheless, difficult economic and market conditions combined with tougher regulations continue to be headwinds for these major banks. Moreover, rising loan losses and weaker demand for credit are some of the factors that could impact the future earnings of the banks, consequently impacting dividend payments. Furthermore, the corporate bad debts had affected the performance. Even though the mortgage debt had not deteriorated, it still raises some concerns over a possible pressure. The loan impairment charges are expected to weigh on earning results in coming years. Furthermore, lower interest rate also continues to drive competition within the sector.

On the other side, Australia’s household debt to income ratio jumped from 167% in 2011 to 186% in 2015 (as per HSBC report). Australian banks heavily invested in inflated real estate markets in the world. The big four banks had issued more than 80% of the countries residential property mortgage. The fall in housing prices also seems to impact the banks’ market performance. Moody’s investor services have also warned about the resurgence in house prices and debt. Furthermore, one of the major factors contributing to the lack of dividend growth is the additional requirement for the banks to hold more capital against the loans they write. This was the reason why banks raised additional capital in the year 2015.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...