a2 Milk Company

.png)

A2M Details

-

Increased the full year estimates: a2 Milk Company Ltd (ASX: A2M) stock surged by a whopping 13.6% on June 15, 2016 driven by the group’s enhanced estimates despite the regulatory pressures of infant formula from China. Earlier, the group reported that they are well placed to withstand the infant formula regulatory changes in China. The group is also adjusting its manufacturing and distribution model to survive these changes from China as well as rising competition. Consequently, A2M estimates a solid second half of FY16 performance and do not estimate a major change in June market conditions. Moreover, the group even enhanced its estimates in the range of $350 million to $360 million while operating EBITDA is expected to be in the range of $52 million to $54 million for fiscal year of 2016. A2M estimates its balance sheet to be strong by year end on the back of a better operating cash flow in the second half with cash likely to exceed $50 million. A2M stock is also getting added in the S&P/ASX 200 index effective from 17 June 2016.

-

Recommendation: We maintain our “Hold” stance on the stock at the current price of $1.71

Bellamy's Australia Ltd

.png)

BAL Details

-

Growing distribution network: Bellamy's Australia Ltd (ASX: BAL) stock surged over 3.5% on June 15, 2016 even though there is no specific update from the group. This rise in the stock could be due to the strong rally in its rival, a2 Milk Company which estimates a better fiscal year of 2016 despite China regulation changes for infant formula. BAL stock corrected over 10.3% (as of June 14, 2016) in the last four weeks as investors were worried over the China’s impact on its performance. On the other hand, even BAL is positioning itself to withstand any regulatory impact on its performance in China. The group enhanced its strategic partnerships in China and building solid distribution network via multiple consumer touchpoints which comprises MBS chains, e-commerce platforms, flagship stores and C2C pathways. Accordingly, better supply chain would enhance its volumes and hence the performance. BAL is also producing at Fonterra which would add to its volumes performance for first quarter of FY17. The group already built a solid network in its core Australian market with more than 4,000 distribution points across the country. BAL is boosting its management and recently appointed Mr Cohen and Ms Henry.

-

Recommendation: We maintain our “Speculative Buy” on the stock at the current price of $10.87

.png)

Strong China network (Source: Company reports)

Asaleo Care Ltd

.png)

AHY Details

-

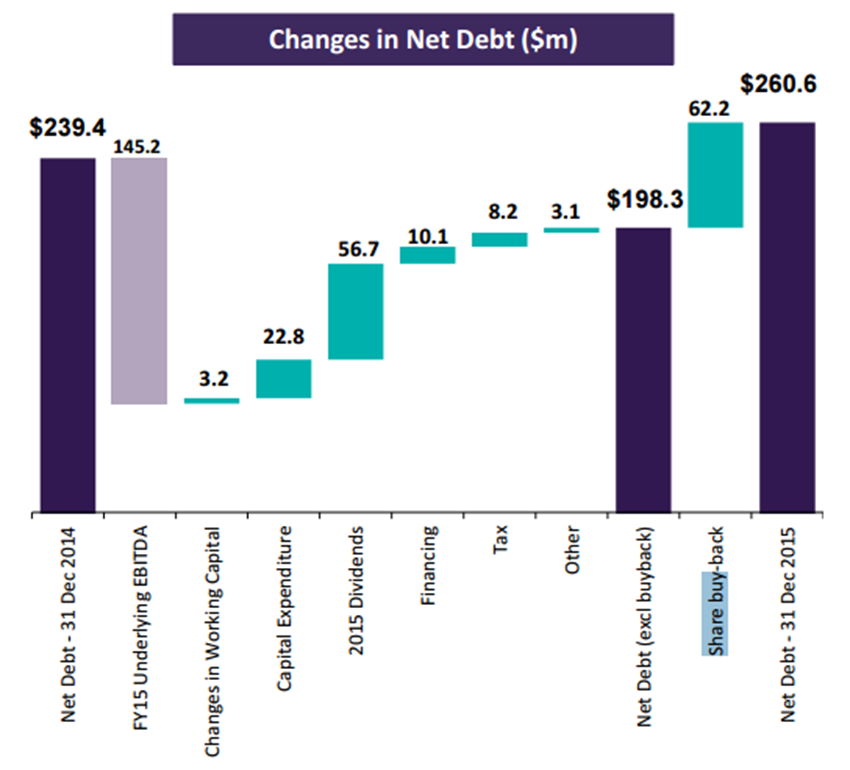

Strong buyback program: Asaleo Care Ltd (ASX: AHY) stock surged over 3% on June 15, 2016 driven by its update of a solid buyback activity report. This indicates the group’s confidence over its performance in the coming months. The group delivered an underlying NPAT rise of 5.3% to $76.1 million and an underlying EPS increase of 12% to 13.4cps which even comprise EPS accretive impact on its buy-back activities. The group’s segments Tissue and Personal Care EBITDA rose by 3.4% and 2.9% respectively. AHY estimates a steady underlying EBITDA and NPAT for FY16. AHY generated over 29.03% in the last six months (as of June 14, 2016).

-

Recommendation: We give a “Hold” on this dividend yield stock at the current price of $2.06

Buyback spending in FY15 (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...