Dicker Data Limited (ASX: DDR)

.png)

DDR Details

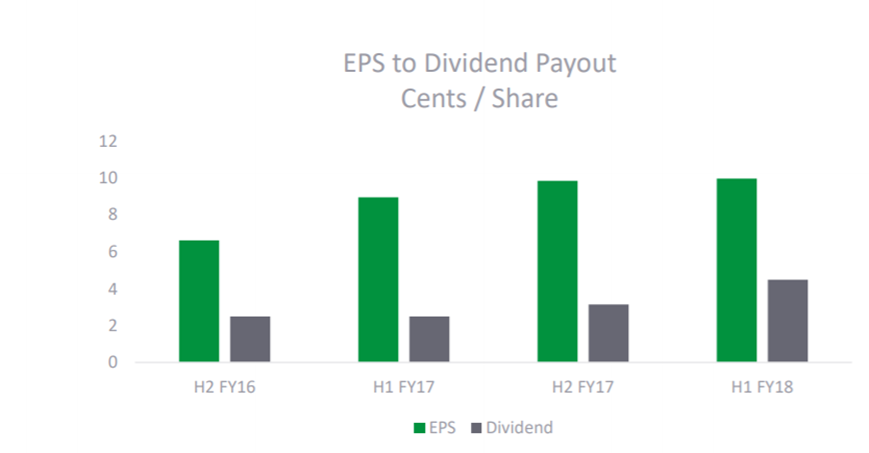

Proposed Quarterly Dividend based on projected Earnings: Up 3.19% on March 05, 2018, Dicker Data announced that it will retain its current Dividend Policy of paying quarterly dividends. In line with its last financial year and to provide consistency and certainty to investors, the Company proposed that each interim dividend for FY18 will be at an equal rate. The proposed rate for the interim dividends for FY18 will be 4.40 cents per share fully franked. This would bring total proposed dividend to be paid in the FY18 year to 18.00 cents per share which is an increase of 9.8% from FY17 dividend of 16.40 cents per share. The Group has forecasted a revenue of $1.38 billion and a net profit before tax of $42.5m for FY18. This forecast is split between Australia and NZ as follows: -

.png)

Revenue Split between Australia and New Zealand (Source: Company Reports)

The consolidated revenue and profit growth is expected to be at 6% for FY2018 and the projected growth for the Australian business is maintained at over 10%. The growth in the Australian business is expected to be achieved through organic growth and by full year contribution from new vendors. Its quarterly dividend rate is based on the expectation of generating pre-tax profits of $42.5m and after-tax profits are expected to be around $29.9m for FY18 after taking into consideration a tax rate of 30%. By looking into the growth prospects, we give a recommendation to “Hold” the stock at the current market price of $2.91

.png)

DDR Daily Chart (Source: Thomson Reuters)

Nick Scali Limited (ASX: NCK)

.png)

NCK Details

Profitability continues to trend favourably: The Group will pay dividend of AUD 0.16 on March 28, 2018 and has announced the appointment of Stephen Goddard as an independent non-executive director of the Company with effect from 1 March 2018. If we talk about the financial performance of HY18, the sales increased by 8.1% as sales were about $128.0m in HY18 against $118.4 in HY17. Gross margin and NPAT increased by 90 bps and by 15.0%, respectively over HY17. In FY17, 20 cps of final ordinary dividend was paid as compared to 14.0 cps in FY16.

.png)

Performance Summary (Source: Company Reports)

An interim dividend for HY18 of 16.0 cps was declared as compared to 14.0 cps in FY17. Six new stores were opened in the first half of FY18 which performed above expectations. It is now expected that net profit after tax for the full year to June 18 will be 5-10% higher than the previous corresponding period. FY19 is expected to benefit from the substantial increase in the store network which will be established during FY18. The stock price was up by 12.58% in the past six months and the stock now seems “Expensive” at the current market price of $7.30

.png)

NCK Daily Chart (Source: Thomson Reuters)

Accent Group Limited (ASX: AX1)

.png)

AX1 Details

Well positioned business to manage competition: Sales for HY18 were $350.3 m reflecting a rise of 17% as compared to the same period of last year. New and annualised stores were opened during the half (22 new stores were opened and 7 closed down). Cost of Doing Business (CODB) increased due to additional operating costs associated with new stores, ongoing investment in infrastructure for new stores and cost related to the digital support team and digital marketing. Underlying EBITDA was $50.0m that is up by 16.5% on pcp basis. Wholesales sales were in line with expectations and margins also improved due to cleaner inventories and improved exchange rates. The group is in the discussions with several new global brands for ANZ distribution licences and continues to investigate future opportunities for its existing distribution agreements.

Earnings Details (Source: Company Reports)

The Group has declared a fully franked interim dividend of 3.0 cents per share which is payable on 22 March 2018. The Group expects 2018 dividend pay-out ratio to be between 75% and 80% of its underlying earnings per share. The stock has climbed up by 13.56% in the past six months and has further room for growth. Hence, we recommend to “Hold” the stock at the current market price of $1.00

AX1 Daily Chart (Source: Thomson Reuters)

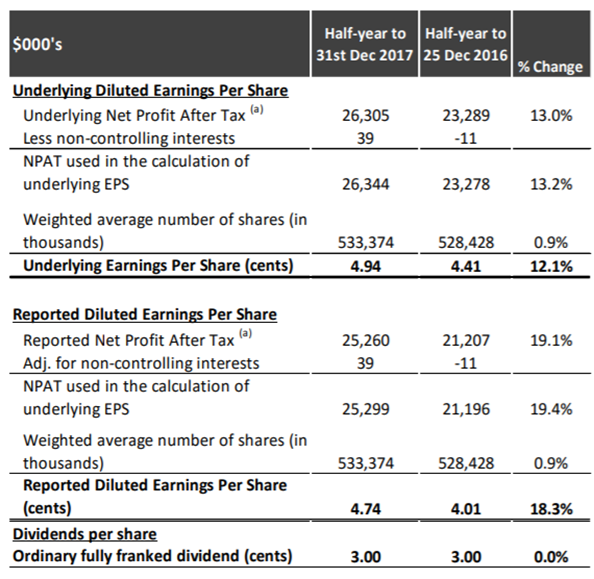

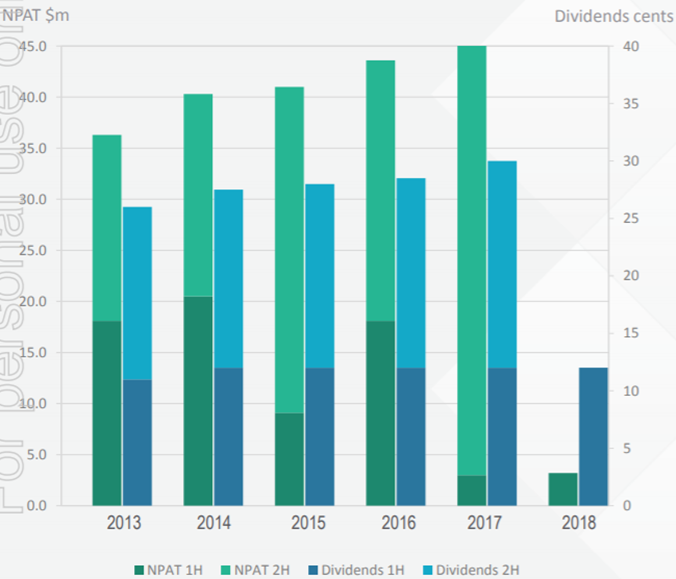

Cedar Woods Properties Limited (ASX: CWP)

CWP Details

DRP Policy to recommence: Cedar announced about a $35 million of temporary increase in its corporate finance to facilitate the completion of Target Australia’s new headquarters at Williams Landing in Victoria. The increase in the facility will remain in place until the settlement of the sale of the project is completed which is expected in mid FY19. ANZ and Bank of Western Australia, a division of Commonwealth Bank of Australia are providing the corporate facility on a joint basis. This increased the corporate facility limit from $205 million to $240 million and provided Cedar Woods with additional funding capacity for existing operations, for ongoing development of its projects and for future acquisition. Cedar Woods announced in June 2017 that it had agreed to pre-sell the building to Centuria Property Funds Limited for $58.23 million. Under the terms of sale, Cedar agreed to continue to develop the eight-story building which remains on track for handover and for settlement which is expected to complete in mid FY19.

Dividend Performance (Source: Company Reports)

The Group resolved to recommence the Dividend Reinvestment Plan and Bonus Share Plan. The plan will apply for the forthcoming interim dividend which will be payable on 27 April. The Board declared a fully franked interim dividend of 12 cents per share and the Board intends to maintain the policy of distributing approximately 50% of full year net profit to its shareholders via dividends. The share price rose by 11.31% in the past six months and we have a “Hold” recommendation at the current market price of $6.00

.png)

CWP Daily Chart (Source: Thomson Reuters)

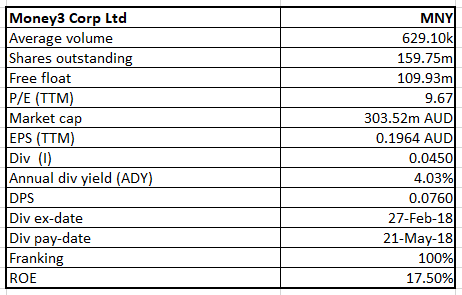

Money3 Corporation Limited (ASX: MNY)

MNY Details

Continued growth opportunities: MNY released its H1FY18 performance and recorded a half yearly revenue of $60.4 m, which is up by 16.8% on a year on year basis. It also declared a half-year dividend of 4.5c which is up by 80% as compared to same period in the prior year. Bad Debts were 2.7% of the gross loan book which was slightly up from 2.5% in H1 FY17, which is within the forecast range of 5-6% annually. 3 branches were closed during H1FY18. Earnings per share was 9.8 cents and the Directors declared an increased interim Dividend of 4.5 cents per share which is up by 80% on a year on year basis. Increased cashflows combined with new finance facilities will allow the company to pay dividends at the higher end of the stated pay-out range of 30-50%.

Dividend Performance (Source: Company Reports)

The company continues to explore ways of releasing excess franking credits held by the company to the shareholders. The share price rose by 28.38% in the past six months and we give a “Hold” recommendation at the current market price of $1.85

.png)

MNY Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...