Australia and New Zealand Banking Group Limited

Strong Performance on the Sustainability Parameters: Australia and New Zealand Banking Group Limited. (ASX: ANZ) has announced via a release that Mr. Lee Hsien Yang will retire as a Non-Executive Director at the ensuing 2018 Annual General Meeting. He has served for more than nine years on the Board. Mr. Lee joined the Board in 2009 and has served as Chairman of the Digital Business and Technology Committee from the Year 2014.

The company has released its sustainability report for the FY 2018. As per the report, the bank has funded ~$11.50 Bn and facilitated in the low carbon and sustainable solutions, since the Year 2015. The company had a 32% representation of women in leadership roles. Moreover, the bank was ranked number one in the net promoters score as per the Australia and New Zealand Institutional Net Promoter Score.

The operating income for the FY 2018 rose by 2.23% on a YoY basis to reach at $19.83 Bn. This growth in income was achieved due to the traction seen in the retail deposits & also the home lending and business lending portfolios. Moreover, the performance looked sound on the back of higher other banking income.

The company for the FY 2018 has achieved net a cash profit of $6.5 Bn, down by 4.72% on YoY basis. This fall was witnessed on the back of the fact that there was degrowth in the Net Interest Income. Consequently, the group’s NIM’s were lower for the FY2018 due to growth in the lower margin liquid assets. Also, there were unfavourable changes in product mix. The introduction of major bank levy due to the implementation of recommendations of the royal commission aided the cause.

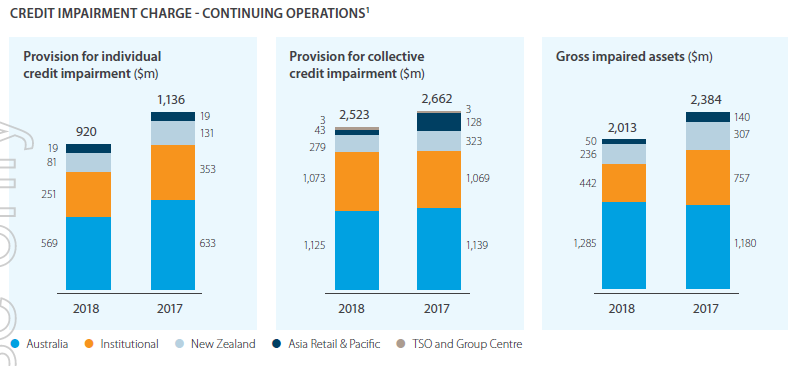

ANZ’s Provisions for Impairment (Source: Company Reports)

Meanwhile, the stock price has fallen by 12.42% over the past six months as on 18th December thus posing an attractive opportunity for the investors to acquire the stock at these levels. Hence considering the strong operating profits and the recent decline, we maintain our “Buy” recommendation on the stock at the current market price of $23.94 (up 1.055% on December 19, 2018).

Challenger Ltd.

Expansion in Distribution Network on Netwealth Platform- Key growth driver: Challenger Ltd (ASX: CGF) has via a press release lately stated that the premier global rating agency S&P Global Ratings (S&P) have recently completed their annual ratings review and affirmed the credit rating and outlook for Challenger Limited. The company was provided with a ‘BBB+’ rating along with a positive outlook.

Also, in a release lately, the company declared that Ms. Angela Murphy has been appointed as the Chief Executive Distribution, Product and Marketing. Ms. Murphy replaces Mr. Howes who has been appointed to the role of CEO and Managing Director commencing from January 2019.

The company recorded the second highest quarterly annuity sales with a figure of $1,171 Mn for the Q1 2019 exhibiting a rise of 7% on PCP. This rise was seen on account of the strong demand for secure income from the growing number of retirees with increasing retirement savings. Annuity sales are also benefiting from Challenger’s expanded distribution reach.

The company has maintained its earlier guidance to achieve growth in NPBT between 8%-12% on FY2018, also the company has remained firm to its 18% pre-tax ROE target. Also, the Normalised ROE is anticipated to rise in the FY 2019 on account of the higher levels of capital deployment from the equity placement in August 2017. Challenger has announced plans to further expand distribution by making its full range of annuities available on the fast-growing specialist Netwealth platform.

CGF’s Financial parameters (Source: Company Reports)

On the analysis front, the price-to-book multiple at which the stock trades at 1.7x, while the insurance industry trades at 1.97x, hence the stock seems undervalued from the net assets perspective. Meanwhile, the stock price has fallen by 20.37% over the past six months as on 18 December 2018, thus posing an attractive opportunity for the investors to acquire the stock at these levels. Hence considering the expanding distribution network & the undervaluation, we maintain our “Buy” recommendation on the stock at the current market price of $9.650 (down 2.03% on 19 December 2018).

Qantas Airways Limited

Improving Net Passenger Revenue & Cost Optimization: Qantas Airways Limited (ASX: QAN) has recently updated the market about the final buyback notice under its ongoing buy-back event wherein the group has bought back a total of 57,918,883 shares via on-market trade for the total consideration of A$ 331,999,993.99. Since this was an on-market buyback, the highest and the lowest price which was paid for the purpose of the buyback were reported at $6.30 and $5.18, respectively.

For the Q1 FY 2019, total revenue was up 6.30% on PCP to reach $4.41 Bn. This growth was driven by the net passenger revenue growth and capacity discipline. However, this growth was a bit offset by the rising fuel costs. The record revenue performance also helped partially offset a rise in non-fuel costs, such as higher commissions and the impact of a weaker Australian dollar.

.png)

QAN’s Key Financial Parameters (Source: Company Reports)

On the other hand, the company faces operational risk in the form of fuel price risk in term of rising fuel prices. In order to mitigate such risk, the company has hedged ~76% of its fuel for the FY2019 & 39% for the FY2020. the Group’s full-year fuel cost is now expected to be $4.09 billion compared with $3.23 billion for the financial year 2018. The company is expecting the group capacity for the FY 2019 to be flat, with the group domestic capacity slated to fall by 0.1 percent and the international capacity is expected to remain flat. The company expects to deliver the transformational benefits of around $400 Mn driven by the cost improvements which would be materializing in the 2H 2019. The sector is also slated to face extreme competition and margin pressures in the upcoming periods. However, the company believes that its market leadership position and the dual brand strategy will help to steer and face the dynamic market changes with requisite solidarity.

Meanwhile, the stock price has fallen by 15.08% over the past six months as on 18 December 2018, thus posing an attractive opportunity for buying as the stock trades at an attractive EV-to-EBITDA multiple of 3.5x. Hence considering the net passenger revenue growth & the cost optimization, we maintain our “Buy” recommendation on the stock at the current market price of $5.80 (up 5.072% on 19 December 2018.

Ramsay Healthcare Ltd.

Increasingly Ageing Population & Rising Healthcare Expenditures - A Growth Catalyst: Ramsay Healthcare Ltd. (ASX: RHC) has via a recent release stated that the company has appointed Ms. Alison Deans who will be joining the company’s board as a non-executive director. Ms. Dean has earlier held a range of board positions over the last 20 years, focused on technology and innovation. She is currently a non-executive director of Cochlear Limited and Westpac Banking Corporation.

For FY 2018, the company witnessed its EBIT expand by 6.8% on a YoY basis, to stand at $1.008 Bn. This was on the back of admissions growth rate being above the industry growth rate. However, this was partially offset by the affordability concerns and the negative focus on the private health insurance space. In the future, the company is committed to investing in the brownfield projects to meet the ever-growing demand generated as a result of the increasingly ageing Australian population. These investments are expected to contribute substantially to the FY 2019 earnings. The company expects the ongoing challenging operating conditions to continue across its all key regions & thus expecting a subdued FY 2019.

RHC’s Financial KPI’s (Source: Company Reports)

On the valuation front, the company is trading at an EV / Sales ratio of 1.5 times, which is attractive enough. Also, the ROE for 2018 stands at 16.80% which is decent enough considering the concerned industry. Meanwhile, the stock is down by 8.10% in the past six months as on 18 December 2018. However, considering the robust ROE and traction in demand driven by the ageing population, we maintain our “Buy” recommendation on the stock at the current market price of $53.870.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...