Commonwealth Bank of Australia

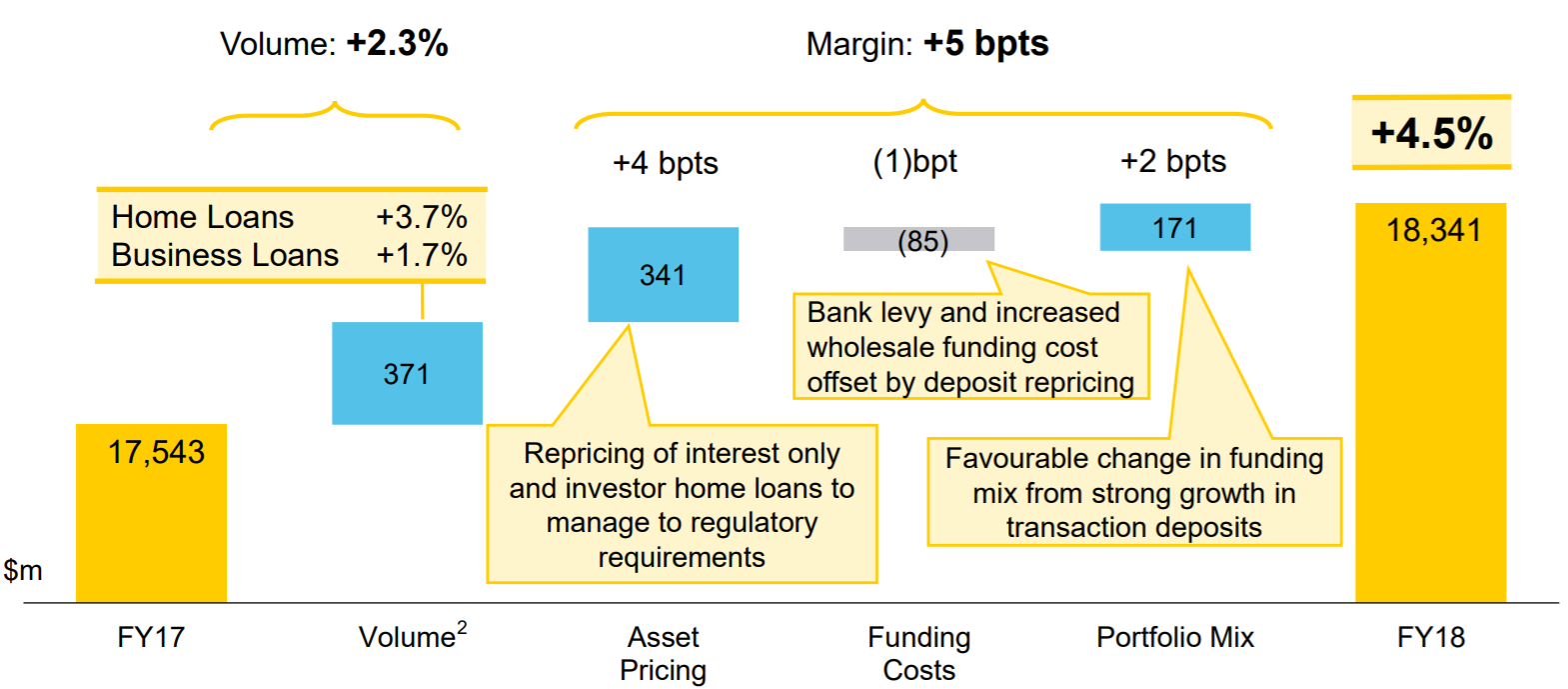

Streamlining Service Portfolio: Commonwealth Bank of Australia (ASX: CBA) has been taking decisions lately to narrow down business and become a simpler bank and have more streamlined service provider. Latest, the bank has decided not to offer self-managed super fund lending from the next month, including the fund operated by CBA-owned Colonial First State. Earlier, CBA sold its life insurance businesses including the Sovereign in New Zealand, Comminsure Life in Australia and BoCommLife in China. On the financial front, Net Interest Income, a significant metric for the banks has increased in FY18 to $18,341 Mn compared to $17,543 Mn in FY17. The bank has ceased its stake in Ausdrill Limited, Flexigroup Limited and offloaded shares in Elders Limited with voting power at 5.06% compared to 6.18% held earlier. The major concern for the investors at the current juncture is declining loan growth, in both Home and Business divisions. However, the major drop has come on the back of the company’s own portfolio rebalancing activity and intense competition from the non – banking institution. We believe that post restructuring process, CBA would be more focused towards offering better on margin services.

Net Interest Income (Source: Company Reports)

Meanwhile, the stock has generated 2.95% over past three months and looks poised to grow from the current juncture. Price has respected the long-term support level of $69.189 and rebounded from that level. Sighting the limited downside at current levels, the investors could take fresh entry in the stock. We, therefore, recommend ‘Buy’ in the stock at the current market price of $71.920.

Transurban Group

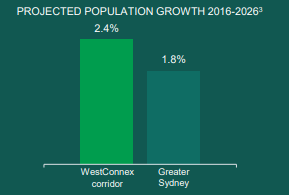

All Round Growth: Transurban Group (ASX: TCL) recently acquired 51% stake in Sydney’s WestConnex toll road, doubling its network in the largest city of the country. Strategically fit decision of acquiring WestConnex toll road and better performance across the Geographies make Transurban a buy candidate. In FY2018, the company saw its EBITDA increase in Sydney, Melbourne, Brisbane, and North America. WestConnex might take some time before starting to contribute to the revenues of TCL but the move would also cement the position of the company as one of the largest toll operators in the country. TCL’s approach and expertise towards owning and operating the toll roads would keep the competitors at bay. On the valuation front, Operating margin for FY18 was recorded at 29.7% in line with the industry average of 30.3%. Even though the net margin at 15% remains below the industry average, the company has improved from the previous year. TCL has consistently generated value for the shareholders with ROE for FY18 at 10.1% compared to 5.0% in FY18 and 10.8% industry average.

Projected Population Growth to support toll performance (Source: Company Reports)

Meanwhile, the stock has generated a negative YTD return of 7.25% but has managed to stay above the support level of $10.964. The price staged sharp V shape recovery from the low of $11.120 on decent volume. Further, the stock has already moved above its immediate resistance of $11.449 and looks good to stride further. We, therefore, recommend a ‘Buy’ in the stock at the current market price of $11.480.

Tabcorp Holdings

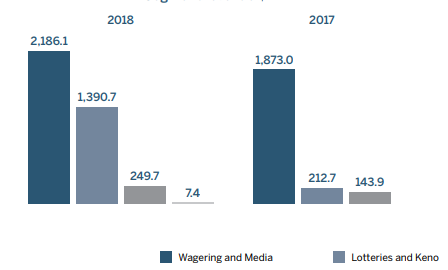

Exiting Loss-Making Business: Tabcorp Holdings Limited (ASX: TAH) posted stellar FY18 numbers and exited loss-making businesses such as Sun Bets and Luxbet. The consumer discretionary company is well positioned for growth as digitization ramps up across the country along with new product launches and licenses renewals. The company earned sustainable income in FY18 as all the major segments contributed to it.

Recently, Director Steven Gregg has increased stakes in the company, buying 7,000 ordinary shares at $4.80 per Ordinary Share. After posting negative margins and Return to shareholders last year, the company has this year returned in Black. Net margin has been positive and so has Return to shareholders for FY18 at 0.7% and 0.7% respectively. Operating margin, on the other hand, has increased by 6.3% compared to 4.5% in FY17.

Segment Revenue (Source: Company Reports)

Meanwhile, the stock has generated a return of 9.60% over past six months on the back of good results and divestment in loss-making businesses. The stock has continued its positive trend for quite some time and there is no sign of a reversal in the near term. The price is above its 21 and 50 days Double Exponential Moving Average (DEMA) suggesting the strength in the near term. We recommend a ‘Buy’ in the stock at the current market price of $4.940.

Scentre Group

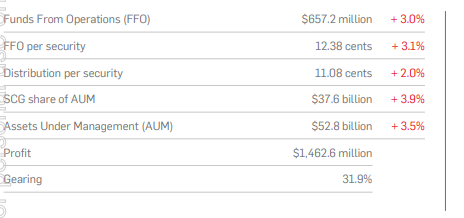

Existing and new businesses add to growth: Scentre Group (ASX: SCG) is a well-managed and run company which posted a profit in 1H FY18. Profit after tax for the period was reported at $1,467.7 Mn compared to $1,419.0 Mn in 1H FY17. Funds from operations registered a growth of 3% at $657.2 Mn in the 1H FY18. The company has invested in various new developments and generated good returns from the properties already up and running. Comparable Net Operating Income recorded growth of 2.5% in the first half, suggesting that the company earned good revenue from the existing businesses.

Half Year Performance (Source: Company Report)

The stock has generated positive return of 3.48% over past six months and has steadily moved upward from the support level of $4.076. In latest trading session, the price moved above to its immediate resistance of $4.180 on decent volume. Short term momentum of the stock looks intact with the price sustaining above its 21 days’ DEMA. Sighting Scentre’s capacity to generate revenue stream from the current operations and investment in the newer once, we recommend a ‘Buy’ in the stock at the current market price of $4.180.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...