Rhipe Limited

.png)

RHP Details

Healthy 1HFY18 Performance: On the financial front, Rhipe (ASX: RHP) delivered healthy revenue growth of 22% to $88,314 Mn in 1HFY18 from $72,451 Mn in 1HFY17. The topline spiked up by strong growth of subscription and support & services activities during the same period. Reported EBITDA stood at $2,762 Mn in 1HFY18, up 304% year on year (YoY). Profit after tax came at $1,077 Mn in 1HFY18, marking splendid growth on YoY basis. The rise in EBITDA and NPAT for the six months to 31 December 2017 was majorly due to significant investment in several key strategic initiatives such as operation expansion across South East Asia and Korea, investment in the Indirect Microsoft Cloud Solution Provider (CSP) program for Office365, and strategic investment in its core business to support the expansion of Microsoft’s Public Cloud Infrastructure platform. As a result of the continued improvement in operating results and strong cash position, the Board of Directors declared fully franked interim dividend of 0.5 cents per share. Moreover, the group announced share buyback event in August 2017 and acquired 3.4 Mn or 2.5% of its own ordinary shares from the market by end of 2017. Total cash outlay on the share buyback event incurred up to $2.3 Mn at an average buy back price of 67 cents per share.

.png)

Healthy Performance (Source: Company Reports)

The Board of Rhipe outlined that its Microsoft Cloud Solution provider (CSP) program continues to drive significant growth in public-cloud subscription business segment. The group has crossed 200,000 office365 user threshold during the month of February. The group’s CSP business has achieved an annualized run rate (ARR) of $34.6 Mn. The management guidance on operating profit is more than $7 Mn for FY18.Regal Funds Management Pty Limited, a substantial holder changed its holding in RHP since 23 March 18 from 13,412,249 of shares with 9.96 per cent of the voting power to 11,172,364 shares with 8.26 per cent of the voting power. Meanwhile, the stock price inclined by 38.9% in the past six months as at April 06, 2018. Based on strong Cloud momentum that continues to build across Asia Pacific (APAC), we give a “Speculative Buy” recommendation on the stock at the current market price of $ 0.910.

RHP Daily Chart (Source: Thomson Reuters)

Telix Pharmaceuticals Limited

.png)

TLX Details

Potential to Grow Further: Telix Pharmaceuticals Limited (ASX: TLX), is emerging as a leading player in the molecular targeted radiation (MTR) market. The group has recently provided an update on the company’s prostate imaging program (TLX-591), co-developed with ANMI SA, wherein, the group has filed Drug Master File (DMF) to US Food and Drug Administration which is an important step towards the product approval for the company. This DMF describes the Sterlite kit which is used to manufacture a clinical dose of prostate imaging agent (68Ga-PSMA-11).

.png)

On-going Development (Source: Company Reports)

On the financial front, the loss after tax of the Group for the financial year ended 31 December 2017 was $6,377,115. Total equity recorded at 31 December 2017 was $49,292,795. The Group had total assets of $51,093,728 and net assets of $49,292,795 as at 31 December 2017. Further, no dividend was recommended or paid during the period. In Q4FY17, the Group completed an initially public offering (IPO) of Telix shares and raised $50,050,000, and on 15 November 2017, the company issued 77,000,000 shares upon Listing with the Australian Securities Exchange. Since listing on ASX in November 2017, the Group has made great strides in its programs and operations, and achieved several key milestones such as completion of recruitment of skilled workers to deliver on clinical activities over the next 24 months, manufacturing establishment on TLX-101 (brain) and TLX-250 (renal) program, Orphan drug application for TLX-250 therapy filled in US and pending in the EU, and several key academic relationships for indication expansion and new clinical application areas. Meanwhile, TLX stock has risen 9.62% in one month as on April 06, 2018; and given the potential into the business and on-going development, we put a “Speculative Buy” recommendation on the stock at the current price of $ 0.580.

.png)

TLX Daily Chart (Source: Thomson Reuters)

Energy One Limited

.png)

EOL Details

Robust Performance to continue: The principle activity of Energy One Limited (ASX: EOL) during the latest half year was development and supply of software services to energy companies and utilities. Operating revenue and other income grew by 75% to $5.02 Mn in 1HFY18 on the back of strong domestic performance and half year contribution of both pypIT and Creative Analytics Businesses. The percentage of recurring revenue was maintained and accounted to 66% of operating revenue. The recurring revenue target for F18 is ~70%. EBITDA margin remains strong at 27%, assisted by the higher margins associated with recurring-type revenues and the Creative Analytics business contributes materially to this. Furthermore, net profit before tax for the Group for the half year amounted to $0.95 Mn from $0.32 Mn in 1HFY17, marking YoY growth of 191%. NPAT for the half year amounted to $0.59 Mn from $0.13 Mn in 1HFY17.

.png)

Robust Performance Trend (Source: Company Reports)

This splendid performance is a result of strong topline growth of the company during the period. Given this successful track record, the group intends to continue to fund innovation and expansion while maintaining a stable domestic base. This includes new product development to meet market changes and to facilitate effective entry of products into chosen overseas markets. Given the nature of business, dependencies and project timing, the Group expects that full year performance will still be consistent in future. EOL stock has risen 36.59% in past six months as on April 06, 2018. The group’s directors have also been acquiring its shares, as noted recently. Based on expanded organic growth opportunities with many regulatory changes falling in place for the gas market,the stock looks to be a “Speculative buy” at the current price of $ 0.840.

EOL Daily Chart (Source: Thomson Reuters)

iSignthis Limited

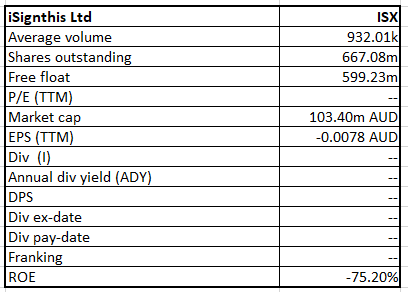

ISX Details

Rise in Users in Domestic and Overseas Market to support Topline Growth:iSignthis Ltd (ASX: ISX) recently announced that its Australian subsidiary iSignthis Money (AU) Pty Ltd has executed payment aggregation agreement with American express Australia (AMEX). As per this agreement, the Group will purchase AMEX processing at a pre-agreed wholesale Merchant Service Fee (MSF) rate, and then the group will on-sell to merchants under its usual Merchant Service Fee plus flat fee structure. This agreement contains provisions for AMEX direct MSF management of larger or pre-existing merchants enabled through ISXPay network. Besides this, the company also announced that the Group has extended the scope of its Paydentity solution to XM.com that includes provision of Chinese identity verification services as a standalone service. Furthermore, Electronic know your customer (eKYC) services have been provided to XM by the company since beginning of the March month. In this regard, the Group is exploring Chinese, as well as UK and EU market to meet AML/CFT know your customer (KYC) requirements. The company continues to extend its relationship with XM, and to build and grow revenue opportunity for both parties.

Increasing Footprint across Domestic and International Markets (Source: Company Reports)

Moreover, the group is engaged with a number of merchants across a range of industry verticals in the European market, Australia and other regions and we expect a steady growth of new customers throughout the year. The share price has been up by 3.33% in the past six months as at 06 April 2018; and given the potential for further growth, we maintain a “Speculative Buy” recommendation on the stock at the current price of $ 0.155.

.png)

ISX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...