JB Hi-Fi Limited

Growth in top line, however, seems a bit overpriced at this point given the challenges: JB Hi-Fi Limited (ASX: JBH) is a music and electronic goods retailer in Australia. The Company operates stores at sites located in most Australian States. Products include consumer electronics, car sound systems, music, and DVDs. The company has posted sales of $6854.3 Mn for the FY 2018 which implies a growth of 21.8% on a Y-O-Y basis driven by the hardware and services sale, however during the same period software services saw a decline due to the accelerated decline in the movie’s category. The NPAT for the same period stood at $233.2 Mn exhibiting a growth of 12.3%. FY18 dividend was up 14 cps to 132 cents per share fully franked and in line with the current Group dividend payout ratio of 65%. The board believes that the dividend payout ratio of 65% forms an appropriate balance between providing recurring income to the shareholders and reinvestment of the earnings for future growth.

Recently, the group released its Quarterly report for the quarter ended 30 September 2018 wherein the group achieved sales growth of 5.3% and 4.0% for JB HI-FI Australia, and New Zealand, respectively. Additionally, for FY19, the company has reaffirmed its sales guidance of $7.1 Bn comprising JB HI-FI Australia - $4.75Bn, JB HI-FI New Zealand - $0.22Bn; and The Good Guys $2.15 Bn.

Value Proposition: The company is trading at a TTM P/E multiple of around 11.70 times but witnesses retail related challenges. Also, the company’s dividend yield stands at 5.56%. Meanwhile, the stock price has marginally fallen over the past one month by 2.82%, however over the period of past six months the stock has given a modest rise of 4.62%. If we look at the YTD performance, the stock is down by 4.23 %, which shows a dismal performance on the exchange. The group is also under short-selling radar with over 19.449% short positions as on 6 November 2018 (as per ASIC or Australian Securities and Investment Commission). Hence, considering the above rationale, we maintain our “Expensive” rating on the stock at the current market price of $24.050.

.png)

JBH Top line trends (in $Bn) (Source: Company Reports)

Syrah Resources Limited

Heavy demand for the Li-ion batteries required by EV is expected to be the turnaround factor: Syrah Resources Ltd (ASX: SYR) is a mineral exploration company. The Company's projects provide exposure to graphite, vanadium, mineral sands, copper, coal, and uranium. The company has a market cap of $666.59 Mn as on November 12, 2018. As per ASIC or Australian securities and investment commission, as on November 06, 2018, SYR was shorted around 16.16%.

The company has through a media release stated that it has achieved two further sales milestones, the first is regarding the binding term sales agreement of 6kt of large flake natural graphite with “Qingdao Freyr” and the second is that it has successfully produced 98% fixed carbon (“FC”) grade graphite across all sizes in the flake circuit using standard flotation processes, and the first spot sale of 98% FC is to a Japanese customer. The above-mentioned installed layout to produce the FC grade graphite without the requirement of chemical purification provides it an outstanding commercial opportunity in terms of cost advantage.

For the quarter ended 30 Sep 2018, the company has achieved a production of 38.7kt which implies a growth of 83% versus Q2 FY18. During the same period, the sales turned out to be 20kt on the back slightly higher weighted realised price as compared to the previous quarter. The “Battery anode material” project site purchases & major supply input terms have been finalized, commercial production of impurified spherical graphite is expected by the year end.

Decent Liquidity & Cash flow position: The company has successfully completed the institutional placement and raised proceeds amounting to US$67.4 Mn and hence the resulting cash as on quarter ended September 30, 2018 was US$100.3 Mn. The net cash outflow for the above-mentioned period was US$21.6 Mn. Q4 FY 2018 net cash outflow forecast is US$ 23.6 million, and the company is targeting positive cash flows from operations at Balama site during Q1 2019.

.png)

Natural Graphite Market Demand/Supply Trends (Source: Company Reports)

The stock price has fallen over the past one month by 5.83%, also over the period of past 6 months the stock has seen a sharp decline of 37.82%. If we look at the YTD performance, the stock has almost halved and has declined 58.81%, which shows a dismal performance on the exchange. However,considering that the company is still into the expansion stage and incurring huge capex into its projects and is expected to achieve positive net cash flows in 2019, we maintain our “Hold” rating on the stock at the current market price of $1.945.

Orocobre Limited

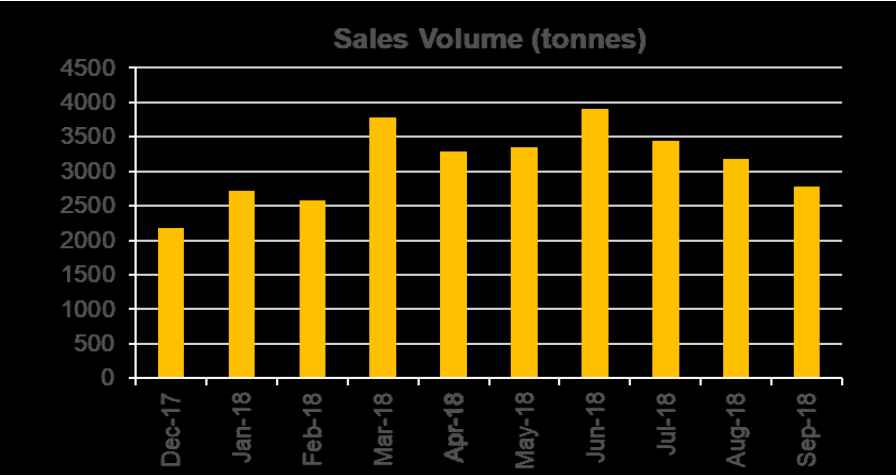

Topliner along with robust balance sheet:Orocobre Limited (ASX: ORE) is a mineral exploration company. The Company's primary objective is to develop lithium-potassium brine projects. Orocobre is focused on advancing its flagship Olaroz lithium-potassium brine project in Argentina. The production for the quarter ended September 2018 was 2,293 tonnes of lithium carbonate, and this implies a rise of 7% on previous corresponding period. The company has posted strong sales of US$ 32 Mn for the quarter, up 36% from previous corresponding period. As per ASIC or Australian securities and investment commission, as on November 06, 2018 ORE was shorted 15.799%.

Decent Liquidity Position: The company had an available cash balance of US$308.7 Mn, thanks to the increase in the average price received per tonne. This was after supporting the Advantage Lithium capital raise (US$4M), Cauchari JV expenditure and early expenses on the Naraha Lithium Hydroxide Plant. Including SDJ and Borax cash and project debt, net group cash came in at US$221.7 million. Following this, the company has a strong balance sheet with virtual debt-free position. Also, the company hasn’t distributed any dividends and hence investing in the positive NPV projects from the internal accruals. The stock seems to have been beaten down a lot even though it has got strong fundamental backing.

ORE Sales volume trends (in tonnes) (Source: Company Reports)

Further, for FY19, Orocobre expects full year production to be higher than the previous year. December quarter production is expected to be materially higher than the September quarter. Meanwhile, the stock price has risen over the past one month by 5.06%, however over the period of past 6 months the stock has fallen drastically by 22.83%; and also if we look at the YTD performance, the stock is down by 37.46 %. However, fundamentally the company is sound enough which is evident from its projects and balance sheet, thus considering the above rationale we maintain our “Buy” rating on the stock at the current market price of $4.52.

Galaxy Resources Limited

Global EV sales volume to drive the growth: Galaxy Resources Limited (ASX: GXY) is a global lithium company, with a diverse project portfolio, consisting of both hard rock and brine assets spanning Australia, Canada and Argentina. As on the quarter ended September 30, 2018 the firm had US$54.7 Mn in cash thanks to a healthy cash margin of US$ 411 per dmt and constant receipts from customers. The company has zero debt on its balance sheet. This strong cash balance is constantly supporting the funding required for ongoing project development and optimization initiatives. The company has posted sales of 29,555 dmt of spodumene concentrate. The NPAT for the 1H 2018, stood at US$11.5 Mn and EBITDA stood at US$42.4 Mn exhibiting a growth of 331% and 2,878% respectively on a Y-O-Y basis. As per ASIC (as at November 06, 2018), GXY was shorted 15.338%.

GXY financials (Source: Company Reports)

Meanwhile, the stock price has modest returns over the past one month of 6.30%, however over the period of past six months the stock has fallen by 17.43%. Also, if we look at the YTD performance, the stock is down by 30.23%. Hence, we can see that that the stock is going through a phase of consolidation and thus considering the robust balance sheet and bright prospects of volume growth due to surge in the production of EV, we maintain our “Hold” rating on the stock at the current market price of $2.75, up 1.85% on November 12, 2018.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...