Westpac Banking Corp

Offering the best discounts for first time to attract new customers: Westpac Banking Corp (ASX: WBC) had declared an unchanged interim dividend of 94 cents per share. For the 1H 2018, the Federal Government bank had levied cost on Westpac of about $186 million pre-tax. The levy is paid out of retained earnings and is equivalent to 4 cents per share. On the other hand, WBC in order to attract new borrowers has slashed as much as 110 basis points (bps), which is a promotional strategy for spring (a traditionally busy time for the housing market). The bank is offering the best discounts for first time in the headline rate of 4.18% for the first five years, before the discount narrows to 80 bps. Therefore, the new housing customers can borrow on rates as low as 3.08%. However, the banks are facing increased funding costs on the back of rising global bond yields and they have to protect their margins by increasing the mortgage rates. Meanwhile, WBC stock has fallen 4.52% in three months as on September 25, 2018 and is trading at a low P/E of 11.38x. The interim report of Royal Commission is expected to come this week, which will pave the stock’s movements. As of now, the fundamentals look strong and we give a “Buy” recommendation on the stock at the current price of $27.810.

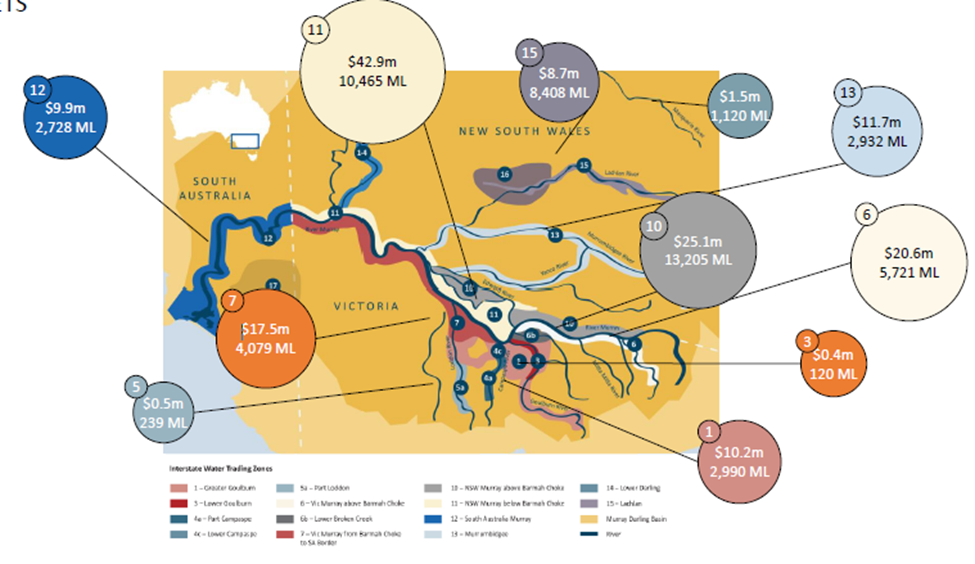

Duxton Water Ltd

Acquisition pipeline of a further $ 25.1 million of water entitlements: Duxton Water Ltd (ASX: D2O), operator of the only pure water entitlement listed business in the world, saw its stock rise by 14.71% in three months as on September 25, 2018. The company currently owns and is managing $160.4 million in water assets comprising of entitlements and allocation, but excluding contracted ones. As on 14 September, 2018, the company has a further $25.1 million (10,258 ml) water entitlements within the pipeline for further acquisition. The company is getting profit substantially from the current water drought, that are being faced by regional Australia. Moreover, D2O had declared dividend of 2.5 cents per share, which was payable on 14 September 2018. The dividend was franked to 75% for Australian Taxation purposes. Since November 2017, the company has paid the shareholders a total of 7.2 cents plus franking. Meanwhile D2O is trading at a very high P/E. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $ 1.400 and will review the stock for a better entry opportunity.

Pro forma Portfolio of Entitlements as at 14 September 2018, excluding Contracted Assets (Source: Company Reports)

National Storage REIT

Funds Raised: National Storage REIT (ASX: NSR) has risen 3.24% in terms of stock price in three months as on September 25, 2018 after the company has successfully raised $175 million, comprising a $50 million Institutional Placement, and a $125 million pro-rata accelerated non-renounceable Entitlement Offer (including both institutional and retail). The company has planned to use the funds raised to strengthen the company’s balance sheet, reducing the gearing levels to 30% from 38%, and also to offer longer-term funding flexibility for its consolidation strategy and pursue further growth through the identified strategic initiatives. Meanwhile, NSR for FY18 reported 12.5% growth in the underlying earnings to $51.4 million, driven by strong storage revenue growth of 18% to $124.6 million. During FY18, NSR settled $155 million in high quality assets across Australia and New Zealand, increased the total assets under management by 23% to $1.4 billion, and reaffirmed their position as the largest self-storage owner-operator in Australasia. Further, NSR has declared the final distribution of 4.9 cps bringing total FY18 distribution to 9.6 cps. Additionally, for FY 19, NSR expects EPS to be in the range of 9.6 - 9.9 cps and FY19 underlying earnings to be in the range of $62.5 – $64.5 million. Therefore, based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 1.655, while it has a year on year dividend growth rate of 4.3%.

Adairs Ltd

Strong FY 18 Performance: Adairs Ltd.’s (ASX: ADH) stock has risen 13.72% in three months as on September 25, 2018 after the company for FY 18 reported 18.8% rise in sales to $314.8 million and 45.4% growth in net profit after tax to $30.6 million. There is 14.3% rise in like for like sales driven by increased transaction volume, with more customers choosing to shop at Adairs and the company’s existing customers, comprising of the growing Linen Lovers membership base, shopping more frequently. Gross profit was up 20.9% to $189.6 million on the back of an improved product offering and continued retail execution success. Additionally, ADH for FY 19 expects total stores to be between 171 and 173, sales to be between $345 million and $360 million, gross margin in the range of 59% and 61%, EBIT to be between $47.5 million and $51.5 million and capital investment to be between $8 million and $10 million. In addition, ADH had declared the final FY18 fully franked dividend of 8.0 cents per share. Therefore, Adairs’ total FY18 dividend grew 68.8% to 13.5 cents per share fully franked. Meanwhile, ADH stock is trading at a reasonable P/E of 13.97x. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.540, while it has a year on year dividend growth rate in double digits.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...