Insurance Australia Group Ltd

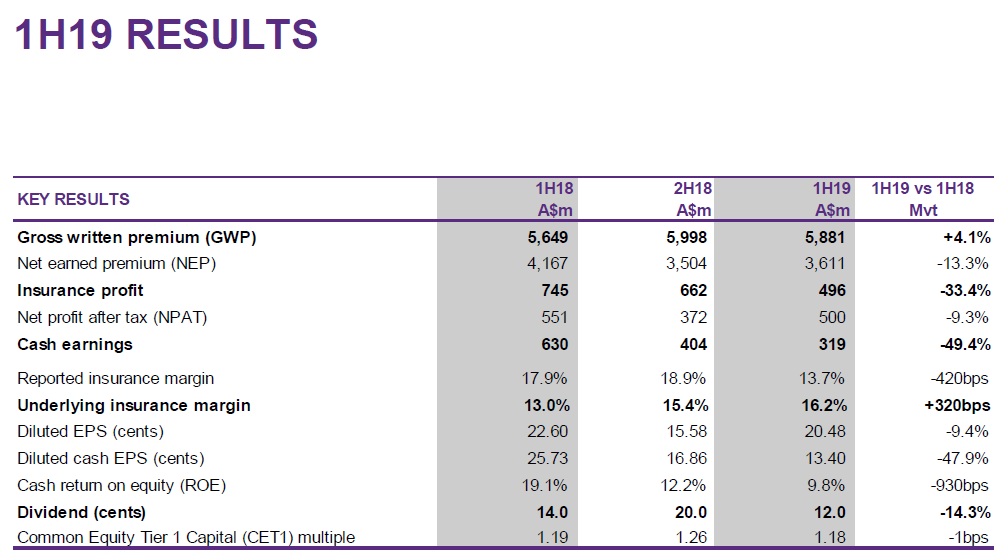

Robust Margin Guidance: Insurance Australia Group Ltd (ASX: IAG) has recently reported its 1H19 underlying results. Their performance was broadly in line with the expectations put forth by the management at the beginning of the year. The company registered a Gross written premium (GWP) growth of 4.1%. This growth was largely rate-driven & was amplified due to the by a favourable foreign exchange translation effect in New Zealand. There was an Improvement in IAG’s underlying insurance margin, which increased to 16.2% for the current period from 15.4% in 2H18. This growth was witnessed on the back of benefits from IAG’s optimisation program, earned rate increases (inflation adjusted), this growth was partially offset by the increasing regulatory and compliance costs. Moreover, the Board has determined to pay an interim fully franked dividend of 12.0 cents per ordinary share on 20 March 2019 with a record of 13 February 2019.

Going further, for FY 2019, the company had provided GWP growth guidance ranging from 2-4% & margin guidance ranging 16%-18%.The GWP growth is expected on the back of the rate increase across personal & commercial classes offset by a slight decline in commercial volumes. The margin growth is anticipated on account of an improvement in the pre-tax profit and no material movement in exchange rates. It's been anticipated by the management that ~$100m of pre-tax improvement will be derived from the optimisation program in FY19, compared to FY18.

IAG’s Key results & comparatives (Source: Company Reports)

The company is trading at a TTM P/B multiple of around 2.90 times, while the insurance industry median is 1.90 times; thus, we consider that the stock is trading at higher levels at this price point, considering the book assets that it has on its balance sheet.

Meanwhile, the stock price has risen over the past one month by 10.35% as on February 8, 2019. Hence, considering the expected net benefits which are to be realised in FY19 & strong margin guidance subject to the higher P/B ratio, we advise the investors to have a wait and watch stance over the stock at the current market price of $7.57 as on February 8, 2019.

Navitas Limited

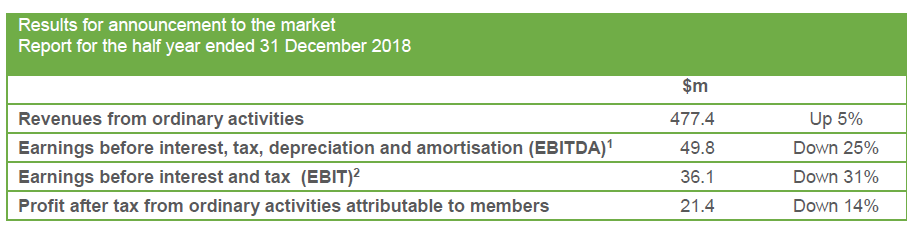

Decent outlook & strong growth in UP & SAE Businesses: Navitas Limited (ASX: NVT) has entered into an agreement with Lancaster University to help them establish and manage their new campus in Leipzig, Germany. Before Lancaster University, it had agreements with The Hague University of applied sciences and The University of Twente, which are some prestigious universities in Europe (in the Netherlands). FY19 Pro forma EBITDA guidance of $148 Mn-$153 Mn has been maintained from the continuing operations by the management. The firm expects strong enrolment growth in the University Partnerships division. It is also of the view that the medium to long term growth shall be delivered by the contract renewal and business development initiatives, in the backdrop of Growing global demand for education services. For the 1H 2019, the company posted revenue from ordinary activities of $477.4 Mn vis-à-vis $477.4 Mn in HY18. This growth was mainly on the back of the robust revenue growth witnessed in their UP and SAE business, following FY18 rationalisation.

1H19 Financial Highlights (Source: Company Reports)

On the financial metrics front, the company has reported EBITDA margins of 21% for the 1H19 down from 22% reported in HY18. The contraction was seen on account of the Investment in the sales transformation program & the recruitment of additional teaching staff.The company reported ROE of 97.4% above the industry median of 8.0% generating more returns for the shareholders. Meanwhile, the stock price has risen by 8.09% in the past three months as on 8 February 2019. Thus, considering the decent outlook and strong growth in UP & SAE Businesses along with better returns to shareholders and reaffirmed FY19 EBITDA guidance, we maintain our “Hold” recommendation on the stock at the current market price of $5.61.

Credit Corp Group Limited

Strong book growth will produce increased revenues:Credit Corp group limited (ASX: CCP) has recently reported its 1H2019 numbers. As per the release, the company delivered a 13% rise in the NPAT to reach at $33.60 Mn. This growth was predominantly on the back of strong growth from the rapidly growing consumer lending and US debt buying businesses and a resilient result from the core Australia & New Zealand debt buying operation. Based on decent performance in 1HFY19, the Board of Directors declared fully franked interim dividend of 36 cents which will be payable on 15 March 2019 with a record of 5 March 2019.

The firm improved its FY19 outlook, on the back of US FY19 contracted purchasing pipeline, which has increased to A$74m, up 23% on FY18 investment. Now it expects, the NPAT to be in the range of $69 - $70m & the EPS to be in the range of 144 - 146 cents. This growth would be in conjunction with the growth in Net lending volumes, which are expected to be ranging $50m - $55m. On the financial metrics front, the company is trading at a TTM P/BV multiple of 3.40x while the banking service industry median stood 1.3x. Moreover, the stock is providing a less dividend yield of ~3.3% vis-à-vis 6.30% as per the industry median. Thus, the company seems to be trading at a higher price point at these levels.

CCP’s Financial Highlights (Source: Company Reports)

The stock price thus had risen in the last one year and was up by 7.35 per cent and further up by 13.88per cent in the past three months. The stock is trading slightly toward the higher level, showing “Expensive” at the current juncture. We, therefore, suggest investors that they should keep a close “Watch” on the stock at the current price of $ 21.90 and wait for further growth catalyst.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...