.png)

Stocks’ Details

Evolution Mining Limited

Generating Strong Cash Flow: Evolution Mining Limited (ASX: EVN) is engaged in the gold mining business with its projects in Australia and New Zealand. The company in its March 2019 quarterly report updated that the group operating mine cash flow stood at A$168.3 million, with the group net mine cash flow of A$107.8 million including record net mine cash flow from Ernest Henry of A$59.5Mn. The bank debt was reduced by A$25.0 million to A$330.0 million. The net bank debt stood at A$74.2 million for the period as compared to A$41.4Million on 31 Dec 2018.

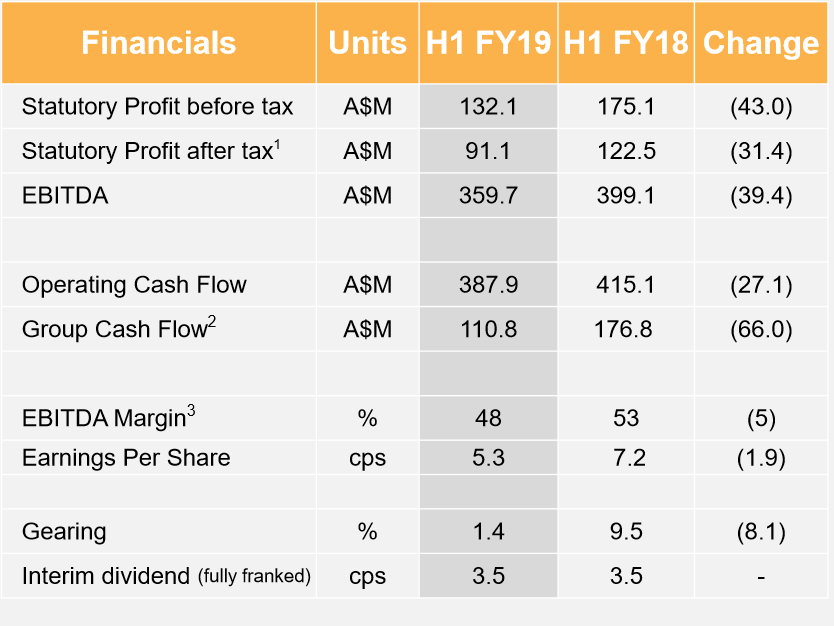

The statutory profit after tax for H1 FY19 stood at A$91.1 millionas compared to $122.5 million compared to the prior corresponding period. Decline in profit was primarily driven by non-cash impact items.

Key Metrics (Source: Company Reports)

The company is maintaining a strong balance sheet with a cash balance of A$313.6 million for H1 FY19 as compared to $163.5 million in the prior corresponding period, a significant increase of ~91.8%. Current ratio and quick ratio substantially rose from 1.7x and 0.86x to 2.31x and 1.42x respectively, in 1HFY19 over the prior corresponding period.

What to Expect From EVN: Going Forward, the companyexpects to produce in excess of 700,000 ounces of gold for at least the next three years.All-in sustaining costs are expected to remain relatively constant throughout this period of 3 years enabling the business to prosper even in weaker gold price environments. EVN is likely to witness higher capex in FY19 due to investment in significant projects at Cowal, however, it is expected to decline from FY20 onwards. Further, the group maintained FY19 production guidance of 720,000 – 770,000 ounces at an AISC of A$850 – A$900 per ounce, with the June 2019 quarter production guidance at 190,000 – 195,000 ounces.

Consistent operational performance along with the strong financials reported for the quarter on the back of reduced debts and higher cash flows for the company augurs well for a robust performance going forward. EVN exhibited strong fundamentals including higher organic growth on the back of increasing gold mineral and ore resources. The stock is trading at P/E multiple of 23.08x which is lower than the peer median of 26.25x. The EV/EBITDA of 7.89x, currently below the industry median multiple of 8.88x shows that the scrip is undervalued.Hence considering the aforesaid parameters, we maintain our “Buy” recommendation on the stock at the current market price of $3.230 per share (up 2.215% on 8 May 2019).

Saracen Mineral Holdings Limited

Strong quarterly performance: Saracen Mineral Holdings Limited (ASX: SAR) is into gold mining. The key assets of the company include Carosue Dam and Thunderbox with long lives and extensive growth potential.

Cash Position March Quarter 2019 (Sources: Company Reports)

The underlying net profit after tax for six months to December 31 stood at A$43.5 million, an increase of 17% from the previous corresponding period of A$37.2 million on the back of a 15% jump in sales revenue to A$281.9 million and increased gold sales of 167,0952 ounces.

The current ratio marginally increased from 2.62x in 1HFY18 to 2.64x in 1HFY19. The EBITDA margin and the net margin stood at 37.1% and 15.2% respectively in 1HFY19, which is significantly higher as compared to the industry medians.

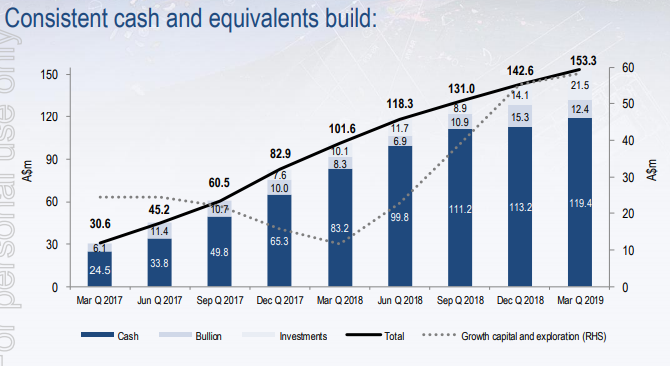

The cash & cash equivalents stood at A$153.3 million for the quarter ended, up from A$142.6 million as of 31 December 2018, despite significant spending on growth capital and exploration.

FY19 Guidance: The FY19 production guidance by the company remained at 345-365koz. With a seven-year production outlook, the company expects the organic production growth to 350kozpa as the standard with an upside opportunity to 400kozpa. The seven-year production outlook will be revised in the September quarter of 2019.

The stock is currently trading at $2.920, with a market capitalization of ~$2.31 billion. The stock has yielded a return of 14.63% over the last six months. Robust fundamentals with consistent growth in cash and cash equivalents, record gold production from Thunderbox operations, spending on exploration and growth lead us to recommend a “Buy” rating on the stock at the current market price of $2.920 (up 3.546% on 08 May 2019).

Resolute Mining Limited

Record Production From Syama: Resolute Mining Limited (ASX: RSG) is into gold mining and exploration with its key projects at Ravenswood, Syama and Bibiani.

The March 2019 quarterly updates highlighted the key achievements of the company with gold production up by 33% to 98,105oz for the quarter. The All-In Sustaining Costs were down by 24% to A$1,039/oz (US$740/oz). The Syama site achieved a record production of 84,552oz, an increase of 50% on the prior quarter. The company signed New Syama Mining Convention and it has been awarded the Mining Permit. The company is in preparations for the listing on London Stock Exchange.

FY18 Highlights (Source: Company Reports)

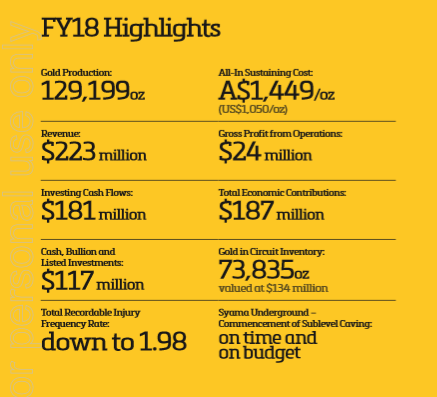

Revenue for FY18 was $223 million from gold sales of 128,275 ounces at an average realised price of A$1,734/oz (US$1,253/oz).The company reported a Net Loss After Tax of $5 million which was inclusive of an adverse movement in the valuation of net realisable inventory of $29 million offset by $15.5 million of unrealised foreign exchange gain on intercompany loans.

Resolute continued to invest heavily in the business in FY18 with capital expenditureson development, property, plant and equipment totalling $175 million and exploration and evaluation expenditure of $10 million.

As at 31 December 2018, the cash, bullion and listed investment position for the company was $117 million, comprised of$39 million held in cash, 22,786 ounces of gold valued at $40 million and investments valued at $38 million.

Guidance For June 2019: The company is reaffirmed its guidance for the 12 months to 30 June 2019 of 300,000oz at an AISC of A$1,280/oz (US$960/oz). Resolute will issue new production and cost guidance in July 2019.

The company has ~758.09 million shares outstanding with the market cap of ~$833.9 million, and an annualized dividend yield of 1.82%. During the past six months, the stock has generated a positive yield of 11.11%. It reported a lower EV/EBITDA of 5.6x as compared to the Metal & Mining industry average of 20.5x showing that the stock is undervalued.

Fundamentally, the company is well-positioned for further growth going forward, considering the strong production numbers achieved during the March quarter, robust cash balance and strong revenue in FY18 supported by substantial capex. Hence, considering lower than industry EV/EBITDA multiple with decent fundamentals, we give a “Buy” recommendation on the stock at the current market price of $1.120 (up 1.818% on 8 May 2019), expecting a better performance going forward.

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...