Scentre Group

Decent FFO growth guidance: Scentre Group (ASX: SCG) disclosed that Mark Bloom would retire from his role at the Group’s AGM in April 2019 and henceforth Elliott Rusanow will be appointed Chief Financial Officer on Mark’s retirement. The company had also advised that the AGM of Scentre Group Limited will be held on 4 April 2019 at 220 Pitt Street Sydney NSW. For the quarter ended 30 September 2018, the company had reported an occupancy rate in terms of portfolio leased of more than 99.50%. This high occupancy rate was on account of the rising demand for high-quality retail space that enjoys high traffic flow. The group’s total in-store sales witness a rise of 1.80% for the nine months ended 30 September. Also, the majors in-store sales were up 1.5% for the nine months and 1.3% for the year. This growth in the In-store sales was witnessed on account of the elevated customer experience, unique product offering and maintaining its position as the premium location for the retailers to succeed. Going forth, the company has reiterated its guidance for the 12-month ending 31 December 2018 of growth in Funds from operation (FFO) at the rate of 4%. The distribution for 2018 has been forecasted to be 22.16 cents per security.

.png)

SCG’s speciality In-Store sales growth (In %) (Source: Company Reports)

Meanwhile, the stock price has increased by 3.13% over the past three months as on 4 February 2019. However, considering the stable real estate property prices in its operational geographies, high occupancy rate along with growing sales in 3Q18, and decent FFO growth guidance for FY18, we maintain our “Buy” rating on the stock at the current market price of $4.01 (up 1.519% on 05 February 2019).

Reliance Worldwide Corporation Ltd

Robust EBITDA Guidance: Reliance Worldwide Corporation Ltd (ASX: RWC), has shown consistency with its earlier FY2019 EBITDA guidance, which they believe would be in the range of $280-$290 Mn. The higher EBITDA margins of circa 53%-55% are expected on account of the earnings contribution from John Guest, accumulation of synergy benefits & cyclical commodity costs which will help reduce the cost of goods sold in 2H FY2019.

However, these EBITDA margins are susceptible on account of non-occurrence of a freeze event in the USA. Hence, if the freeze event does not take place in the Feb-March 2019, then the result could be negatively impacted by between 1.5% and 3.0%.

For FY 2018, the EBITDA (before contribution from John Guest) was clocked at $150.90 Mn, up by 25% for the year. This was on the back of the strong sales witnessed across the product segment, a better product mix, scalability and improvements in the procurement process.

.png)

RWC’s FY 2018 Financial Performance (Source: Company report)

On the analysis front, the company has deleveraged its balance sheet, as the debt-equity has reduced to 0.50x from the levels of 1.32x reported in the FY2017. Moreover, the company delivered robust FY18 EBITDA margins of 17.60% depicting the efficiency gained through operational leverage. Meanwhile, the stock price has risen 7.31% in the last one month as on 4 February 2019 and is trading close to lower level. Hence, considering strong EBITDA guidance along with the deleveraging of the balance sheet and decent EBITDA margins for FY18, we reiterate our “Buy” recommendation on the stock at the current market price of $4.73 (up 0.638% on 05 February 2019).

Westpac Banking Corporation

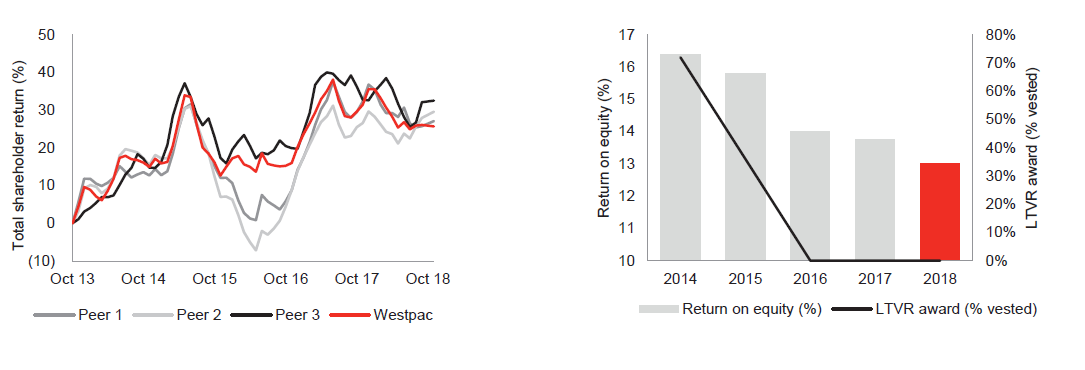

Robust Net Interest Income:Westpac Banking Corporation (ASX: WBC) has disclosed that it will take the time to consider the 76 recommendation which has been proposed by The Royal Commission. The company assured that it has already taken major significant steps when it came to address some of the very prominent issues such as dealing with customer complaints and leading the industry in moving away from grandfathered commissions.

WBC’s Total shareholder return and ROE (Source: Company Reports)

As per the recent 3 pillar report, CET1 came in at 10.63% as at 30 September 2018. This was an improvement of 13Bps from the levels at 31 March 2018. The improvement in the capitalisation was on account of the increase in cash earnings & conversion of preference shares to common equity. On the financial metrics front, the company has Net Interest margins of 2.13% as compared to the 1.94% which is the Industry median. This shows that the bank has invested its funds more effectively as compared to the overall banking sector. Also, on the valuation front, the bank has got a higher dividend yield of 7.56% as compared to the banking industry median of 6.40% which shows the stock still has got enough value left at these levels. Meanwhile, the stock price has fallen by 14.68% over the past six months as on 4 February 2019, thus posing an attractive opportunity for the investors to acquire the stock at these levels. Hence, considering the robust NIM’s & strong Dividend yields, we maintain our “Buy” recommendation on the stock at the current market price of $26.70 (up 7.358% on 05 February 2019).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...