QBE Insurance Group

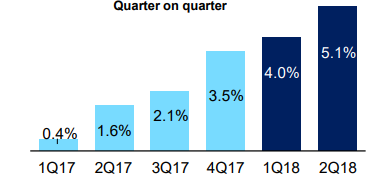

Growth Across Markets: QBE Insurance Group Limited (ASX: QBE) posted healthy numbers in 1H FY18 with the net profit coming in at A$358 compared to A$345 Million in 1H FY17. The company witnessed pricing momentum across the geographies including North America.

Premium Rate Growth (Source: Company Reports)

Improved attritional claims ratio in Australia and New Zealand, better accident year COR in Europe and progress in North America are working in favor of the company. While Australia, New Zealand and Europe are strong growth regions for the company, progress in Asia and North America are notable. To cut down the losses and non-core assets, the company sold its Latin American operations to Zurich Insurance and exited from the North America personal lines.

Stock Performance: The stock has performed well over past six months generating the positive return of 8.40%. At the current juncture, the stock looks positive on the chart holding its short-term support levels and moving higher. Sighting the positive developments and growth across the geographies, we recommend ‘Buy’ in the stock at the current market price of $11.030 while some concerns over natural calamities across the US have been noted.

Boral

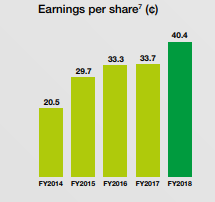

Headwater Business Drives Growth: Boral Limited (ASX: BLD) posted good numbers for the FY2018 with revenue coming in at $5,869 Mn compared to $4,388 Mn in FY 2017. The company did perform well with higher Earnings per share at 40.4 cents per share and increased rate of dividend.

EPS Growth (Source: Company Reports)

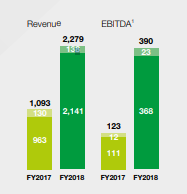

In FY18, the company successfully integrated its Headwaters Business into Boral North America. Boral Australia contributed significantly to the revenue, but it was North America where the maximum variance was witnessed from last year in terms of both revenue and EBITDA on the back of additional earnings from the Headwater business. Moreover, in the United States, the company has strong footing in fly ash and building products providing winning opportunities to grow.

Boral North America A$ m (Source: Company Reports)

Stock Performance: The stock has generated negative return of 8.50% over past six months but has turned positive over last three months. Overall, the growth prospects of the company look good with North America now contributing majorly to the revenue with Australia already being a strong contributor. The 14-day relative strength indicator looks in tandem with the price movement not suggesting any significant diversion. We therefore recommend ‘Buy’ in the stock at the current market price of $6.910 while the group may be in demand at the wake of the environmental challenges in the US.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...