Cash Converters International (CCV)

In today’s daily we cover Cash Converters International (CCV). The company recently announced that its class action in New South Wales has been settled. The settlement provides for Cash Converters to pay $20 million into a fund for distribution to the members of its class. Class members comprise borrowers in New South Wales who took loans from Cash Converters subsidiaries and franchisees during the period 1 July 2010 to 30 June 2013. Cash Converters will also pay legal costs capped at $3 million. Any part of the distribution fund which remains after efforts to contact and pay class members have been exhausted and after payment of the fund administrator’s costs, will be repaid to Cash Converters. The company also recently announced its March quarterly update whose key highlights were an increase in revenue of approximately 9% and an increase in EBITDA of approximately 12.1%, on the previous corresponding period.

The solid operations of Australian business (increase in EBITDA of 16.5%), was negatively impacted by poor performance of UK business (EBITDA down 94.5%). The division financial services administration showed a maximum increase of 31.3% while the division financial services personal loans showed the next best increase of 18.5%. The maximum decline was seen in the division Green light auto of -320%, as compared to the previous corresponding period.

Australian personal loan book growth (Source - Company reports)

Australian personal loan book growth (Source - Company reports)

In financial services the loan book of company was at $110.5 million as on 31

st March 2015 (representing a growth of 10.2% on the previous corresponding period). The personal loan book is down 4.5% from the 31

st December 2014 balance of $115.7 million, due to the traditional seasonally low advance period from January through March. The bad debts written off or provided for, for the three months ending 31 March 2015, were $3 million higher on the previous corresponding period.

In other divisions the corporate store revenue of $ 46.7 million was up 8.2%, on the previous corresponding period. This was driven by ongoing expansion of corporate store network in Australia and EBITDA was up 1.4% on the previous corresponding period. In the Green Light Auto division, EBITDA for the quarter was a loss of $694,260 million as compared to a loss of $165,403 loss in the previous corresponding period. A number of issues contributed to the loss, including the additional investment and overhead from opening a new distribution outlet in New South Wales, the departure of National Sales Manager and impact of collections from technical issues resulting from the implementation of new software.

Australian online personal loan book growth (source - Company Reports)

Australian online personal loan book growth (source - Company Reports)

In United Kingdom the credit card legislation came into effect from 2

nd January 2015. Cash advance volumes have fallen by 12.1% on the previous corresponding period. Personal loan volumes have been more severely impacted by the change and are down 54.9% on the previous corresponding period. This is largely due to the fact that loans that were written prior to 2

nd January 2015, cannot be refinanced under the new legislation. Corporate stores in UK have suffered from the reduced margin on their cash advanced fees from the rate cap introduced on 2

nd January 2015. Also commission on personal loans written have decreased due to the same reason. UK Corporate stores produced a loss of $962,206 down 63.3% on the previous corresponding period. A cost cutting program has been implemented all across the UK business to reduce overheads particularly overheads related to personal loan business. A restructure is also underway to more effectively manage the UK business. Some senior management changes have already been made. An EBITDA loss of approximately $3.1 million is expected to be incurred in the second half across UK businesses.

CCV Daily Chart (Source - Thomson Reuters)

CCV Daily Chart (Source - Thomson Reuters)

Demand for company’s financial services product range continues to be strong in Australia there is a healthy growth of online cash advance product. The company has a finance facility with FleetPartners for funding car purchases for the Green Light Auto Group, a bond facility with FIIG Securities, a bank securitisation facility for its Australian loan book and a bank working capital facility in Australia. The company’s cash flow and cash position are strong and the company is well funded to pursue growth. The UK business remains under pressure following the implementation of the new regulatory regime. The company is reviewing the UK operations to ensure that the current cost structure better matches the size of the business today. The impact of these savings will benefit the business going forward

The company is currently trading at a stock price of $0.715, which is away from the 52 week high of 1.205 and close to the 52-week low of 0.665. At the current price the company is trading at a Price to Earnings multiple of 12.790 and a dividend yield of 5.5%. There are other companies in the sector are trading at a similar combination of P/E ratio and dividend yield.

Despite some bad news related to legislation and the challenges in UK, the growth prospects of the company are sound. Furthermore given the low Price to Earnings ratio of he company, we believe that the stock is a buy at the current price of $0.715.

Nine Entertainment

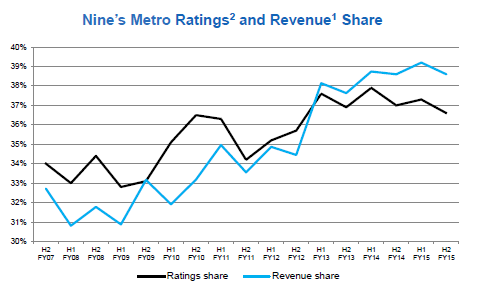

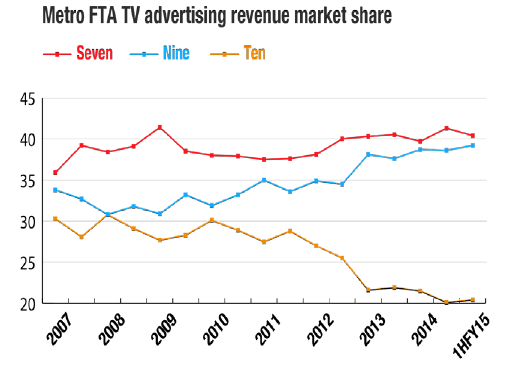

The pay TV penetration has been slowing down, and even ARPU (over $90 per month) has been decreasing. Meanwhile, the demand for news on free to air (FTA) TV during the peak news services hours continue to attract greater than 1 million viewers each night throughout the year. As per the advertising industry, the expenditure has been growing at a CAGR of 2.2% over the last ten years. TV continue to account the major total ad spend of over 30%, while TV and online segments represent over 65% of the advertising expenditure. The company operates in these major segments of advertising industry that is in television as well as online.

Australia Pay TV Penetration (Source: Company Reports)

NEC Penetration in Online Media

Online media has been witnessing strong demand in advertising against other media formats like traditional newspapers. As a result, the firm wants to tap this opportunity to minimize its risks, and have acquired Mi9 in 2013. Microsoft continues to be the form’s strategic partner. NEC has developed a strong audience network reaching over 12.3 million online domestic publishers. The firm is also seek a leading share in online display market and tap the growing online video advertising opportunity. Also, NEC has invested in Daily mail Australia in 2014 and Pedestrian TV, Australia’s leading youth culture publisher in 2015.

Australian Advertising Expenditure (Source: Company Reports)

Advertising revenues have been decreasing for free to air as well as newspaper formats, while the online advertising revenues have been growing rapidly. In fact price water coopers estimates that the internet would contribute over 51% of advertising dollars by 2019, an increase of 34% from 2014. Moreover online streaming services like Netflix are expected to divert TV audiences. As a result, Nine Entertainment entered into a 50:50 joint venture with Fairfax Media in September 2014, launching an Australian Subscription video on demand service call Stan. Both the shareholders have committed till $50 million each over a multiyear period to break even. Stan got 100,000 gross sign ups by Mid-March and intends to achieve a range of 300,000 to 400,000 active subscribers by December 2015. The present streaming run rate is over 1.5 million hours per month.

.png)

Stan’s Performance (Source: Company Reports)

As per the other developments, the firm has also sold Nine live to Equity partners for $640 million. The net proceeds to the firm will be 64 cents per share. The warner bros contract will be finished by 2016. The NRL prepayment is expected by 2017. NEC announced a $150 million buyback program in February 2015, and remains on track

Conclusion

Nine Entertainment Co Holdings Ltd (ASX: NEC) has plunged over 27.7% in just last four weeks post its trading update. The company now expects its EBITDA (before specific items, and inclusive of Nine Live) to be in the range of $285 million to $290 million, as compared to $311 million during the same period last year. The group decrease its outlook, on the back of slower than expected growth in free to air advertising market during the second half of the year. Free to Air advertising market is expected to witness a single digit decline especially in May and June of 2015. Earlier, the Free to air market was expected to grow at over 2% during the period. As per the firm’s dividend policy, the group expects to maintain its final dividend to over 5 cents per share and intends to declare it post the full year results in August 2015. Nine Entertainment estimates to improve its annual dividend payout ratio to 80% to 100% of net profit after tax (pre specific items).

NEC Daily Chart (source - Thomson Reuters)

NEC Daily Chart (source - Thomson Reuters)

On the other hand, Nine Entertainment is making all the efforts to maintain its dominant position in the growing competing Australian free to air market. Meanwhile, rumors have been swirling on Nine Entertainment’s possible gain of broadcasting rights for major sports events like AFL and the NRL, to maintain its dominant position. We believe the recent correction to be a buying opportunity to the shares of NEC. The firm’s streaming service-STAN and buyback program is expected to drive the stock going forward.

Based on the foregoing, we give a “BUY” recommendation to the stock at the current price target of $1.505.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...