Woodside Petroleum

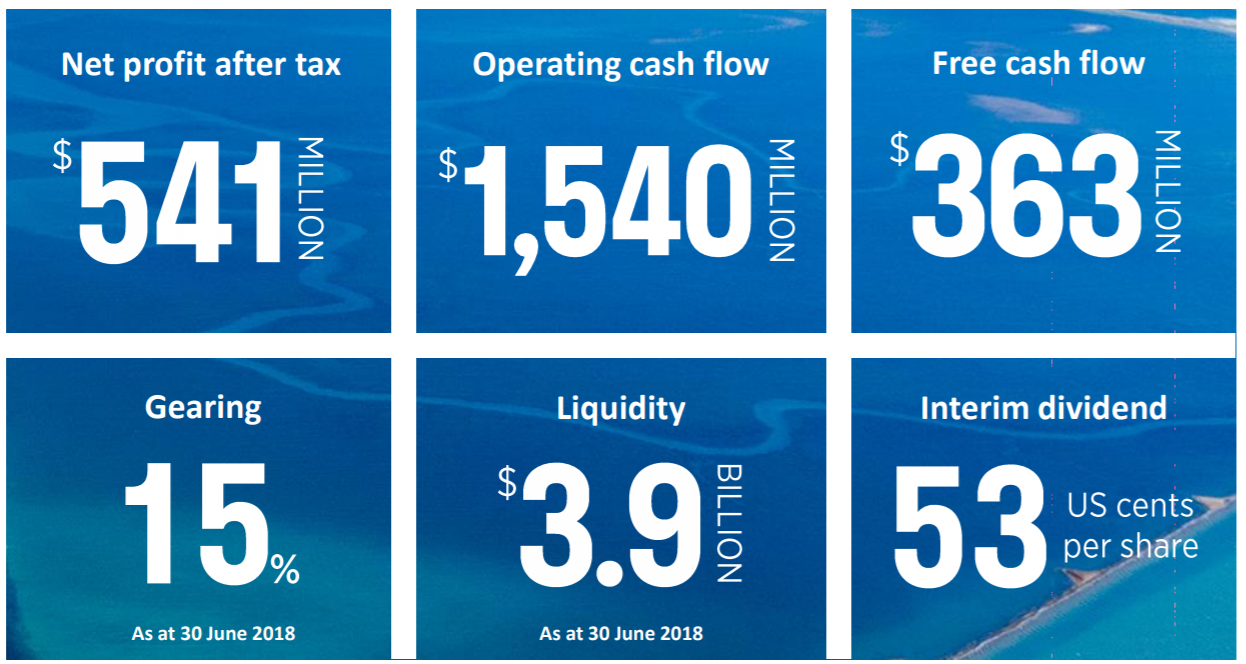

Decent Performance in 1H FY18:Woodside Petroleum Limited (ASX: WPL) posted a decent 1H FY18 set of financials in which Revenue and NPAT grew by 27% and 6% to $2,388 Mn and $541 Mn in 1HFY18 over the prior corresponding period. Based on higher production and sales growth, the group delivered positive free cash flow while acquiring additional equity in the Scarborough gas resource and investing to deliver the near-term growth which will contribute to the targeted production of approximately 100 MMboe in 2020. In other words, this has resulted in an uplift of 25% in operating cash flow to $1,540 million in 1H FY18 over the prior corresponding period. As of 30 June 2018, the company has net debt of $2,973 Mn with a gearing ratio of 15%. Moreover, the company expects investment expenditure for 2018 to be between $2,000 Mn and $2,050 Mn, which includes the acquisition of an increased interest in Scarborough in the first half. As on now, the group balance sheet is in good shape for the upcoming growth phase. Moreover, the group is making progress on its two key LNG growth project i.e., Scarborough/Pluto Train 2 and Browse strategic agreement with NWS Project participants and also preparing the phase 1 Senegal oil advancement for FID in 2019.

Besides this, the company has maintained a low unit production cost of $3.60 per barrel of oil equivalent at Pluto LNG and the North West Shelf project. And, the group now have Wheatstone on stream with both Trains 1 and 2 exceeding nameplate capacity. Based on the performance of Pluto, Wheatstone and its oil assets, the company has uplifted its 2018 production guidance from 85 to 90 million barrels of oil equivalent, up to 87 to 91 million barrels of oil equivalent.

Financial Performance (Source: Company Reports)

The group informed the market that one of its Non-Executive Director, Lawrence (Larry) Eben Archibaldwho had an Indirect interest in the company acquired 598 shares through the on-market purchase with the share price consideration of $37.05 per share. Meanwhile, the share price has risen 24.81 percent in the past six months (as at September 11, 2018) and traded at a reasonable PE level of 22.80x. Based on decent performance in 1H FY18, we maintain our “Hold” recommendation on the stock at the current market price of $ 36.700 (up 1.6% on September 12, 2018).

Horizon Oil

Improved Outlook Ahead: Horizon Oil Limited’s (ASX: HZN) stock climbed up 8.696 percent on September 12, 2018 as the group presented its business prospects to RIU ? Good Oil conference at Hyatt Regency Hotel, Perth and highlighted about FY18 activity and guidance for FY19 wherein the group continues to focus on the portfolio of conventional production, development, and exploration assets in Asia-Pacific region, including 26.95% interest in Beibu Gulf oil fields, 26% interest in Maari/Manaia oil fields, and 30% interest in Western LNG resources base. In the release, the group stated that it anticipates Earnings before Interest, Taxes, Depreciation (or Depletion), Amortization and Exploration Expense (EBITDAX) in the range of US$65 Mn to US$75 Mn for FY19. This will be mainly supported by topline growth, high-margin, low-cost oil production, and reserves. Additionally, the group anticipates net operating cash flow from China and New Zealand, for FY19, to be around US$70 Mn to US$ 80 Mn, with modest capital expenditure.

On the other hand, the group posted decent FY18 financials in which sales revenue increased by 46% and amounted to US$100 Mn in FY18 over the prior year. It was mainly driven by the volume and value growth during the period. As a result, EBITDAX grew by 52% and amounted to US$68.5 Mn in FY18 compared to the previous year. However, the company recorded loss after tax of US$2,599 Mn in FY18 from the loss after tax of US$336 Mn in FY17. It was mainly impacted by the higher finance cost related to the unrealized movement in the value of options. Despite the additional acquisition interest of 16% in the Maari/Manaia fields in New Zealand, the company reduced net debt by $20 Mn over the year to $88.6 Mn.

.png)

FY18 Financial Highlights (Source: Company Reports)

Pinnacle Investment Management Group Limited and its subsidiaries ceased to be the substantial holder of the Group since 12 September 2018. Meanwhile, the share price has fallen 17.86 percent in the past three months as at September 11, 2018 and traded close to the 52-week higher level. Based on foregoing, we maintain our “Hold” recommendation on the stock at the current market price of $0.125.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...