Free Cash Flow to Equity (FCFE)

Updated on 2023-08-29T11:58:17.085340Z

What is free cash flow to equity?

Free cash flow measures are used to understand the amount available to a company to return to its investors, including shareholders and bondholders. It is used as a proxy for a company's valuation instead of dividends or share buybacks as these are often not linked to a company's earnings and hence, do not reflect the true potential. There are two widely used free cash flow measures: free cash flow to the firm (FCFF) and free cash flow to equity (FCFE). Free cash flow to equity is the amount available with a business to be paid to its shareholders after deducting all reinvestment requirements and other legal obligations, including interest and principal repayments.

Summary

- Free cash flow to equity is the amount available with a business to be paid to its shareholders after deducting all reinvestment requirements and other legal obligations, including interest and principal repayments.

- Free Cash Flow to Equity (FCFE) = Net Income - (Capital Expenditures - Depreciation) - (Change in Non-Cash Working Capital) + (New Debt Issued - Debt Repayments)

- Valuing high growth companies using a dividend discount valuation method might underappreciate the high growth prospects. Hence, typically in such companies, FCFE is used as a proxy for the dividends in the discounted cash flow methods.

Frequently Asked Questions

How is free cash flow to equity calculated?

While there are many formulae to arrive at FCFE, the following equation is widely used:

Copyright © 2021 Kalkine Media

The free cash flow equation starts with the net income available to shareholders- this is the accounting profit that the shareholders have earned in the given period and is the base amount available with a business to be distributed to its shareholders. However, certain major cash flow items like capital expenditures, debt repayments, and working capital repayments do not factor in the accounting profits and have to be adjusted from this net income.

Capital expenditures are a significant cash outflow that is not accounted for in the net profits. It primarily includes the purchase of tangible and intangible assets and the acquisition of assets. Given that it is a cash outflow, gross capital expenditures are deducted from the net outflow. However, depreciation and amortisation expenses are included in the net profit calculation but do not involve cash outflows. Hence, they are added back while calculating free cash flow. The difference between gross capital expenditure and depreciation is defined as net capital expenditure. Net capital expenditure is considered an indicator of the growth aspect of a business. High net capital expenditure relative to a company's earnings typically indicates high growth potential. On the other hand, some firms have low or negative net capital expenditure and typically indicates lower growth potential.

Working capital, the capital used for day-to-day operations of a business, is another major cash flow item adjusted while calculating free cash flows. It is calculated as current assets less current liabilities. An increase in working capital indicates increased investment in current assets compared to current liabilities. In other words, higher working capital leads to increased cash investment in current assets and is hence a cash outflow. Similarly, a decrease in working capital leads to the release of cash from working capital, which is a cash inflow. The working capital requirements of a firm are usually linked to the industry it operates in. For instance, industries like retail have high working capital requirements. On the other hands, services industries like Information Technology and Business Process Outsourcing (BPO) have lower working capital requirements.

The final major component considered for calculating free cash flow is net debt repayment. Firms often fulfil their financing requirements using debt. If a company raises debt, the amount so raised can be utilised by the shareholders and must be added while computing free cash flow to equity. Similarly, repayment of debt reduces the cash available with shareholders and hence, must be deducted while calculating free cash flow to equity. In some instances, companies refinance their existing high-cost debt with a lower cost debt and hence, the net debt repayment amount must be added while computing free cash flow to equity.

In addition to these, certain companies might use hybrid instruments or preference shares to finance their activities. In such cases, net cash inflow or outflow from such instruments is added or subtracted while calculating free cash flow to equity. For instance, the dividend paid to shareholders should be subtracted while the firm must add the amount raised from the issue of preference shareholders back to net income.

We arrive at the residual cash flows available with shareholders by adjusting the net income for the cash flow effects of net capital expenditures, changes to working capital and net debt repayments. Hence, this is defined as the free cash flow to equity. A company can use this cash to be paid out as dividends or even for stock buybacks.

How is free cash flow to equity calculated?

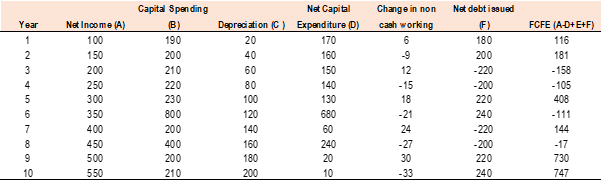

Let’s understand the calculation of free cash flows with the help of an example. The below table shows the net income, capital expenditures, working capital changes and debt repayments for company A and the FCFE calculation over 10 years.

Copyright © 2021 Kalkine Media

As the above table shows, Company A had negative free cash flows to equity in four out of the ten years. In two of the years, it was primarily due to significant debt repayments. On the other hand, FCFE was negative in the other two years primarily due to the high capital expenditures. It must also be noted that in some of the years like years 1 and 2, FCFE is positive only due to debt.

Why is free cash flow to equity used as a proxy for dividends?

Investors in companies receive payouts in the form of dividends and share buybacks. As a result, dividends are the primary metric for equity returns from a company. However, free cash flow offers a broader view of the total resources available with a company to be distributed amongst its shareholders. Dividends are often just a minor portion of the free cash flow, especially for high growth potential companies. In such companies, the cash remaining after dividends is retained by the management for investment opportunities. As a result, valuing high growth companies using a dividend discount valuation method might underappreciate the high growth prospects. Hence, typically such companies are valued using free cash flow to equity, where FCFE is used as a proxy for the dividends in the discounted cash flow methods.