ILU Dividend Details

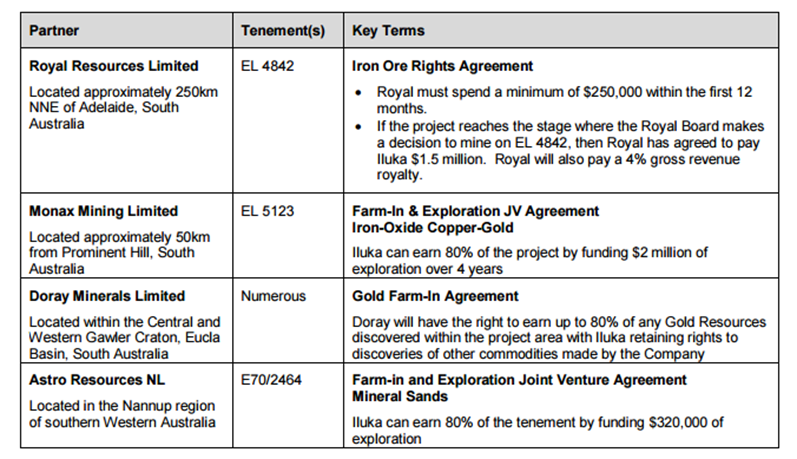

Farm-in agreements and third quarter performance: Iluka Resources Limited (ASX: ILU) recently issued a notice for its 51% entitlement to E70/2464 under the Farm-in and Exploration Joint Venture Agreement. Primarily, the company has undertaken very low expenditure under the terms of the Farm-in and Exploration Joint Venture Agreement and issued a corresponding notice to Governor Broome Sands Pty Ltd. Another update has been centered on the Gold farm-in agreement between Doray Minerals Ltd and Iluka with regards to Gold Rights at the West Gawler Project. As per the third quarter highlights, ILU’s production with regards to Zircon/rutile/synthetic rutile (Z/R/SR) improved by 41% to 198 thousand tonnes in September quarter, as compared to 141 thousand tonnes in June 2015 quarter. The group reported a year to date production increase of 21% to 475 thousand tonnes against 393 thousand tonnes in prior corresponding period, driven by high-grade titanium feedstock production and resumption of production from Iluka’s SR 2 kiln. Accordingly, the revenues for products of Z/R/SR rose 26% year on year to $168.9 million in September 2015 quarter driven by better sales volumes, falling Australian dollar and increased proportion of synthetic rutile in the product mix.

Farm in and Joint Exploration Activities (Source: Company Reports)

Drilling Updates: ILU is set to commence drilling for the Phar Lap Project (JV with Monax Mining Ltd) which will entail three diamond drill holes to a depth of ~500 metres for testing three separate gravity anomalies.

Stock Performance: The shares of Iluka have been correcting over 31% (as of November 12, 2015) from the last six months and fell over 17.46% in the last four weeks due to ongoing tough market conditions. Then there were deferred shipments of over 15 thousand tonnes of zircon volumes in fourth quarter while the group tried to optimize logistics costs by combining cargoes. However, Iluka Resources reiterated its production and sales guidance for the full year of 2015 and estimates a higher production as compared to last year, in spite of tough market conditions. ILU is controlling capital expenditure as well as enhancing its cash costs of production to offset the falling prices pressure. Higher volumes coupled with ongoing Australian dollar pressure against the US dollar would continue to be favorable for Iluka. Further, the titanium market seems to show signs of recovery with improved demand in North America and China. Based on the foregoing, we reiterate our “BUY” recommendation in this 3.11% dividend yield stock, at the current price of $5.99.

ILU Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.