Corporate Travel Management Ltd

.png)

CTD Details

Targeting future growth via acquisition: Corporate Travel Management Ltd (ASX : CTD) reported impressive 43% rise in revenues for the half year of 2016 while EBITDA increased by 38% and net profit surged 75% to $17.3 million. Management guided FY16 EBITDA to be at the top end range of $68 million vs $ 28 million in H1FY16 indicating robust performance for the second half of the year. On the other side, CTD is making continuous efforts to maintain its growth track and accordingly acquired USA based Travizon Travel for US$21 million to deepen its US footprint after the acquisition of MontroseTravel earlier in the year. The Group had also joined forces with Australia's most popular shopping rewards program, flybuys, with the launch of a new online travel booking website, flybuys travel, which would help company to increase its sales with a bouquet of services offering to its customers.

Consequently, the stock rallied over 26.35% in the last six months (as of May 03, 2016). Given strong earnings growth forecast, we give “Hold” on the stock at the current market price of $14.36

.PNG)

CTD Daily Chart (Source: Thomson Reuters)

Flight Centre Travel Group Ltd

.png)

FLT Details

Strong corporate brands: Flight Centre Travel Group Ltd (ASX: FLT) has six dedicated brands providing specialist services which generated 35% of the total turnover for the first half of FY16. This year, the group acquired four companies – BYOject.com, AVMIN, FCM Mexico and Malaysia and Cievents Hongkong - which would strengthen its FCM and Cievents brands. The Group recently rolled out next generation shop and also launched new products like GOGO Care in USA and Mexico and IAPs in Canada while another product - Key to The World- is in process. In order to enhance operational flexibility new front-end wage model has been initiated in United Kingdom and New Zealand after implementing successfully in Australia in FY15. For the first half, the Group reported 15.1% rise in revenues to $1.3 billion while net profit grew 16.3% to $ 116.7 million. The Group also declared interim dividend of 60 cents per share.

.png)

1H16 TTV by Region (Source: Company Reports)

Going forward, the management expects full year PBT of $380 million to $395 million. The client acquisition and business expansion through acquisition, product and store launches and strong brand earning visibility confirms company is on growth track, which would be supported by share price appreciation. For instance, FLT has tied-up with Cover-More (ASX: CVO) wherein CVO will provide travel insurance across nine FLT brands. We recommend a “Hold” on the stock at the current market price of $37.81

.PNG)

FLT Daily Chart (Source: Thomson Reuters)

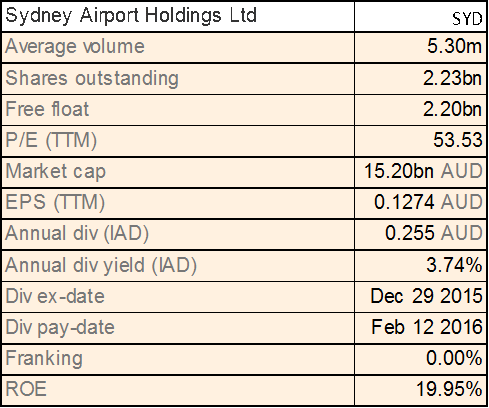

Sydney Airport Holdings Ltd

SYD Details

Boosting capital position: Sydney Airport Holdings Ltd (ASX: SYD) recently finished the issue of USD900 million of US144A/RegS 10 year bond while the group intends to use the AUD1.2bn equivalent of proceeds to repay its drawn bank debt, unlocking additional liquidity to cover future debt maturities and fund investment. The group’s traffic performance also improved and reported a total passenger’s rise by 7.6% during this year to date (as of March 2016). During March, the group’s international and domestic passengers rose by 7.9% and 4.4% respectively.

.png)

Outstanding performance (Source: Company Reports)

Meanwhile, SYD announced seven new international carriers in fiscal year of 2015 while reported a 3.8% price hike forecasts for over next four years, enhancing international travel revenues. In car parking segment, 1600 new car spaces were planned, while in hotel segment, two new hotels with 250 hotel rooms will be constructed. Accordingly, SYD surged over 31.09% in the last one year (as of May 03, 2016) placing them at very high P/E. We believe SYD is “Expensive” at the current market price of $6.99

SYD Daily Chart (Source: Thomson Reuters)

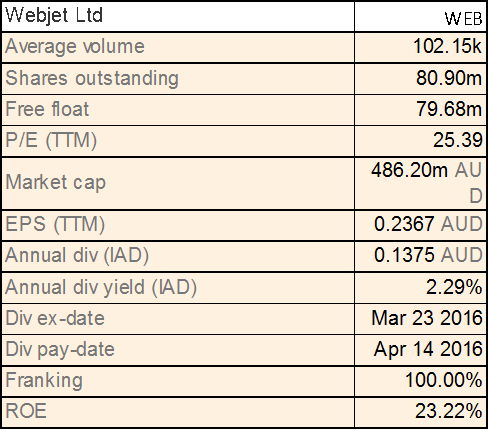

Webjet Ltd

WEB Details

Robust TTV growth: Webjet Ltd (ASX: WEB) reported 28% increase in TTV (total transaction value) to $796 million for the first half of FY16. B2B segment (hotel and Sun hotels brands) reported splendid 53% rise while B2C segment (comprising the Webjet and ZUJI brands) reported 22% increase in TTV. Revenues grew to $ 73.8 million while net profit was at $10.7 million against $9.1 million in previous corresponding period. The Group declared interim dividend of $0.065 per share.

For FY16, the Group has capex plan of $8.5 million towards development of website and point of sales and improvement on international shopping and selection processes and mobile applications. Going forward, the management expects B2B-TTV to exceed $700 million by FY18. The stock has delivered 65.95% return over the last one year (as of May 03, 2016) due to which it is trading at high P/E. We believe the stock is “Expensive” at the current price of $6.18

WEB Daily Chart (Source: Thomson Reuters)

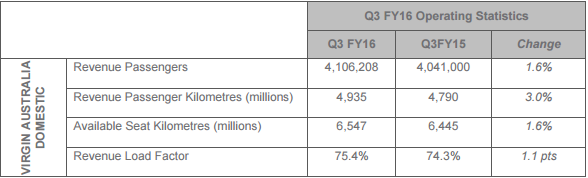

Virgin Australia Holdings Ltd

.png)

VAH Details

Business transformation initiatives:Virgin Australia Holdings (ASX: VAH) reported revenues of $2,658.2 million in first half of FY16 as against $2,377.5 million in H1FY15. The underlying PBT was at $81.5 million, up from $10.2 million recording a significant increase. Going forward, the management expects to close FY16 with profit. Moreover, the group also plans to increase capacity by over 35,000 more seats on trans-Tasman route, A330 with “The Business” from MEL and BNE to Fiji. Meanwhile, over last five years, the Group has undertaken a major transformation program resulting into an evolution from a low cost carrier to a diversified airline group. Cost cutting is a major objective and the group is targeting to control $1.2 billion by end of FY17.

Operating Statistics for quarter ending March 2016 (Source: Company Reports)

Moreover, the group is also restructuring its capital to support its strategic objectives and as part of this, recently the Group has secured a new 12 month A$425 million loan facility with its four major shareholders Air New Zealand, Etihad Airways, Singapore Airlines and Virgin Group. This new loan would provide an additional flexibility in the short term.

Furthermore, Air New Zealand (holding over 26% in VAH) is exploring options with respect to its shareholding in Virgin Australia Holdings Limited including a possible sale of all, or part of its shareholding to focus on its own growth opportunities. In the third quarter update as on March 31, 2016, VAH reported a statutory loss after tax of $58.8 million. On the other hand, given the slowdown in the economy, we still believe the stock is “Expensive” at the current market price of $0.305

VAH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.