Commonwealth Bank of Australia

.png)

CBA Details

Pressure on margins:Commonwealth Bank of Australia (ASX: CBA) plunged 3.36% in the last one month (as at April 20, 2016). CBA posted a 4% gain in first-half cash profit in line with market expectation. The bank reported drop in revenues and increase in loan impairment expenses. Loan impairment expenses were largely driven by higher home loan arrears and losses in mining towns of Western Australia and Queensland and higher rural lending provisioning in New Zealand.

The Bank declared a flat dividend of $1.98 a share. Furthermore, there is pressure emanating from rising bad debt charges, stretched margins as well as stricter capital rules. CBA’s third-quarter cash profit is expected to be steady on-quarter with a flat margin. We give “Expensive” recommendation on CBA at the current market price of $75.48

CBA Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Details

Improvements in operations:National Australia Bank Ltd.’s (ASX: NAB) first half results are due in May 2016 while the bank reported a decent cash earnings for continuing operations excluding CYBG PLC to $1.7 billion for December 2015 quarter. Statutory net profit was at $1.5 billion while revenues were higher by 2%.

.png)

Basel Methodologies (Source: Company Reports)

Moreover, Bad and doubtful debts fell 52% to $84 million, mainly due to lower charges in Australian banking due to improved asset quality. NAB’s step to sell 80% of its life insurance business is indicative of its last major divestment of low returning and legacy assets.

Accordingly, NAB would continue to focus more on its core operations. NAB dipped 3.65% in the last one month (as at April 20, 2016) but with the stock trading at attractive P/E and a solid dividend yield coupled with other transformation changes, we recommend a “Buy” at the current market price of $27.52

.PNG)

NAB Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Details

Credit Environment witnessing some softness: Australia and New Zealand Banking Group Ltd (ASX: ANZ) reported revenue growth of 3.63% from $35.8 billion to $37.1 billion in FY15 and there was an improvement of 3.05% in net income from $7.27 billion to $7.49 billion. Furthermore, according to data release from Australian Prudential Regulation Authority, Australia & New Zealand Banking Group Ltd is gaining a market share. The group also reported that they estimate another $100 million increase to the earlier estimated $800 million of credit charge for the first half of 2016 while indicating exposure to resources as the key factor for some extent of weakness.

ANZ stock recovered over 0.55% in the last five days (as of April 20, 2016) and is up 1.67% on April 21, 2016, and trading at an attractive P/E and dividend yield. We recommend a “Buy” at the current market price of $24.30

.PNG)

ANZ Daily Chart (Source: Thomson Reuters)

Westpac Banking Corporation

.png)

WBC Details

Challenging environment: Recently, Australia’s securities regulator, ASIC has started civil proceedings against Westpac Banking Corporation (ASX: WBC) in relation to the Bank Bill Swap rate and WBC has indicated to defend the claim while rejecting the allegations.

We also note that Westpac has flagged higher debt provisions because of bad consumer loans in Western Australia and Queensland, which have been hit by the resources industry downturn. More will be revealed when the bank reports its first-half results on May 02, 2016. Given such tough environment to the group, we believe the stock is “Expensive” at the current market price of $31.15

WBC Daily Chart (Source: Thomson Reuters)

Telstra Corporation Limited

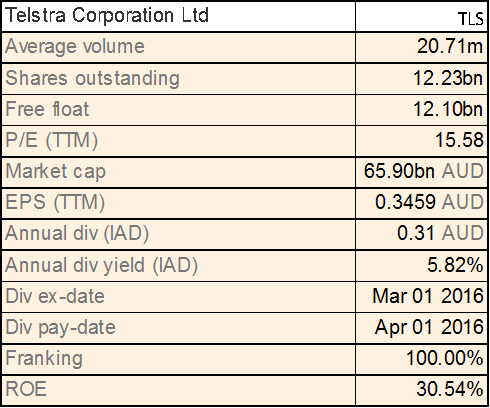

TLS Details

Divestment of stake in Chinese company: Telstra Corporation Limited (ASX: TLS) had entered into an agreement with Ping An Insurance Group for the sale of 47.7 % of total issued shares in Chinese online business Autohome for $2.1 billion and retain a 6.5% interest after completing the transaction. TLS also inked a deal (worth $1.6 billion) to upgrade the cable television and internet assets that were sold to NBN in 2014 with an aim to provide planning, design, construction and construction management services for the hybrid fibre-coaxial (HFC) network. Meanwhile, for H1FY16, the Group reported total income growth of 9.1 % to $14.2 billion, and EBITDA was up 1.7 % to $5.4 billion.

Net profit was up 0.8% to $2.1 billion. The Group secured a new five year naming and mobile digital rights agreement with the NRL, including mobile live broadcast rights out to 2022. The stock has surged 5.04% in the last five days (as at April 20, 2016). On the other hand, we believe the stock is “Expensive” at the current levels at the market price of $5.42

.PNG)

TLS Daily Chart (Source: Thomson Reuters)

BHP Billiton Limited

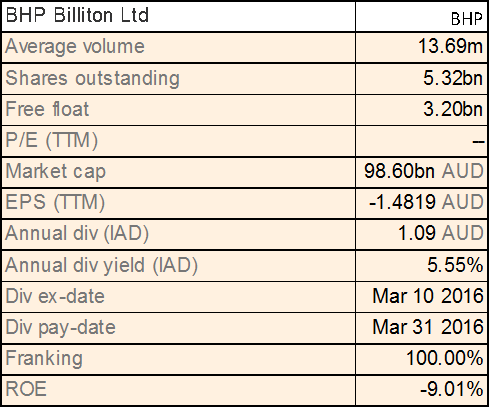

BHP Details

New operating Model: BHP Billiton Ltd (ASX: BHP) moved up 7.79% in the last five days (as at April 20, 2016) and recently established an operating model for making its business less agile in the disturbed mining market and widen the scope of its business in various geographical operating regions. This would help BHP to accrue a globally recognized operating scale and expertise.

.png)

March year to date performance (Source: Company Reports)

In order to improve operational capability in the quarters ahead, BHP is undertaking strategic cost-cutting programs as well as strengthening the balance sheet for greater financial flexibility. BHP is progressing well to deliver 14% of an average unit cost improvement across its major assets. The group is planning for a USD 640 million exploration program in petroleum for future growth opportunities. We maintain our “Buy” recommendation on BHP at the current price of $21.05

.PNG)

BHP Daily Chart (Source: Thomson Reuters)

CSL Limited

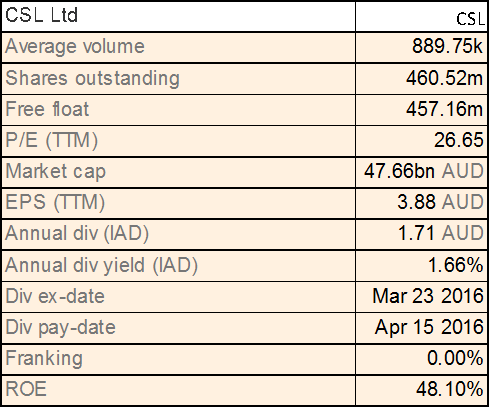

CSL Details

Global scale and unique business model: CSL Ltd (ASX: CSL) is up 4.32% in the last five days (as at April 20, 2016) and has grown in scale to become global leader through organic and acquisition route. The Board has implemented numerous on market share buybacks in recent years, boosting EPS (announced $1 billion on October 2015 while finished 53% repurchase worth of over $528 million as of March 11, 2016).

.png)

Performance for six months ended on December 2015 (Source: Company Reports)

The group declared a revenue rise by 11% yoy to USD 3,056 million for six months ended on December 2015. Hence, CSL stock surged over 16.7% in the last six months (as of April 20, 2016) placing them at higher levels. Moreover, the stock is currently trading at high P/E with a low dividend yield. We believe that the stock is “Expensive” at the current market price of $105.00

.PNG)

CSL Daily Chart(Source: Thomson Reuters)

Wesfarmers Ltd

.png)

WES Details

Third Quarter FY16 with retail sales up: Wesfarmers Ltd (ASX: WES) released its results for third quarter of the 2016 financial year that were steered through growth in Coles, Bunnings, Kmart and Officeworks. Coles’ headline food and liquor sales growth rose by 5.9% while Bunnings total sales growth jumped 11.0% at the back of ongoing investment in value, service and brand reach. Total sales for Kmart soared 17.9% to $1.1 billion, with comparable store sales increasing 15.2%.

WES sometime earlier revealed that it is implementing growth strategies which involve expanding Bunnings into UK. Additionally, Wesfarmers entered into an agreement to acquire Homebase, which is second largest home improvement and garden retailer in UK and Ireland for about $700 million. WES is also restructuring departmental store businesses to enable Kmart and Target to maximize and share opportunities. However, given the rising competition for WES, we believe the stock is “Expensive” at the current market price of $42.20

WES Daily Chart (Source: Thomson Reuters)

Woolworths Ltd

.png)

WOW Details

Restructuring efforts to deliver growth:Woolworths Ltd (ASX: WOW) reported 1.4% decline in sales to $32 billion for H1FY16 compared with H1FY15 and loss of $972.7 million after accounting $1,898.5 million towards cost of impairment of assets and store exit costs attributed to exit from Home improvement business. Excluding these significant costs, the profit recorded is $925.8 million. It has declared dividend of 44 cents. On the other hand, WOW has taken various initiatives like repositioning the Woolworths brand with the launch of “low price always” and relaunch of Woolworths reward program in supermarket segment. In petroleum segment, it widened the network by opening 5 new petrol sites taking number to 521 and has plans to add another 10 new sites in H2FY16. Its liquor group is doing well along with good progress reported from the newly acquired Summergate/Pudao business in China.

It further plans to grow network by new stores in the second half. We believe the group would benefit from this restructure strategy and will be able to deliver planned $500 million cost-savings by end of FY16. We put a “Buy” recommendation at the current market price of $21.77

.PNG)

WOW Daily Chart (Source: Thomson Reuters)

Rio Tinto Ltd

.png)

RIO Details

Cost cutting measures to improve performance: Rio Tinto Ltd (ASX: RIO) and Sinosteel Corporation have extended their historic Channar Mining Joint Venture in Australia’s Pilbara region. Accordingly, Rio Tinto will supply iron ore up to 70 million tonnes from the Pilbara, to Sinosteel Corporation over the next five years. In turn, RIO will receive one time payment of US$45 million and additional product loyalties from Sinosteel.

.png)

First quarter of 2016 performance (Source: Company Reports)

RIO also reported a decent first quarter performance with global iron ore shipments reaching 80.8 million tonnes (Rio Tinto share 64.9 million tonnes) representing an increase of 11% against prior corresponding period driven by brownfield developments and expanded infrastructure capacity in the Pilbara during 2015. The stock rose 16.33% in the last four weeks (as of April 20, 2016) and we maintain “Buy” on RIO at the current market price of $52.55

RIO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.