Brambles Ltd

.png)

BXB Details

JV, acquisitions and divestments highlights: Brambles Ltd (ASX: BXB) recently announced for the formation of a joint venture (JV), Hoover-Ferguson Group (HFG) with Hoover Container Solutions which entails combining of the oil and gas container solutions businesses of the respective companies. The JV will operate under a 50%/50% arrangement. The transaction is considered to have a neutral impact on BXB’s underlying earnings per share for FY17. BXB also finished the sale of its LeanLogistics business to Kewill for US$115 million on 1

st June 2016. This would result in pre-tax gain of US$53 Million in FY16 accounts (within Significant Items in Discontinued Operations). On the other hand, BXB acquired Empacotecnia for US$7 Million indicating the acquisition multiple of 4.9 times over the last 12 months’ EBITDA. BXB has a considerable interest in Columbia where Empacotecnia is the only RPC pooling operator. Moreover, BXB has planned an investment of US$10 Million in BXB Digital for FY 17.

.png)

Segment Performance (Source: Company Reports)

Weak guidance: BXB is expecting sales growth of 8%-10% for FY 16 while the underlying profit (based on 30

th June 2015 forex) is expected in the range of US$1,015-1,035 Million. But, the return on capital invested is expected to be down for FY 16 due to acquisitions since July 2014. Additionally, BXB has reported no growth in the overall revenue during the nine months ending on 31

st March 2016 period as compared to the corresponding period of 2015. During this period, BXB has shown 5% fall in Pallets EMEA, but a 9% fall in Pallets Asia-Pacific leading to overall 1% fall in the sales revenue of the total Pallets as compared to the corresponding period last year. Moreover, the sales revenue of the containers also fell 3% but BXB has slight growth of 3% in Pallets Americas and 6% growth in RPCs in the nine months ended in March quarter of 2016 as compared to the three quarters of FY 15.

Moreover, even though the global pallet market is expected to grow at a CAGR of 4.90% during the period 2016-2020, one challenge that could restrict the market growth is the limited availability and high cost of raw materials as per the "Global Pallet Market 2016-2020" report. BXB is the key vendor of the Pallets who could be affected in the current scenario. We believe investors need to leverage the BXB stock rise of over 24.11% in the last six months (as of August 08, 2016), to exit the stock. Trading at a low dividend yield and higher P/E, we give a “Sell” recommendation on the stock at the current price of $12.93

.PNG)

BXB Daily Chart (Source: Thomson Reuters)

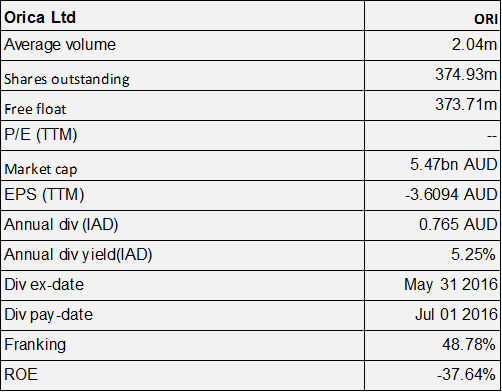

Orica Ltd

ORI Details

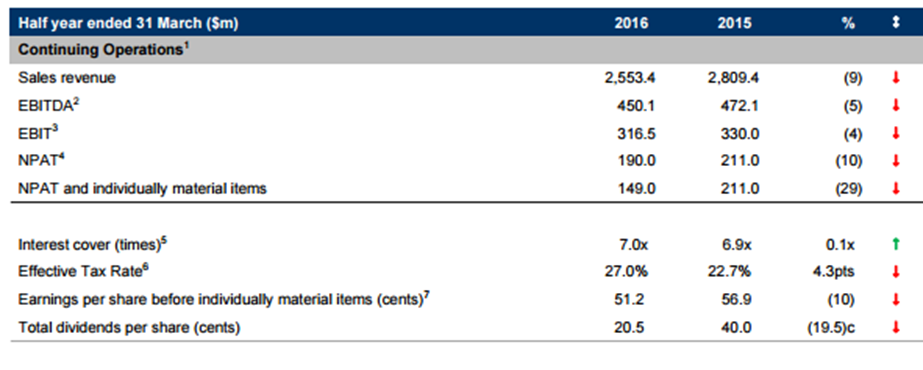

Weak performance due to challenging market: Orica Ltd (ASX: ORI) has reported a fall in AN product volume of 1.71 million tonnes in 1H16 as compared to 1.86 million tonnes on pcp basis. The fall in volume was on the back of lower demand of coal in Australia, despite improved volume in Indonesia. The underlying EBIT was down to $317 million during the period as compared to $330 million pcp. Consequently, ORI reported fall in NPAT of $190 million in 1H16 as compared to $211 million on a pcp basis while statutory net profit after tax (NPAT) fell to $149 million (as compared to pcp value of $222 million). Moreover, there was a substantial commodity price volatility since October 2015 which had affected the customer production volume as the iron ore price declined to a low point of 25% and the oil declined to a low point of 33%. Additionally, ORI’s explosives volumes were down by 20% and reached below 4-year monthly average in January/February, even though they recovered in March/April but were over 3% below the expectations. However, ORI had increased the forecast of net incremental business improvement benefits of over $70 to $80 million for FY16. The company is expecting Burrup AN plant to be commissioned in the second half of 2016. In addition, ORI replaced the progressive dividend policy with payout ratio policy having the range of 40% - 70%.

Financial Performance of 1H 16 (Source: Company Reports)

Headwinds to outlook: ORI is expecting a long term decline for the US Coal demand. There is an at least 15% reduction expected in main power generation markets (Southeast, Mid Atlantic and Central) due to warmer winter and high inventory levels which would continue to impact volumes. The declining cost of gas and increasing focus on environmental policy is leading to long term decline in demand. Moreover, higher cost in the Appalachian region has led to biggest reductions in coal production.

Accordingly, for FY 16, ORI is expecting Global AN product volumes in the range of 3.45 ± 0.1 million tonnes and over $85 million negative impact from price resets and contract renewals. We recommend investors to leverage the ORI stock rise of 20.98% in the last four weeks (as of August 08, 2016) as an exit opportunity. Based on the foregoing, we give a “Sell” recommendation on the stock at the current price of $14.70

ORI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.