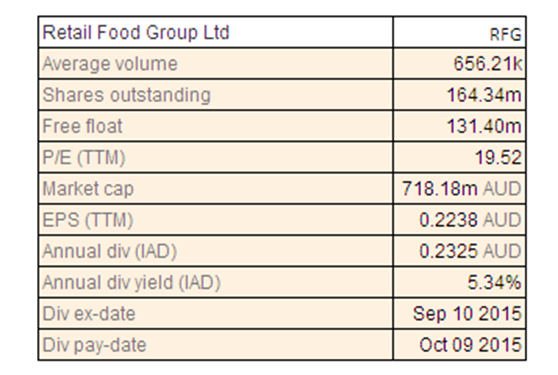

Retail Food Group Ltd

RFG Dividend Details

Expanding penetration via acquisitions: Retail Food Group Ltd (ASX: RFG) expects a positive performance with 25% growth of underlying NPAT during first half of 2016 and reiterated its FY16 guidance of 20% underlying NPAT growth against FY15. Retail Food Group expanded its penetration via its Cafe2U, Gloria Jean’s Coffees Group and Di Bella Coffee acquisitions in FY15. The group’s new outlets already rose by 140 during FY16 year to date, which is over 70% of its overall organic outlet in FY15 and the company is on track to reach its FY16 forecasts of 250 outlets.

.png)

Acquired business highlights (Source: Company Reports)

On the other hand, RFG shares plunged over 22.46% in the last six months (as of December 16, 2015) due to weak consumer sentiment but recovered by 5.74% in the last three months driven by the positive outlook. We reiterate our “BUY” recommendation on this high dividend yield stock at the current price of $4.48

RFG Daily Chart (Source: Thomson Reuters)

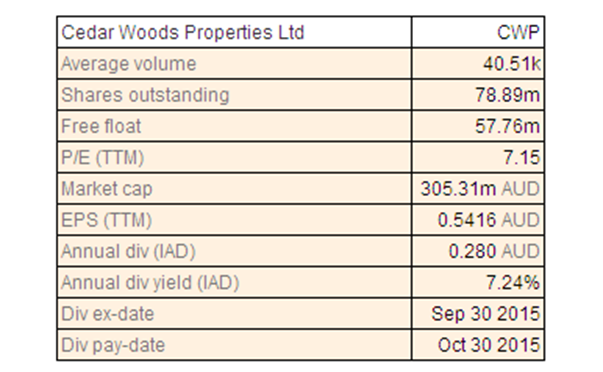

Cedar Woods Properties Ltd

CWP Dividend Details

Attractive valuations: Cedar Woods Properties Ltd (ASX: CWP) has built a strong pre-sales of $184 million during the first quarter of 2016 and got the approval from Queensland Government for developing 480 lots. On the other hand, CWP stock declined around 33.85% (as of December 16, 2015) during this year to date on the back of weak investor’s sentiment towards Western Australia exposed firms.

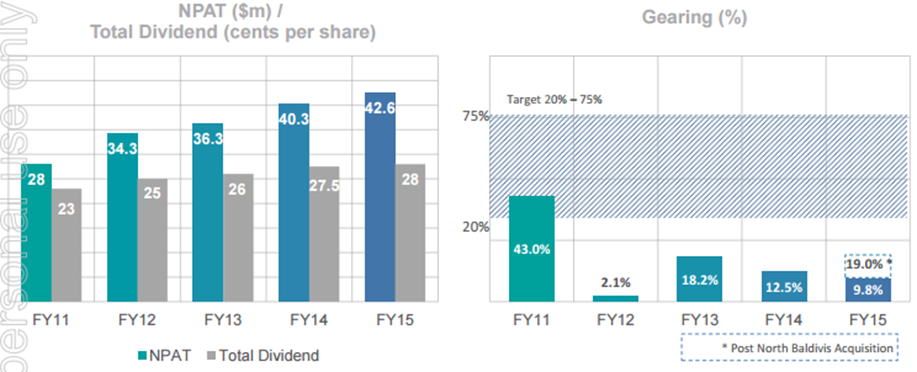

Fiscal year of 2015 performance highlights (Source: Company Reports)

But, the heavy correction in the stock placed it at cheaper valuations, with the stock trading at a lower P/E and the group has a strong dividend yield. With the improving residential property market in Western Australia, Victoria and Queensland coupled with decent earnings visibility via its pre-sales, we believe CWP would be able to deliver a better performance in the coming periods and accordingly, we give a “BUY” recommendation on the stock at the current price of $3.80

CWP Daily Chart (Source: Thomson Reuters)

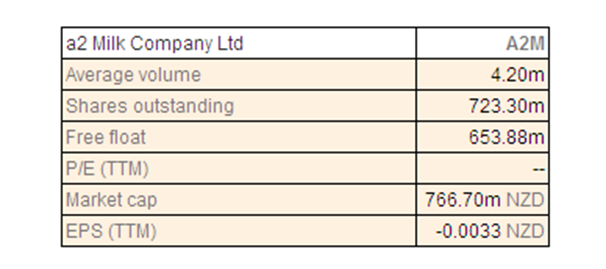

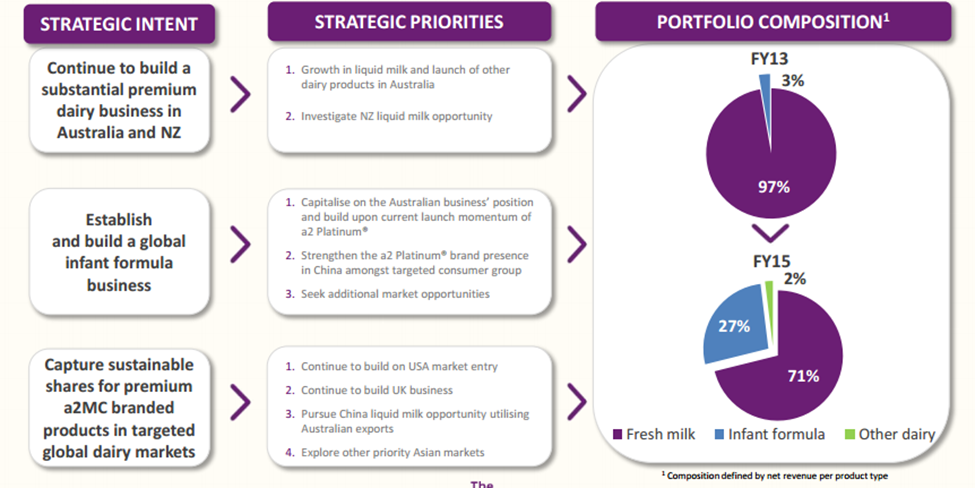

A2 Milk Company Ltd

A2M Details

Outstanding infant formula performance: A2 MILK Company Ltd (ASX: A2M) is making efforts to enhance consumer awareness on benefits of A2 beta casein protein to boost demand for its products. The group’s Platinum infant formula brand revenues continue to increase by over NZ 38 million during first four months of FY16 (as of October 2015), against the entire FY15 revenues of NZ$41.7 million.

Strategic initiatives to drive further growth (Source: Company Reports)

The firm is also focusing on China e-commerce opportunity to strengthen its platinum infant formula sales while targeting a value market share of over 15.3% for platinum infant in Australia. The shares of A2M surged over 97.12% (as of December 16, 2015) in the six months and we reiterate our “BUY” recommendation at the current price of $1.035

A2M Daily Chart (Source: Thomson Reuters)

Xero Ltd

.png)

XRO Details

Strong international subscriber’s growth: XERO Ltd (ASX: XRO) delivered a 71% year on year (yoy) operating revenue growth during first half of 2016 while the average revenue per subscriber rose to $30.70 during the period. The group generated a strong international division performance with an operating revenue growth of 110% on a yoy basis during the period. The average revenue per subscriber rose to $34.50 for international division while subscribers rose by 74,000 at CAC (related to cost of acquiring subscribers) of 21 months. Meanwhile, lifetime value of international division surged by 45% to $1,396 during the period, leading to an overall lifetime value increase by 16% to $1,805.

.png)

Xero’s position against its peers (Source: Company Reports)

Xero reaffirmed its subscription revenue forecast to be more than NZ$200 million for 2016 fiscal year (as per June 2015 FX rates) and estimates a 71% growth of annualized committed monthly revenue of $159.3 million in 2016 fiscal year. As a result, XRO stock surged over 31.96% (as of December 16, 2015) in the last three months and we believe the positive momentum would continue even in the next year and accordingly place a “BUY” recommendation at the current price of $16.76

XRO Daily Chart (Source: Thomson Reuters)

Magellan Financial Group Ltd

.png)

MFG Dividend Details

Attractive returns: Magellan Financial Group Ltd’s (ASX: MFG) Magellan Global Fund generated 29.5%, after fees, during the twelve months to 30 June 2015, surpassing the MSCI World Net Total Return Index (AUD) by 4.9%. The group has been witnessing positive funds under management this year, and recently reported net inflows of $130 million as of November 2015 with net retail inflows into global equity strategies of $203 million and net institutional outflows of $89 million. As a result, MFG stock rallied over 51.02% during this year to date (as at December 16, 2015). We remain bullish on this stock and give a “BUY” recommendation at the current price of $26.17

MFG Daily Chart (Source: Thomson Reuters)

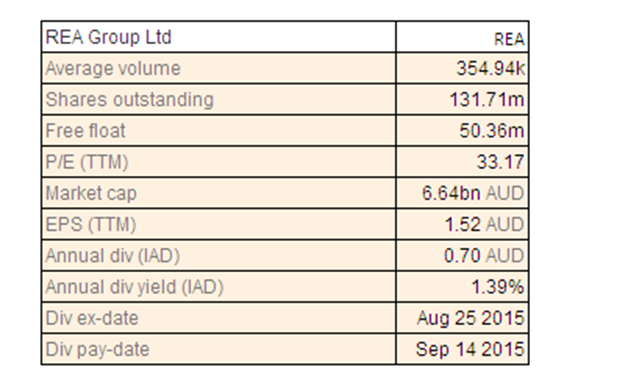

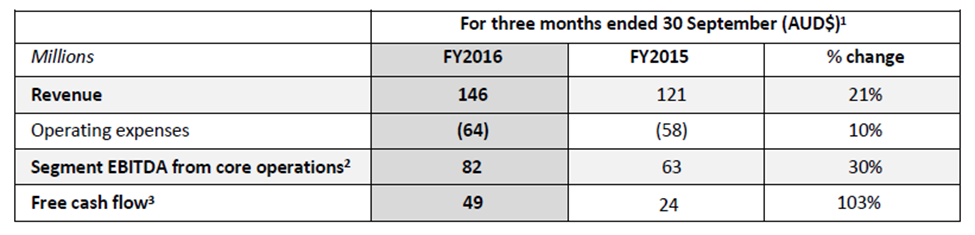

REA Group Ltd

REA Dividend Details

Expanding addressable market by focusing on Asian opportunity: REA Group Ltd (ASX: REA) intends to capture the growing online advertising market in Asia and hence acquired iProperty Group, a major property portals at Malaysia, Hong Kong, Thailand and Indonesia. The company reported a robust 21% surge to $146 million in first-quarter revenue while EBITDA jumped 30% year on year to $82 million.

First quarter of 2016 performance (Source: Company Reports)

REA is a clear market leader in Australia via its realestate.com.au wherein the average monthly time spent on this site is 5.5 times more than the number two portal site. REA stock rallied over 36.63% in the last six months (as at December 16, 2015) and we reiterate our “BUY” recommendation at the current price of $52.51

REA Daily Chart (Source: Thomson Reuters)

Crown Resorts Ltd

.png)

CWN Dividend Details

Well positioned to leverage improving tourism opportunity: Crown Resorts Ltd.’s (ASX: CWN) Australian Resorts is delivering a decent growth with main floor gaming revenue improving by 10% yoy during fiscal year of 2016 year to date ended on October 2015. The group’s VIP program play turnover growth is on track while wagering and online are generating decent performances. We believe that the group is well positioned to leverage the rising tourism opportunity especially from China’s outbound leisure travelers, estimated to increase to 200 million by 2020 from 107 million in 2014. Melco Crown’s Studio City project’s success might support group’s Macau performance in the coming periods to a certain extent. Crown resorts is trading with decent dividend yield.

.png)

Australia and Macau composition in Crown’s NPAT (Source: Company Reports)

The stock has been consolidating from the last three months and rose by 11.88% (as of December 16, 2015). In response to the latest ASX price query post the sudden surge in CWN’s share price, CWN stated that it has not received any buyout proposal from the majority owner, James Packer. The surge comes at the back of the media reports on James Packer’s Consolidated Press Holdings discussions with private equity and pension funds about a bid on CWN’s assets. Nonetheless, we estimate that the stock has the potential to deliver a decent performance going forward. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $11.58

.png)

CWN Daily Chart (Source: Thomson Reuters)

Lend Lease Group

.png)

LLC Dividend Details

Strong pipeline:Lend Lease Group (ASX: LLC) improved the construction backlog revenue by 7% to $17.3 billion, despite the current challenging conditions. LLC even enhanced its international urban regeneration projects portfolio and witnessed strong interest from Chinese buyers who contributed over 20% of the apartment pre-sales while LLC forecasts Chinese buyers’ contribution to raise to around 30% by June 2017. The group is increasing its focus on the booming retirement living and consequently developed these units to 14,193 in FY15 as compared to 12,417 in FY13.

.png)

Growing urbanization projects (Source: Company Reports)

Meanwhile, the shares of LLC surged over 11.94% (as of December 16, 2015) in the last four weeks while the stock is still trading at attractive valuations with a reasonable P/E and decent dividend yield. We believe LLC has the potential to rally further in 2016 and accordingly place a “BUY” recommendation on the stock at the current price of $13.45

LLC Daily Chart (Source: Thomson Reuters)

Fairfax Media Ltd

.png)

FXJ Dividend Details

Diversified investments to offset falling print advertising pressure: Fairfax Media Ltd (ASX: FXJ) has built a diversified media portfolio in growth business like Domain, Life Media & Events, and Stan to offset the declining print advertising market impact on its core publishing business. As a result, the group was able to sustain its growth track even during FY16 and witnessed a total revenue growth of over 2% to 3% during year to date of fiscal year of 2016, against prior corresponding period. Metro Media rose 10% boosted by its Domain’s revenue growth of 68% yoy while digital business surged 43% during the period.

.png)

Improving Domain performance (Source: Company Reports)

FXJ is also reorganizing its Australian Metro Media publishing business and estimates to deliver over $60 million of annualized cost benefits by the end of fiscal year of 2016. The company also announced about the release of 9,652,765 fully paid ordinary shares from voluntary escrow on January 01, 2016. FXJ stock increased over 2.99% in the last four weeks (as at December 16, 2015) and we believe this positive momentum would continue even in 2016 and accordingly give a “BUY” on this good dividend yield stock at the current levels of $0.865

FXJ Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Dividend Details

Strong dividend yield: Australia and New Zealand Banking Group Ltd (ASX: ANZ) shares fell over 19.30% during this year to date (as of December 16, 2015) due to investor’s concerns over its Asian division performance on the back of volatile conditions is China. On the other hand, management reported that China’s Exposure at default comprised only 3% of the bank’s exposure at default (EAD), while its total Institutional Asia Exposure constituted 12% of the group’s EAD. Moreover, the group almost doubled its total assets to $890 billion to withstand short term pressure and has built a strong Australia and New Zealand core business which would continue to perform well in the coming periods.

.png)

Performance (Source: Company Reports)

ANZ is also trading at a lower P/E and has an outstanding annual dividend yield. We remain bullish on the stock and reiterate our “BUY” recommendation on the stock at the current levels of $26.53

.png)

ANZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.