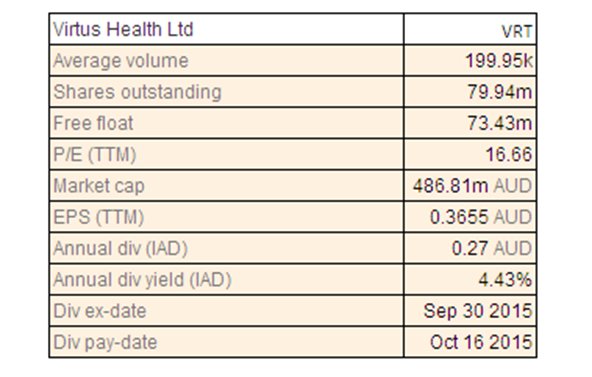

Virtus Health Ltd

VRT Dividend Details

Building business through acquisitions: Virtus Health Ltd (ASX: VRT) stock surged over 27.42% in the last three months (as at November 19, 2015), driven by its strong performance, acquisitions and favorable demographics. The group reported a revenue growth of 16.1% year on year (yoy) to $233.7 million in FY15, against $201.2 million in prior corresponding period, driven by its domestic acquisitions as well as expanding international presence. VRT acquired Sydney based Independent Diagnostic Services (with a revenue of $2.9 million for the FY15), to further strengthen its specialist diagnostics capabilities and to leverage IDS network of seven collection centers at southern suburbs of Sydney. Virtus Health is a market leader in Australia with over 37% market share and its fertility centers’ revenue improved more than estimated. VRT also maintained its leadership in Australia’s IVF services and is constantly increasing its total Virtus IVF cycles (17,064 in FY15 as compared to 15,021 in the fiscal year of 2014) with contribution from TasIVF acquisition.

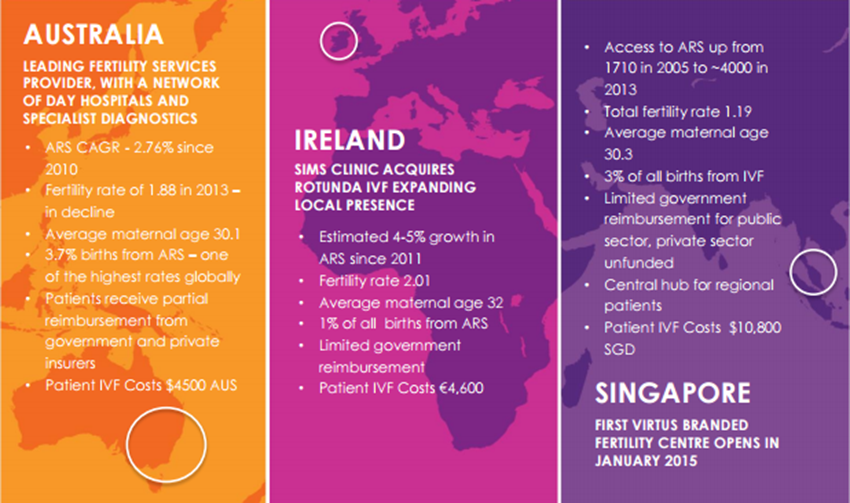

Virtus ARS markets (Source: Company reports)

Virtus is also targeting United Kingdom and South East Asia to boost its international presence. Favorable demographic drivers in Australia coupled with ongoing group’s focus on enhancing efficiency would continue to add support to the stock in the coming months. With the media reports that average maternal age in Australia has surged to 30.9 years in the last ten years and the proportion of women having babies 35 years and above surging from 17.1% (year 2000) to 22.3% (year 2015), VRT has a good scope. We reiterate our “BUY” recommendation on the stock at the current stock price of $6.22

VRT Daily Chart (Source: Thomson Reuters)

Challenger Ltd

.png)

CGF Dividend Details

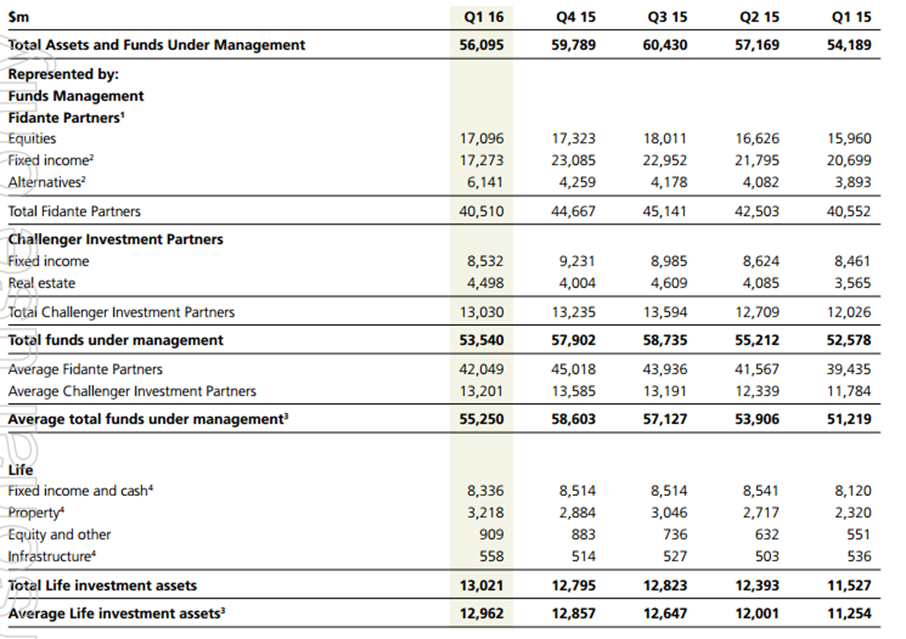

Positive regulatory reforms and expanding market opportunity to drive growth: Challenger Ltd (ASX: CGF) reported that its assets and funds under management decreased by 6% to $56.1 billion as at Sep 30, 2015, affected by the sale of Kapstream capital business and Dexion capital acquisition which would offset the solid organic flows to the group. But, the group’s total life annuity sales rose by 12% to $884 million during the first quarter of 2016 against prior corresponding period while overall retail annuity sales increased by 2% yoy to $707 million. CGF’s life’s investment assets rose by $0.2 billion to $13 billion during the period driven by net book growth. Challenger would also be benefited by the favorable demographics in Australia given the increase in ageing population, with almost 700 people turning 65 every day. Accordingly, the government (in response to the Financial System Inquiry) reported that they would enhance outcomes for retirees and the sustainability of Australia’s superannuation system, opening more opportunity to CGF. Meanwhile, CGF issued positive life’s cash operating earnings guidance in the range of $585 million to $595 million in the fiscal year of 2016.

Assets and FUM highlights (Source: Company Reports)

Challenger Ltd stock delivered a year to date of 36.78% (as of November 19, 2015) and surged over 25.87% in the last three months boosted by target market growth in Australia and favorable regulatory reforms by government. Still, Challenger is trading at a reasonable valuation and has a decent dividend yield. We recommend investors to “Buy” the stock at the current price of $8.78

CGF Daily Chart (Source: Thomson Reuters)

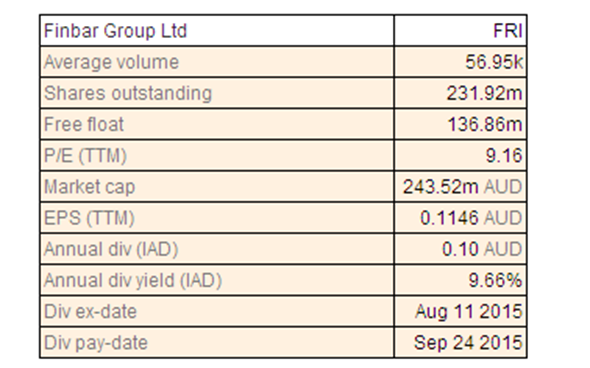

Finbar Group Ltd

FRI Dividend Details

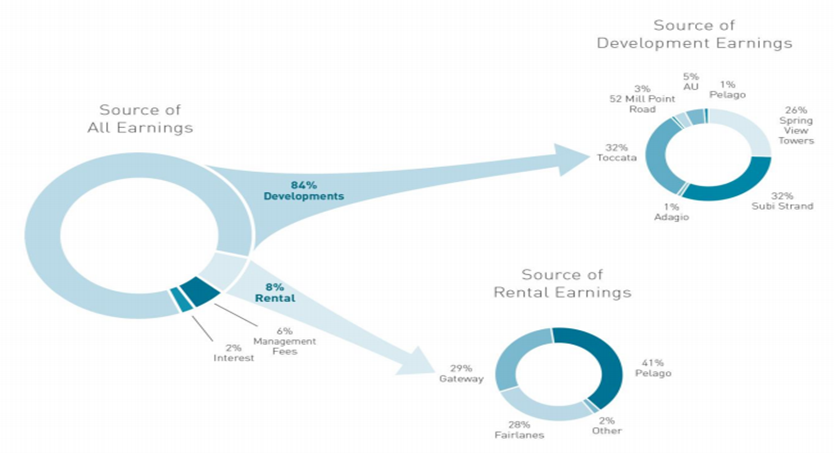

Project wins and Attractive Valuation: Finbar Group Limited (ASX: FRI) stock reported a year to date decline of 23.90% (as of November 19, 2015) and fell over 8.41% in the last four weeks, on investors’ concerns of tough market conditions impacting the group’s performance. The group’s NPAT fell over 29% yoy to $25.9 million in FY15. On the other hand, the group generated solid presales of over $407.7 million in 2015 adding to the >$2 billion project pipeline. Finbar’s average worth of sales per day reached $1.04 million during FY2015. The company finished three major projects worth of $350.3 million and already has development approval of eight projects valued at $1.06 billion. The group partnered with Perth Upper China to boost its market projects for potential Chinese buyers, while FRI has already built several other international partnerships for Singapore, Indonesia, and Malaysia markets.

Source of Earnings (Source: Company Reports)

Meanwhile, the recent correction in the FRI stock placed it at a valuation with trading at a P/E of about 9x as compared to its peers. Moreover, Finbar has an outstanding dividend yield of 9.66%. The group’s on-going buyback program is also expected to boost the stock further. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $1.03

FRI Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.