Super Retail Group Ltd

.png)

SUL Dividend Details

Delivering organic growth: Super Retail Group Ltd (ASX: SUL) delivered a sales rise of 7.1% year on year (yoy) to $2.24 billion in fiscal year of 2015, boosted by like for like sales improvement across its Auto and Sports division. The group’s auto retailing witnessed a like for like revenues increase of 2.5% during the first seven weeks of the fiscal year of 2016, while Leisure Retailing like for like revenues rose by 10% during period, driven by BCF and the clearance program in Ray’s outdoors. Over the 16 weeks to October 17, 2015, like for like (LFL) sales growth for Auto was reported as 3% (as opposed to 4% last year). In the same period, Leisure and Sports reported 5% like for like sales growth. With the new stores and refurbished stores delivering a better performance, SUL is enhancing its network across all segments. Accordingly, SCA segment is planning to open 15 new stores, and make 65 refurbishments, extensions and relocations. Leisure retailing business is opening 5 new BCF stores and finished 20 BCF refurbishments. Ray’s shift is also on track having 5 initial pilot stores (with 3 in hand and 2 new stores have been scheduled for September and October).

Financial Performance over the years (Source: Company Reports)

SUL intends to begin 8 new stores, close 3 stores and refurbish 12 stores across the Rebel and Amart Sports businesses. Super Retail Group stock was able to deliver solid performance generating an increase of over 29.16% during this year to date (as of November 16, 2015). The stock rallied over 6.04% in the last four weeks alone. SUL has a decent dividend yield of 4.22%. We maintain our positive stance on the stock, and reiterate our “BUY” recommendation on SUL at the current price of $9.60

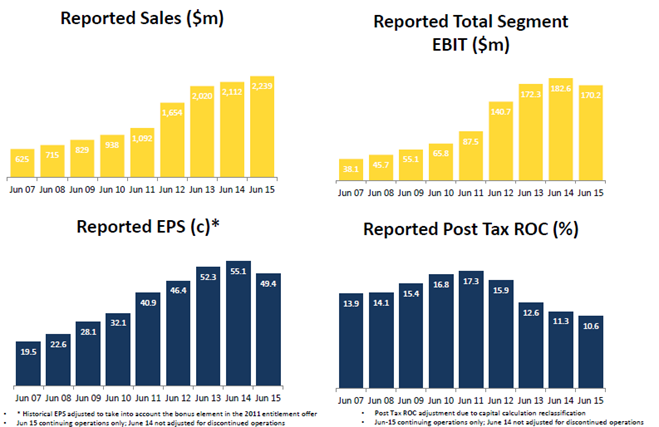

Retail Food Group Ltd

.png)

RFG Dividend Details

Strategic acquisitions to boost international coffee and franchise market penetration: Retail Food Group Limited (ASX: RFG) reported a solid FY15 performance with its underlying Net Profit after Tax rising by 49.3% yoy to $55.1 million and delivered increase of 5.7% yoy of total dividends to 23.25 cps. The group made strategic acquisitions during fiscal year of 2015 to enhance its global presence via Cafe2U which is a mobile coffee van franchise; Gloria Jean’s Coffees Group and Di Bella Coffee. Accordingly, RFG’s international brand systems EBITDA delivered outstanding performance during the fiscal year of 2015 which rose by 619% yoy (including coffee & allied beverage sales to brand systems franchisee) to $15.1 million. Subsequently, RFG expanded its presence to over 2,500 franchised outlets across the globe. The group also boosted its domestic brand systems EBITDA performance by over 16.6% yoy to $66 million in FY15, while its Coffee wholesale EBITDA surged to $7.7 million from $0.4 million in FY14.

.png) Expanded Network highlights

Expanded Network highlights (Source: Company Reports)

Stock Outlook: Retail Food Group acquisition business contributed over $19.8 million to the RFG’s FY15 underlying EBITDA, while the group estimates a better FY16 for acquisition assets which might contribute over $35 million in underlying EBITDA. RFG is already leveraging its expanded network and accordingly launched its Brand Systems in several international markets and even started international distribution hubs and coffee roasting facilities. On the other hand, the stock corrected over 35.56% in the last six months (as of November 16, 2015) owing to softness in consumer sentiment. But we believe that this correction led the stock to be considered as a long term potential stock. We reiterate our “BUY” recommendation on this 5.34% dividend yield stock at the current price of $4.31

Woolworths Ltd

.png)

WOW Dividend Details

Improving pricing promotions to survive the rising competition: Woolworths Limited’s (ASX: WOW) Australian Food and Liquor sales segment managed to improve by 0.4% yoy to $11.1 billion boosted by its extra price investments of over $100 million during the first quarter of 2016, which led to a decrease in average prices of 1.82% (across categories like groceries, produce, bakery and general merchandise). The group opened six new Australian Supermarkets during the quarter resulting to a total of 967 Australian Supermarkets, three Dan Murphy’s totaling to 199 as well as seven BWS stores totaling 1,254 BWS stores (comprises standalone and supermarket attached BWS stores). The group’s New Zealand Supermarkets’ sales rose by 3.6% yoy to NZ$1.6 billion, and comparable sales surged 2.5% yoy boosted by price decrease programs as well as positive domino Stars collectables promotion impact. Meanwhile, WOW’s Home Improvement sales delivered a solid increase of 20.3% yoy to $568 million during the quarter driven by strong Masters Sales which rose by 23.5% yoy to $294 million. Home Timber as well as Hardware sales for the quarter rose 17.1% yoy to $274 million boosted by sales from recent store acquisitions.

.png)

Performance by Segment (Source: Company Reports)

Stock Performance: The shares of WOW plunged over 24.58% during this year to date due to its declining performance impacted by weak consumer sentiment and rising competition. Moreover, the group cautioned investors on the short-term consequences due to the group’s growth efforts across all of its businesses and reported that there would be an impact on its business during the first half of 2016. Management estimates that Net Profit After Tax to be in the range of $900 million to $1.0 billion for first half of 2016 which is 28% to 35% lower than first half of 2015 Net Profit After Tax before significant items. As a result, WOW stock plunged over 14.92% (as of November 16, 2015) in the last four weeks alone. On the hand, the group is focusing on its core Food and Liquor business and investing on price, service as well as loyalty in order to sustain competition from its competitors. Consequently, WOW’s key customer metrics like Net Promoter Score were also improving from the starting of the year. WOW is trading at a relatively cheaper valuation, with a P/E at 13.52x as compared to its competitors. The group also has a decent dividend yield of 6.02%. We remain bullish on WOW and recommend investors to use the recent correction as an entry opportunity and accordingly reiterate our “BUY” recommendation at the current price of $23.40

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.