Greencross Ltd

.png)

GXL Dividend Details

Long term potential driven by the group’s expanding target market: Greencross Limited (ASX: GXL) reported ongoing business growth wherein it’s like-for-like sales (LFL) improved by 6.2% in the YTD of 2016 fiscal year, addressing the investors’ concerns on its organic growth. GXL enhanced its business size by 6x from FY13 to FY15 while its customers spend 5x more at GXL stores which offers retail, vet and grooming services as compared to customers who shop only at its retail stores and 2x spend by customers who use only Greencross vet. Therefore, the firm is targeting growth by offering all the three growth platforms to customers, with which it could boost its market share from 8% (with 332 outlets) to 20%. Accordingly, the group is on track to achieve growth through co-locate stores. GXL’s network is accessible to 59% of the Australian households.

.png)

Pet care market (Source: Company Reports)

GXL improved its retail loyalty membership by 25% yoy to more than 2.9 million members while the Healthy Pets Plus membership surged by 43% yoy to >43,000 members during FY15. On the other hand, the shares of GXL were under pressure witnessing a year to date decline of over 23.2% (as of November 24, 2015) partly due sudden resignation by its CEO Jeffrey David as well as the group’s heavy reliance on acquisitions for growth. However, the group took steps by making CEO contract amendments, who are now required to issue a 12 months prior notice in order to end their employment without cause. Moreover, GXL’s ongoing growth generation indicates its ability to derive synergies from acquisitions. We believe that this recent correction in the stock is an entry opportunity given GXL’s long term potential growth prospects and based on the foregoing, we recommend a “BUY” on GXL at the current price of $6.20

GXL Daily Chart (Source - Thomson Reuters)

Village Roadshow Ltd

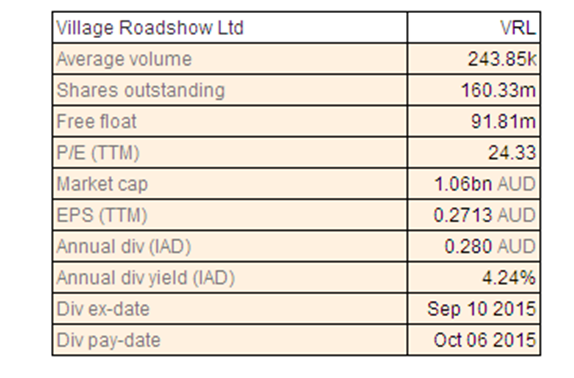

VRL Dividend Details

Better outlook: The shares of Village Roadshow Ltd (ASX:VRL) plunged over 8.8% in the last four weeks (as of November 24, 2015) on the back of the weather conditions impact on its Australian Theme Park division. The group reported a profit before tax decrease to $71.2 million in fiscal year of 2015, as compared to $79.4 million in fiscal year of 2014. On the other hand, the group’s Cinema Exhibition division reported record results from four consecutive years, with its EBIT rising to $56.9 million from $47.7 million in FY14, driven by better performance of its films’ releases during the year (includes The Imitation Game, American Sniper, Mad Max: Fury Road, San Andreas and Jurassic World). Management reported an improving Gold Coast theme parks performance during the fiscal year of 2016 boosted by memberships programs and new program openings.

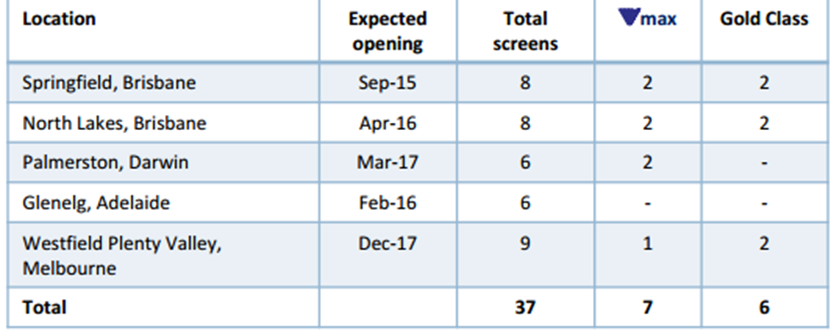

Cinema Exhibition Outlook (Source: Company Reports)

The group estimates a better summer performance next year after witnessing a subdued September holiday performance this year on the back of weather impact. VRL is also targeting Asian opportunities and made an agreement to manage the proposed marine theme park development in China on Hainan Island. VRL estimates its Australian Cinema Exhibition business to continue to deliver growth boosted by better admissions and increased spend per customer. Films like Spectre, Hunger Games and Mockingjay Part 2 have performed well while the division has high expectations on the December release Star Wars: The Force Awakens. VRL acquired 31% of FilmNation Entertainment to enhance its earnings channels in the future. VRL also plans to be the first few ones to test new site-blocking laws under the Government’s anti-piracy legislation. The company also recently updated about the retirement of the director, Dr. Peter D. Jonson and the appointment of Ms. Jennifer Fox Gambrell as the new director. The company also announced some restructuring of committees, the impact of which shall be seen through in due course of time. Nonetheless, we believe that investors could leverage the recent correction in the stock as an entry opportunity and based on the foregoing, we give a “BUY” recommendation on this stock at the current price of $6.83

VRL Daily Chart (Source: Thomson Reuters)

Caltex Australia Ltd

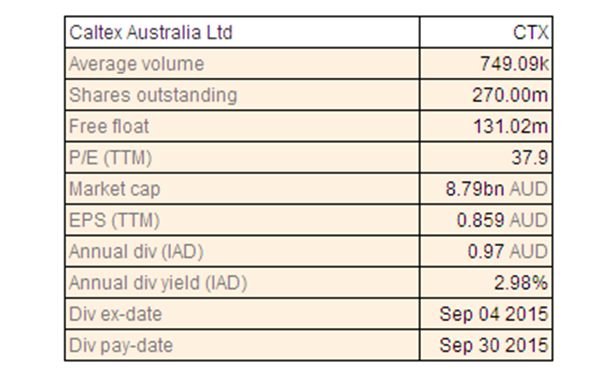

CTX Dividend Details

Ongoing better volumes despite pricing pressure: Caltex Australia Limited (ASX:CTX) reported a net profit after tax of $375 million during the first half of 2015, delivering an outstanding rise of 130% on a year over year basis, on the back of its surplus property sale at Western Australia which contributed over $29 million after tax. Caltex Australia’s efficiency efforts also paid off as the group doubled its EBIT to $551 million in 1H15, against $275 million in the prior corresponding period. Moreover, CTX improved its sales of premium grades from Vortex 95 and Vortex 98 which had offset the falling demand for unleaded petrol to some extent. Solid Vortex diesel product across the group’s retail segment also partly offset the overall pressure, as Vortex premium diesel contributed to over 30% of total diesel sales during the period. The group also shifted its business model in to pure transport fuels business to focus on its core business and enhance competitiveness. As a result, CTX closed its Kurnell refinery last year and focused on cost savings leading to a better cash flows.

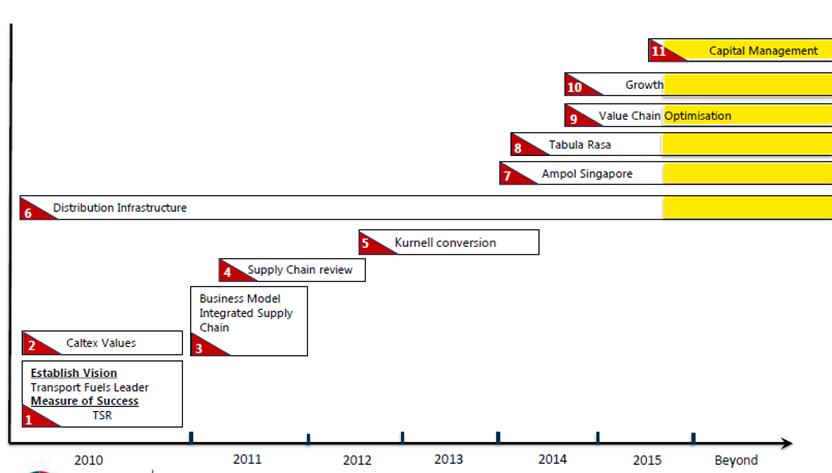

Multiyear transformation strategy to generate growth (Source: company Reports)

Stock Performance: Caltex October unlagged CRM decreased to US$16.23/bbl, as compared to US$18.05/bbl in September. Moreover, Caltex witnessed a negative pricing lag of US$0.57/bbl against September’s US$0.77/bbl impacted by the higher AUD/USD exchange rate and rising petrol and diesel refiner margins. October 2015 realized CRM also decreased from that of September and prior corresponding period.

.png)

Refiner Margin Update (Source: Company Reports)

On the other hand, Caltex continues to improve its CRM sales from production to 580ML from 514ML of September, though this is still below the prior year equivalent when Lytton as well as Kurnell refineries were operating. Meanwhile, Caltex Australia shares improved over 6.5% (as of November 24, 2015) from the last three months and we believe the positive momentum in the stock to grow further. The group intends to focus on its Ampol product sourcing, shipping capabilities as well as expand its supply chain infrastructure and retail network. Lytton supply agreement with BP would boost its volumes in the coming periods and the group continues to focus on Lytton operational efficiency. CTX would continue its Tabula Rasa program of implementing cost and efficiency initiatives. We reiterate our “BUY” recommendation on this stock at the current price of $33.78

CTX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.