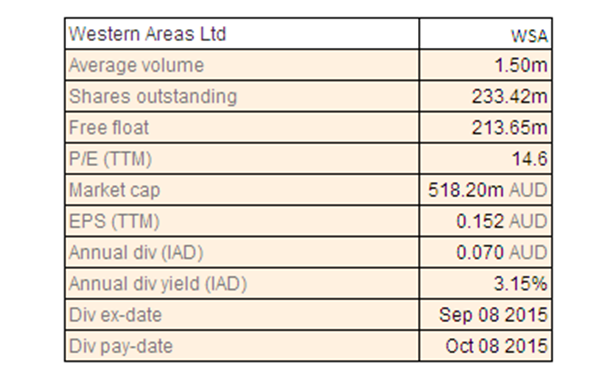

Western Areas Ltd

WSA Dividend Details

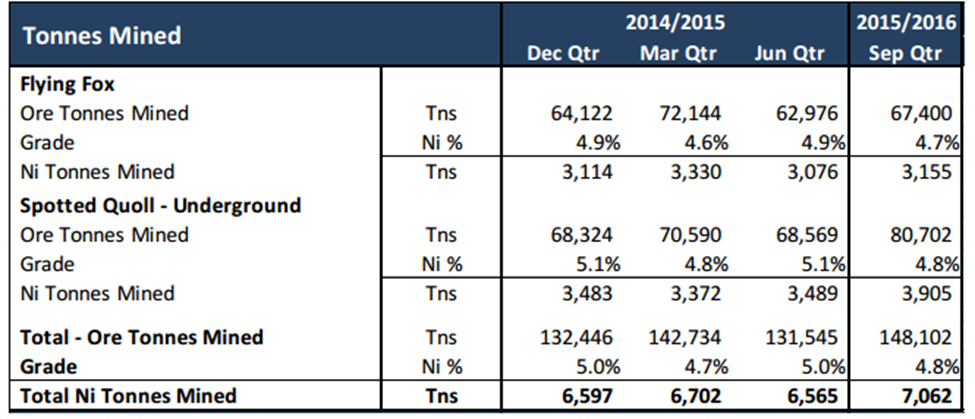

Operating efficiency coupled with better production to further boost performance: Western Areas Ltd (ASX: WSA) was able to generate a net profit after tax increase of 37.5% yoy to $35 million for the fiscal year of 2015, driven by decreasing operating and borrowing costs. The group is also improving its production to offset the falling commodity prices pressure because of which revenues fell 25% yoy to $312.7 million from $320.1 million in FY14, as the group’s realized nickel prices plunged over 4% or $0.33/lb against last year. Accordingly, WSA reported that its Mine production reached 148,102 tonnes of ore at an average grade of 4.8% for 7,062 nickel tonnes which is the highest nickel in ore output from December 2013, for the quarter ending September 30, 2015. Spotted Quoll underground production reached 3,905 nickel tonnes while Mill production produced 6,252 nickel tonnes. WSA reported a unit cash cost of production of $2.26/lb, which is on track to reach its FY16 guidance range of A$2.30/lb to A$2.50. During the AGM, the company sent out positive indications about the commodity prices being expected to rebound in sometime and the company’s capabilities to deal with the cyclical changes.

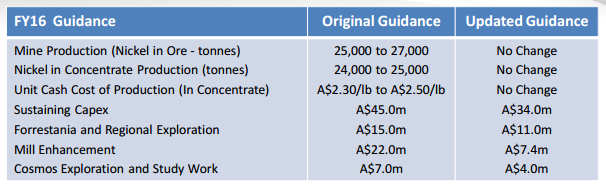

FY16 Guidance (Source: Company Reports)

Moreover, the group achieved a record decline in unit cash costs since three years to $2.31/lb during the FY15, against $2.50/lb in FY14, boosting its overall profitability. Meanwhile, Western Areas also has a solid pipeline of projects and a potential mafic intrusions have been identified from the first round of RC drilling at the Western Gawler project in South Australia. Monax started the field mapping while surface sampling on its new NT-based Mt Ringwood Gold Project are ongoing. There is a scope of visible gold at Great Northern Leases while Western Areas achieved 90% earn-in stage of its Western Gawler Craton Farm-in Agreement. Drilling is also starting at Phar Lap IOCG Project which is a Farm-in and Joint Venture Agreement with Iluka Resources. On the other hand, WSA approved Mill recovery enhancement project during July 2015 with project’s development cost estimated to be over $22 million during six months of construction.

Quarterly Production (Source: Company Reports)

Stock Performance: Western Areas is diversifying its investments in potential capital growth projects like Cosmos exploration and study work during this year. Most of the development work is completed at the Flying Fox mine which would boost its cash flow as well as their target of capital expenditure cut during fiscal year of 2016. Western Areas also built a flexible balance sheet (with over pre-consolidated cash at bank of $59.0 million) and is also making efforts to decrease its discretionary capital and exploration spend. Earlier, the group stopped the mine development at Flying Fox during FY14 for six months. Western areas wants to be conservative and intends to achieve an optimal mining rate to maximize margin, due to short term nickel price volatility. On the other hand, the group’s stock plunged 42.38% during this year to date, as well as fell over 12.20% in the last three months (as of November 26, 2015), impacted by the ongoing commodityprice pressure. But the group generated a solid financial performance even during the tough market conditions which boosted the investor’s sentiment. The stock got little boost from the Forrestania operations which are restored with power and the group estimates a minimal impact during its full year of 2016. The steady nickel prices estimations during the FY16, might result to positive quotational pricing adjustments. WSA is also trading at a low P/E of about 14x, as compared to its peers. Based on the foregoing, we give a “BUY” recommendation on this 3% dividend yield stock at the current price of $2.30

WSA Daily Chart (Source: Thomson Reuters)

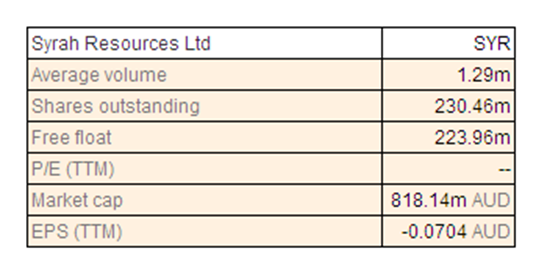

Syrah Resources Ltd

SYR Details

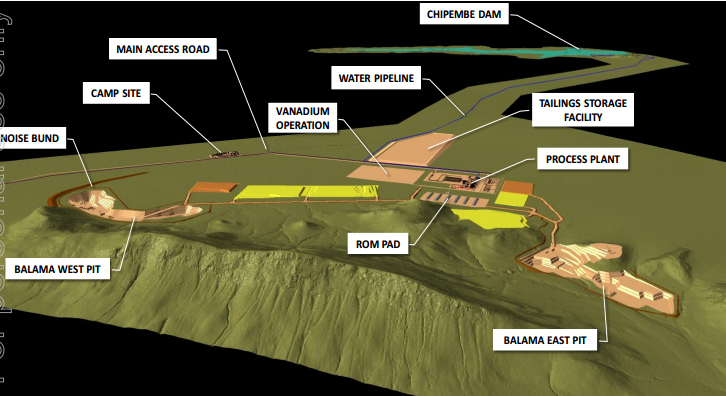

Building long term prospects for Balama project: Syrah Resources Ltd (ASX: SYR) rose over $211 million of capital to fund the development of its Balama project. The group is also making sales negotiations with several graphite traders and end customers. Accordingly, SYR recently signed a statement of sales intent agreement with a leading refractory producer which might buy up to 15,000 tons per annum of natural graphite for its production facilities across the world. The group also made a three year product sales agreement with Morgan Hairong for 2,000 tpa of uncoated spherical graphite as well as a three year marketing agreement for 5,000 tpa of uncoated spherical graphite and 2,000 tpa of coated spherical graphite. Syrah Resources also signed a 20 year licensing agreement with Morgan Hairong for its proprietary spherical graphite coating technology. SYR is continuously receiving positive feedback from the potential clients over its higher quality uncoated spherical graphite Balama. Syrah Resources project development activities of Balama is on track and the company estimates to start the production by next year end and production ramp up by the first quarter of 2017. Syrah estimates its Balama project to produce over 270,000 tonnes of +95% graphite for world markets in 2017. The company scheduled the production of the project at 356,000 tonnes per annum (tpa) for the first 10 years. The group reported a proven and probable ore reserve of 81.4 Mt at an average grade of 16.2% total graphitic carbon.

Balama Project (Source: Company Reports)

SYR received the necessary government approvals and made a three year Offtake Agreement with China Aluminum International Engineering Corporation for 80,000 tpa. Syrah Resources also entered into an MOU with Marubeni Corporation. Ongoing contract wins by Syrah boosted the stock by over 14.06% (as of November 26, 2015) in the last four weeks and we believe the positive momentum in the stock would continue in the coming months given its solid Balama project prospects. We reiterate our “BUY” recommendation on the stock at the current price of $3.53

SYR Daily Chart (Source: Thomson Reuters)

AWE Ltd

.png)

AWE Details

Optimizing efforts coupled with enhancing resource potential prospects to boost growth: AWE Limited (ASX: AWE) announced about its improved production forecast for FY2015-16 during its recent AGM. AWE is focused on achieving sustained higher production from the BassGas and Sugarloaf projects and stable production from Casino. The Lengo gas project and the Ande Ande Lumut (AAL) oil project are also expected to help AWE cater to the key Asian markets. We also note that AWE’s portfolio of 2P Reserves and 2C Resources has reached 236 mmboe (an increase of 75%).

.png)

Guidance (Source: Company Reports)

AWE’s revenues fell over 27% during the September quarter of 2015 against the earlier quarter, impacted by the ongoing falling oil prices. On the other hand, the group is building solid resource potential wherein its north Perth Basin, Western Australia delivered solid results during the September quarter, with the Waitsia, Senecio, Synaphea and Irwin gas fields gross combined 2P Reserves and 2C Resources improving to 721 Bcf. AWE has resource potential of >22 years of production at current rates with net 2P Reserves of 114.4 mmboe, and 2C Resources of 121.9 mmboe with the ability to convert most of these assets to 2P within the short to medium term. Meanwhile, Waitsia-1 flow testing delivered a combined gas flow rate of more than 50 mmscf/d from the conventional Kingia and High Cliff Sandstone formations. Sugarloaf AMI also contributed to AWE’s Reserves and Resources of a combined 2P Reserves and 2C Resources of 65 mmboe. AWE is also focusing to drive its operational efficiency and accordingly reported a 3% production decrease to 1.38 mmboe in September quarter of 2015 against the earlier quarter, due to initial flush production from the Pateke-4H well at Tui. The group’s cost cutting initiatives paid off during the quarter and accordingly Field opex could be cut by 21% with overall investment expenditure (exploration and development) drop by 29%. AWE reduced its staff by over 30% in its Sydney and New Plymouth offices and intends to shut the Jakarta project office by this year end. BassGas production generated 23% increase driven by the Yolla-5 and 6 development wells while Sugarloaf production rose by 7% as over 20 wells (gross) were brought to production. AWE is also offloading its non-core assets by divesting its 57.5% interest in the Cliff Head oil project to Elixir Petroleum.

.png)

Third quarter Production highlights (Source: Company Reports)

Stock Performance: The shares of AWE plunged over 57.39% (as of November 26, 2015) in the last six months on the back of challenging market conditions as well as the slowdown of economy in China. On the other hand, the group is implementing solid cost cutting initiatives and executed oil price hedging program for FY16 which could boost its cash flow further. We believe that investors need to use the recent correction as an opportunity given AWE’s solid long term potential and accordingly, we reiterate our “BUY” recommendation on AWE at the current market price of $0.63

AWE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.