XERO FPO NZ

.png)

XRO Details

Solid performance driven by Subscriber’s Growth: XERO FPO NZ (ASX: XRO) stock surged over 22.81% (as of November 13, 2015) in the last four weeks driven by the group’s solid performance wherein total operating revenue rose by 71% year on year (yoy) to $92.86 million in first half of 2016. The total Australian subscribers and New Zealand subscribers rose by 66% and 37% to 262,000 and 163,000, respectively; and the company exceeded 100,000 paying subscribers in United Kingdom during 1H16. Xero also enhanced its North American subscribers by 114% yoy to 47,000 in 1H16.

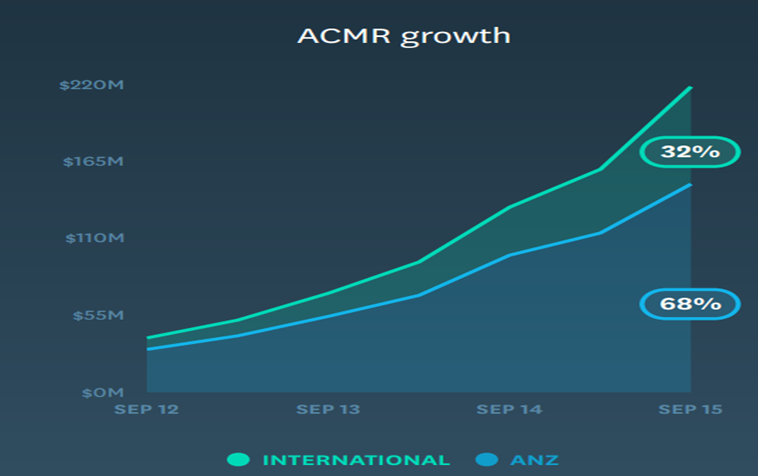

Annualized committed monthly revenue growth (Source: Company Reports)

XRO earlier forecasted that its recurring revenue model which is implemented in 2016, would generate a growth of 71% for annualized committed monthly revenue of $159.3 million in 2016 fiscal year. We remain bullish on the stock and accordingly reiterate our “BUY” recommendation at the current price of $17.93

XRO Daily Chart (Source: Thomson Reuters)

Flight Centre Travel Group Ltd

.png)

FLT Dividend Details

TTV growth, acquisitions to drive performance: Flight Centre Travel Group Ltd (ASX: FLT) which recently agreed to acquire 51% interest in AVMIN, a Brisbane based firm to enhance its leisure and travel portfolio, has reaffirmed its FY16 guidance for an underlying profit of $380 million to $395 million. Further, 1Q16 Australian outbound travel surged 2.3% in total. The growth drivers for FY16 range from Australian profit and sales, contributions from off-shore as businesses gain scale, market growth, contribution from Top Deck and network expansion with 6-8% growth globally. The company’s general cash is up 18.6% to record $564.7m and has only $32.8m in debt.

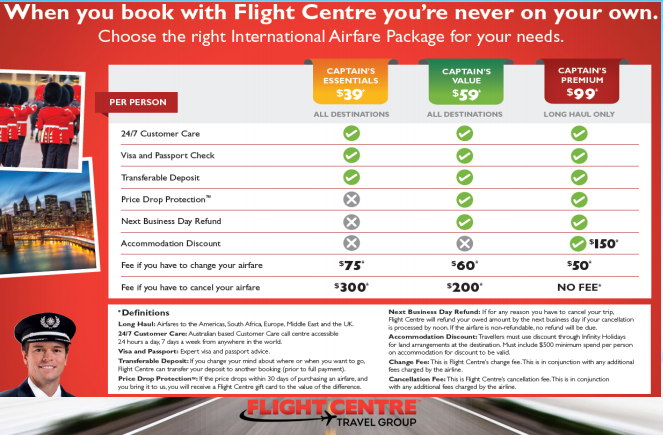

International Airfare Packages (Source: Company Reports)

FLT has been building its performance across international markets, wherein UK and Ireland, USA, South Africa and Singapore reported record earnings before interest and tax during fiscal year of 2015 leading to >$100 million overseas EBIT for the first time. FLT generated revenues increase by 6.8% yoy to $2.4 billion for the fiscal year of 2015, boosted by major total transaction value improvement by 9.7% yoy to $17.6 billion. The group expects a decent outlook with IATA forecasting a 4.1% compounding annual growth in passenger numbers globally through to 2034, boosting FLT’s addressable market. FLT stock is trading at reasonable P/E of 14.33x and has a dividend yield of around 4.16%. We maintain “BUY” recommendation to the stock at the current price of $36.51

.png)

FLT Daily Chart (Source: Thomson Reuters)

Cash Converters International Ltd

CCV Details

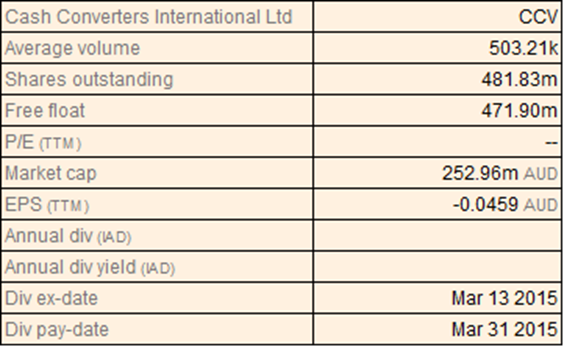

Efforts to recover the growth track: Cash Converters International Ltd (ASX: CCV) shares fell over 49.02% (as of November 13, 2015) during this year to date impacted by a class action claim on behalf of borrowers resident in Queensland who took out personal loans from the Company’s subsidiaries during the period from 30 July 2009 to 30 June 2013. The court also recently approved the NSW class action settlement. On the other hand, Cash Converters has a solid online business and generated revenue increase of 13.0% on a year over year basis to $374.9 million in the fiscal year of 2015. Emerchants signed a multiyear contract with CCV, wherein Cash Converters would use Emerchants customized prepaid debit cards to disburse cash advance load funds for in store as well as online customers. Having an outstanding dividend yield of 7.69% and attractive P/E of 9.17x, we give a “BUY” at the current price of $0.52

CCV Daily Chart (Source: Thomson Reuters)

Capitol Health Ltd

.png)

CAJ Dividend Details

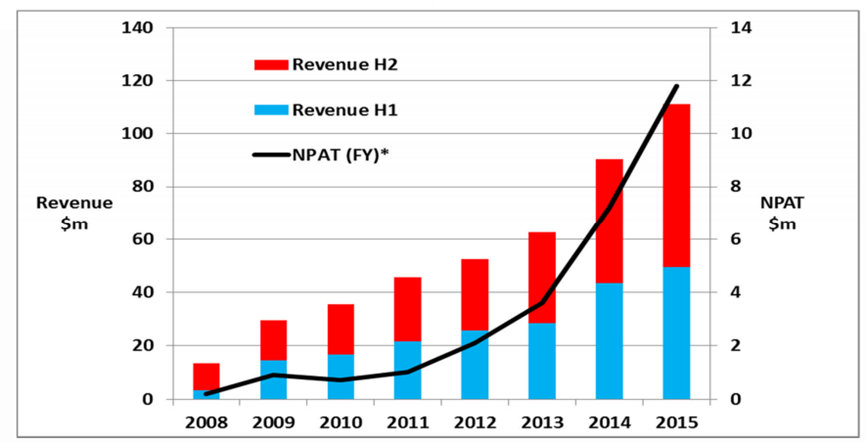

Rising specialty diagnostics demand and MRI players preference by government to boost growth: Capitol Health Ltd (ASX: CAJ) recently entered into a MOU with Enlitic to leverage Enlitic’s expertise and Artificial intelligence for delivering better patient outcomes. The group is expanding its NSW radiology in Sydney through Liverpool diagnostics acquisition and finished its Southern radiology and Eastern Radiology acquisitions during April and July months, respectively. However, management reported that the regulatory ambiguity coupled with disruptions of referral patterns would lead to a slower than estimated growth in FY16. In view of the most likely temporary but unfavorable disruption to normal referral patterns, the guidance for FY16 has been updated with a 4-6% reduction in gross revenues otherwise expected. Therefore, CAJ stock plunged over 31.78% in last four weeks alone (as at November 13, 2015).

Maintaining a solid growth track (Source: Company Reports)

But, the Government’s favor towards MRI market players, rising ageing population, acquisition synergies, improved priority for early detection of diseases and CAJ’s focus on sub specialty radiology would boost its performance further in the coming periods. We maintain “BUY” recommendation on the stock at the current levels of $0.365

CAJ Daily Chart (Source: Thomson Reuters)

Dick Smith Holdings Ltd

.png)

DSH Dividend Details

Outstanding dividend yield: Dick Smith stock plunged over 64.52 (as of November 13, 2015) year to date on the back of lower than projected fiscal year of 2015 performance as well as subdued FY16 outlook. But this correction placed Dick Smith at a very cheaper of P/E of 4.66x as compared to its retail peers. Dick Smith also has an outstanding dividend yield of 16.11%. Moreover, DSH sales rose by 6.9% yoy in the first quarter of 2016 and the company is seeking to enhance its network to 420-430 stores by FY2017, by opening over 15 to 20 new stores annually. The group is also improving its private labels penetration, which accounts more than 12.5% of its FY15 sales and targets to be more than 15% of sales by 2017 fiscal year. We remain positive on the stock despite the recent crash and accordingly give a “BUY” recommendation at the current price of $0.745

DSH Daily Chart (Source: Thomson Reuters)

MMA Offshore Ltd

.png)

MRM Dividend Details

New contract win and subdued outlook: MMA Offshore Ltd (ASX: MRM) recently won a contract from Woodside worth over $50 million. Through this contract, MRM will provide three vessels to support Woodside’s offshore Northwest Shelf, Pluto and AusOil production assets. Though the management gave a subdued outlook given the challenging offshore marine industry and MRM’s lower than expected performance during the first four months of FY16, MRM still seem to have potential given the new contract win and the ability to generate positive operating cash flow with full year EBITDA expected to be $75-85 million. The MRM stock plunged over 50.94% in the last four weeks (as of November 13, 2015). However, this correction placed MRM at very cheap valuation while the company has an outstanding dividend yield of 21.15%. We give a “BUY” recommendation at the current price of $0.26

MRM Daily Chart (Source: Thomson Reuters)

BHP Billiton Ltd

.png)

BHP Dividend Details

Solid asset quality: BHP Billiton Limited (ASX: BHP) recently reported that at its Samarco operations, the Fundao dam failed leading to major damage on the site. Therefore, BHP stock fell over 18.46% (as of November 13, 2015) in the last four weeks. But, the group is making solid efforts to offer instant necessary support to address the fatality and subsequently investigate the site. BHP has built a diversified assets base and developing four major projects worth of US$7.0 billion in Petroleum, Copper and Potash as of September 2015 quarter. Moreover, the group’s share of Samarco production was 14.5 Mt while Samarco contributed only 3% of the BHP’s underlying EBIT. BHP mentioned that it will review its iron ore production guidance for the year. We believe the group still has a solid long term potential and the recent correction offers attractive entry to investors looking for a high dividend stock with BHP offering an outstanding dividend yield of 8.33%. Accordingly, we give a “BUY” recommendation on the stock at the current price of $20.23

.png)

BHP Daily Chart (Source: Thomson Reuters)

Webjet Ltd

.png)

WEB Dividend Details

Positive Outlook: Webjet Limited (ASX: WEB) issued a positive outlook for FY16 and estimates an EBITDA increase of 20% yoy to $33.5 million in FY16, driven by the ongoing growth across all of its business segments. The group also posted a decent FY15 performance with TTV improving by 31% yoy while revenues rising by 21% yoy to $119.1 million. The shares of WEB surged over 46.39% in the last six months (as at November 13, 2015) and we believe the momentum to continue and accordingly give a “BUY” recommendation to this 2.56% dividend yield stock at the current price of $5.27

WEB Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

ANZ Dividend Details

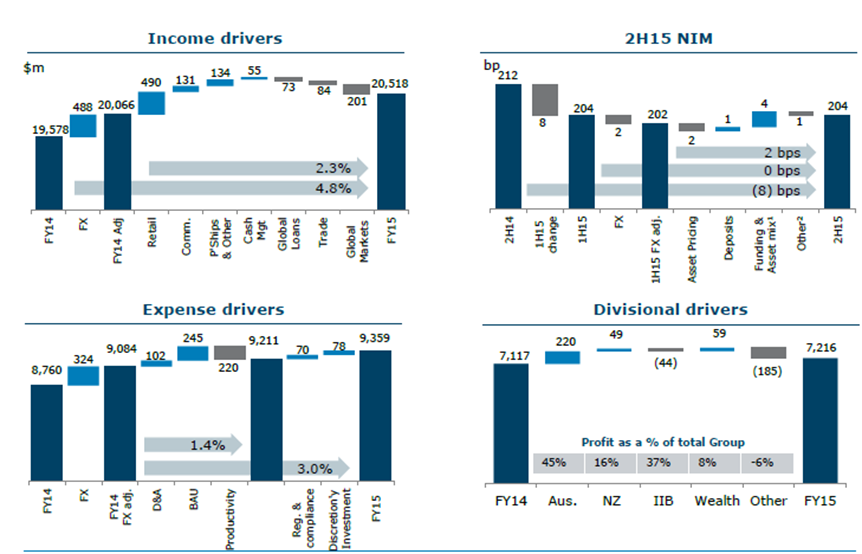

Ongoing core business growth: Australia and New Zealand Banking Group Ltd.’s (ASX: ANZ) shares also corrected over 20.54% (as of November 13, 2015) in the last six months on investors’ concerns over its china division performance due to slowdown in China. Accordingly, the China’s cash profit fell by 2% in International and Institutional Banking. But, ANZ’s core Australia Division and New Zealand delivered a cash profit increase of 7% yoy and 3% yoy, respectively, in fiscal year of 2015 driven by New South Wales customer’s growth and better market penetration through home loans and credit cards growth. The group improved its capital position and almost doubled its total assets to $890 billion. Recently, ANZ confirmed that it expected to fully frank dividends for the foreseeable future and also got over with a scheduled update of the Information Memorandum for its Australian dollar debt issuance program for the issue of covered bonds to wholesale investors.

Financial Performance (Source: Company Reports)

The recent correction in the share prices placed ANZ at attractive valuation, with ANZ trading at a very cheap P/E of 9.69x. The bank also has solid annual dividend yield of over 6.88%. We continue to maintain our “BUY” recommendation on the stock at the current levels of $26.31

ANZ Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd.

.png)

NAB Dividend Details

Improving capital position: National Australia Bank (ASX: NAB) improved its asset quality during fiscal year of 2015, wherein its total charge for Bad and Doubtful Debts fell by 5% yoy to $823 million on the back of decrease in Australian Banking and UK Banking. Meanwhile, Nippon Life Insurance might offer a deal in the range of 200 billion and 300 billion yen or US$2.5 billion, to buy National Australia Bank’s insurance operation, which would further boost NAB’s capital position. NAB is investing over 300 million in its Wealth business for the next four years and also focusing on customer relationships.

.png)

National Australia Bank performance (Source: Company Reports)

Moreover, the correction in the stock placed NAB at attractive valuation with a relatively cheaper P/E of 11.18x with a decent dividend yield of 7.01%. We maintain our positive stance and reiterate our BUY recommendation on the stock at the current stock price of $28.25

.png)

NAB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.