AGL Energy Limited

.png)

AGL Details

Pressure on wholesale gas margin: AGL Energy Limited (ASX: AGL) recently announced about gas market constraints. In addition, the company stated for higher than expected acquisition of wholesale gas for the first quarter of FY17 from the spot market and other short-term sources at the back of recent reduction in Queensland gas supply owing to safety issues at a key supplier’s project and rising demand at the AGL Torrens power station. AGL specified that the peculiar high prices prevalent in the spot market from strong East Coast demand will lead to a negative impact of approximately $35 million on its pre-tax wholesale gas margin in the first quarter of FY17.

.png)

Australia’s Renewable Energy Target (Source: Company Reports)

The company expects the total pre-tax contribution to margin from its Energy Markets gas portfolio in FY17 to be lower than FY16 by at least $100 million while there is no change to the FY16 underlying profit guidance. We believe that the stock is “Expensive” at the current price of $20.00

.PNG)

AGL Daily Chart (Source: Thomson Reuters)

Spark Infrastructure Group

.png)

SKI Details

Capital raising and business expansion: Spark Infrastructure Group (ASX: SKI) announced that Victoria Power Networks Pty Ltd reached an agreement with US investors to place about US $500 million of bonds in USPP market while the total proceeds raised are about A$657 million which will be used for refinancing USPP debt maturing in November 2016 and bank debt bridging facilities. Recently, the group also reported that TransGrid‘s funding entity, NSW Electricity Finance Pty Ltd would be placing US$700 million and A$75 million of bonds via US private placement market with four tranches. With this move, TransGrid would diversify its funding and extend its debt maturity profile. SKI is focusing on organic growth by improving efficiency, productivity and managing costs along with positioning with advanced technology. But, Spark Infrastructure has divested 8% of economic interest in DUET Group at price of $2.25 per security.

However, the Group has been diversifying its portfolio and accordingly, has holdings in SA Power Networks, CITIPOWER, Powecor and TransGrid. On the other side, SKI has a decent dividend yield while the management guided that its distribution would reach 14.5 cents per share (cps) in FY16, 15.25 cps in FY17 and 16 cps for FY18. The stock has surged 22.89% in the last three months (as at July 13, 2016). We recommend a “buy” on the stock at the current market price of $2.51

SKI Daily Chart (Source: Thomson Reuters)

ERM Power Ltd

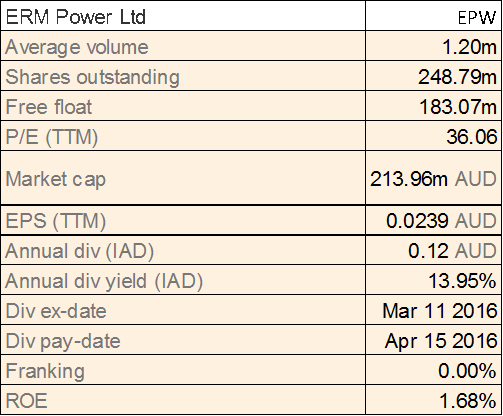

EPW Details

Weak outlook:ERM Power Ltd (ASX: EPW) recently affirmed its FY16 guidance of EBITDA $81 - $85 million. Moreover, for FY17 the group guided that its US business would rise in terms of growth, margin and cooperating expenditure. On the other hand, ERM Power reported that its Oakey Power Station, which is operating as a merchant plant, would underperform in FY16 and expects an EBITDA of $16 million.

The group’s Australian business also has a bleak outlook on margins due to load growth while average gross margin would be under pressure for FY17. Consequently, the stock has plunged over 41% in the last four weeks alone (as of July 13, 2016). Despite this fall, we believe that the stock is still trading at a relatively high P/E. Given the weak outlook, we give an “Expensive” recommendation on the stock at the current price of $0.895

EPW Daily Chart (Source: Thomson Reuters)

Ausnet Services Ltd

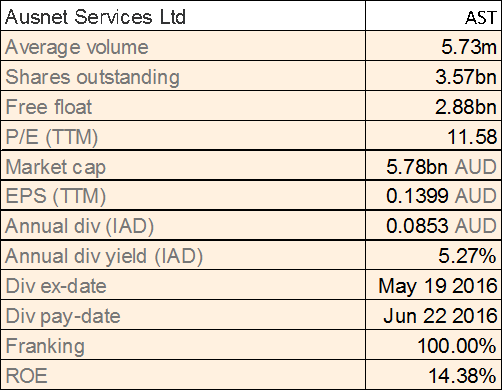

AST Details

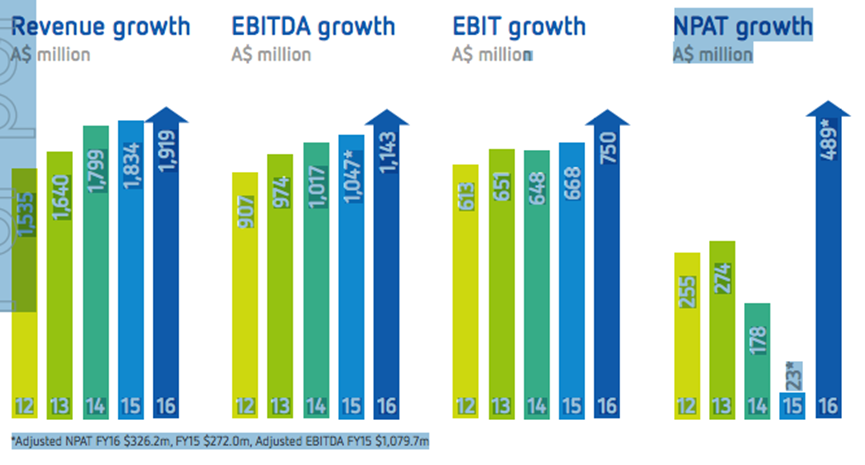

Positive AER decision:Ausnet Services Ltd (ASX: AST) recently reported that Australian Energy Regulator (AER) accepted the group’s proposed faster capital recovery, especially where assets are no longer utilized. Cash flow from depreciation has increased by over $100 million from the Preliminary Decision. The group welcomed AER’s approval of capital expenditure related to bushfire safety obligations and the inclusion of a mechanism to include upcoming Government mandated expenditure. Meanwhile, AST also reported decent a full year adjusted net profit for FY16 which rose by 20% to $326.2 million on a 4.6% rise in sales to $1.92 billion. Its electricity distribution network reported a significant 26.9% rise in EBITDA on 9.5% rise in revenues driven by regulated price increase and metering revenues. AST is also prompt in integrating new technologies into its network, and accordingly, the group is currently running the first trial of its kind in Australia involving 14 homes enabled with solar panels and battery storage with a common connection to the grid.

Strong FY16 performance (Source: Company Reports)

AST has a debt to the tune of $ 6 billion in books while the company announced for raising $148 million by issuing HKD875 million bonds issue. On the other hand, AST stock already rallied over 10.03% (as of July 13, 2016) in the last three months placing them at higher levels. Accordingly, we rate the stock as “Expensive” at the current market price of $1.655, and would review the stock at a later date.

AST Daily Chart (Source: Thomson Reuters)

Duet Group

.png)

DUE Details

Growth prospects from Energy Developments: Duet Group (ASX: DUE) has completed the rollout of Eze software investment suite across its operations to centralize its existing businesses and seamlessly integrate new business into the platform. The group recently published the Economic Regulation Authority (ERA) of Western Australia’s final decision on DBP’s proposed revisions to the 2016-2020 Access Arrangement for the Dampier to Bunbury Natural Gas Pipeline (DBNGP). Based on ERA’s final decision, there is a 6% increase in the total allowed revenue (real) against the draft ERA decision issued in December 2015 and a 20% rise in total allowed capital expenditure (real) for 2011-15 against the draft. Over 35% rise in total allowed capital expenditure (real) for 2016-20 is expected against draft decision. Meanwhile, Spark Infrastructure has divested 8% of economic interest in DUET Group at price of $2.25 per security. Origin Energy sold its Cullerin Range wind farm in NSW (financial close reached on July 13, 2016) to Duet Group for $72 million and the asset sales included infrastructure and wind energy assets, coupled with its interests in oil and gas fields in the Cooper and Perth basins. Energy Developments (EDL) has also acquired Pecan Row from Energy Systems Group, and has inked agreements with Territory Generation and Anglo American.

The expansion at Oaky Creek’s capacity has also been increased. DUE stock has an attractive dividend yield and declared a dividend of $0.09 per share while guided a dividend of 18.5 cents for FY17. We give a “Hold” on the stock at the market price of $2.51

.PNG)

DUE Daily Chart (Source: Thomson Reuters)

Water Resources Group Ltd

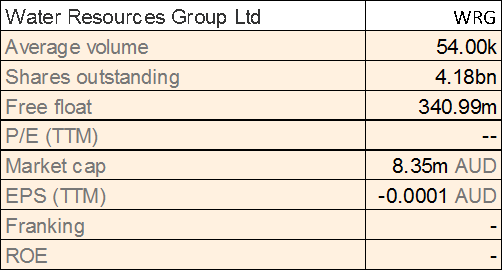

WRG Details

Developing New water treatment solutions: Water Resources Group Ltd (ASX: WRG) has developed a technology solution known as Free Radical Generator (FRG) which is an improvement to its earlier launched AiR

2O

3 and accordingly got full patent protection. FRG has potential to provide unique solutions to number of water contamination problems such as Contaminated drinking water, medical waste water, industrial and mining water, purification of ground water, grey water treatment and pre-treatment in waste water plants. On the other hand, the group’s stock is trading with poor volumes this year. Moreover, WRG has reported for net operating cash flows of ($54,000) during the March quarter leading to ($185,000) in this year to date (as of March quarter). We believe that the stock is “Expensive” at the current market price of $0.002

WRG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.