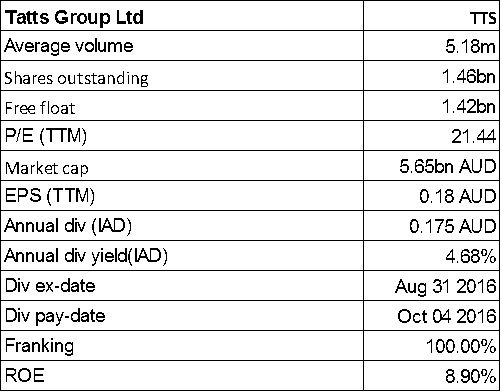

Tatts Group Limited

TTS Details

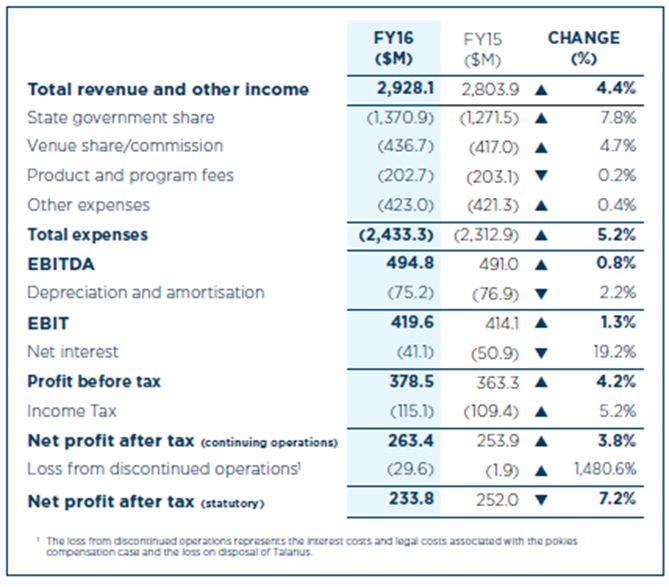

Weak bottom line in FY 16: Tatts Group Limited (ASX: TTS) reported a 7.2% fall in the net profit from ordinary activities to $233.8 million in FY 16 after the loss on sale of Talarius and the repayment of the interest benefit to the State of Victoria in the Pokies compensation decision.

FY 16 Financial Performance (Source: Company Reports)

As a result, TTS stock fell over 6.45% in the last four weeks (as of September 20, 2016), and is still trading at a high P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $3.72

TTS Daily Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Details

Building development projects: Transurban Group (ASX: TCL) announced that Transurban Finance Company Pty Ltd has priced USD 550 million of senior secured 10.5 year notes representing second US 144A issuance, and the group earlier reported a proportional toll revenue growth of 17.5% to $1,946 million in FY 16. TCL has reported the statutory profit from ordinary activities of $22 million while the proportional earnings before interest, tax, depreciation and amortization (EBITDA) and before significant items grew by 14.8% to $1,480 million.

.png)

FY 16 Statutory results (Source: Company Reports)

In FY 16, TCL has distributed dividend of 45.5 cents per security and in FY17 TCL has given the distribution guidance of 50.5 cps, reflecting 11.0 per cent increase on the FY16 distribution. Moreover, TCL has $9 billion of development projects to improve customers’ trips in Melbourne, Sydney, Brisbane and Greater Washington Area.

On the other hand, the stock fell over 7.9% in the last four weeks (as of September 20, 2016) due to concerns over interest rates. TCL stock is also trading at a very high P/E. As a result, we give an “Expensive” recommendation on the stock at the current price of $10.85

TCL Daily Chart (Source: Thomson Reuters)

Santos Ltd

.png)

STO Details

New operating model expected to lift productivity:Santos Ltd (ASX: STO) recently announced that Anthony Neilson will be replacing the outgoing chief finance officer, Andrew Seaton. The group’s operated drilling program along with Beach Energy for South Australian Gas revealed that five?well appraisal and development campaign progressed on the central flank of the Big Lake field, while the results have been found to be in line with pre?drill estimates. Moreover, down?flank extension of gas reservoirs has been confirmed. On the other hand, STO in the first half 2016 reported net loss of US$1,104 million, impacted by the impairment charge for GLNG of US$1,050 million after tax and lower oil prices. However, STO has made the good progress in the first half and is forecasting a free cash flow breakeven oil price of US$43.50 per barrel for 2016, which is down from US$47 per barrel.

.png)

First half of 2016 Financial Performance (Source: Company Reports)

In addition, the establishment of the new operating model for STO would enhance their productivity and drive long-term value for shareholders in a low oil price environment. Meanwhile, STO stock fell 25.05% in the last four weeks (as of September 20, 2016) placing them at attractive levels. We give a “Buy” recommendation on the stock at the current price of $3.59

STO Daily Chart (Source: Thomson Reuters)

Spark New Zealand Ltd

.png)

SPK Details

Decent growth for FY 17:Spark New Zealand Ltd (ASX: SPK) reported an EBITDA growth of 2.5% in FY 16 driven by their efforts of ongoing management of cashflow and capital. Mobile and IT Services revenue and margins also improved. SPK has completed the four year, $238m re-engineering program to upgrade the key customer service IT systems. The re-based revenue grew 2.5% to $83m due to strong Mobile, IT Services and Broadband performance. The launch of Wireless Broadband is expected to provide further growth and cost reduction in the future. Moreover, SPK expects ordinary dividend of 22 cps and declared a special dividend of 3 cps for FY 17. The ordinary dividend is expected to be fully imputed and the special dividend is anticipated to be at least 75% imputed. The revenue is expected to grow 0%-3% in FY 17.

.png)

FY 16 Financial Performance (Source: Company Reports)

EBITDA excluding potential net gains on sale for Mayoral Drive Carpark is estimated at $17m-$19m and forecasted to grow 0%-2%. The earnings per share for FY 17 are expected to be 21 cents as compared to 20 cents in FY 16.

The company has also indicated that Spark Finance Ltd recently launched for NZ$125,000,000 of fixed rate bonds. Meanwhile, SPK stock rose over 15.5% in the last six months (as of September 20, 2016), and still the company is having a good dividend yield. We give a “Hold” recommendation on the stock at the current price of $3.54

SPK Daily Chart (Source: Thomson Reuters)

Rio Tinto Ltd

.png)

RIO Details

Improving cash flow:Rio Tinto Limited (ASX: RIO) has reported consolidated sales revenues of $15.5 billion in 1H 2016 which is $2.5 billion lower than the 1H 2015 due to the decline in commodity prices. But, RIO has focused on cost reduction, and accordingly reduced costs by $0.6 billion and maintained 33% EBITDA margins in 1H 2016.

.png)

1H 2016 Financial Performance (Source: Company Reports)

The group is boosting its cash flow and has generated net cash from operating activities of $3.2 billion and reported underlying earnings of $1.6 billion. Moreover, RIO has delivered strong operational performances in iron ore, bauxite and aluminum, with all key commodities on track to meet full year guidance. RIO has also terminated its Management Services Agreement with Bougainville Copper Limited (which is now an independently managed Papua New Guinea company) before stipulated time.

Meanwhile, the stock rose 6.3% in the last three months (as of September 20, 2016). Accordingly, we give a “Buy” recommendation on the stock at the current price of $47.65

RIO Daily Chart (Source: Thomson Reuters)

QBE Insurance Group Ltd

.png)

QBE Details

Profits fell significantly in 1H 2016:QBE Insurance Group Ltd (ASX: QBE) reported a fall in the underwriting profit from $401 million to $54 million in the first half 2016 while the net profit after tax fell to $265 million from $455 million.

.png)

Credit Ratings (Source: Company Reports)

As a result, QBE stock fell over 16.6% in the last three months (as of September 20, 2016), and also trading at a high P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $9.58

QBE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.