Infomedia Ltd

.png)

IFM Dividend Details

Positive Outlook: Infomedia Ltd (ASX: IFM) board decided to change leadership to address the challenging market automotive sector conditions. The Board also reported that they were concerned on the delay of the realized revenues from its new business even though IFM built a strong pipeline. Hence, the stock declined over 37.54% in the last six months (as of December 29, 2015). On the other hand, the group delivered a decent first quarter of 2016, and witnessed a revenue increase of 15% year on year (yoy) while profit rose by 2% as compared to the prior corresponding period (pcp). Management estimates a positive fiscal year of 2016 performance and accordingly is expanding its projects pipeline. JLR Australia authorized the rollout of Superservice Triage to its dealer network in Australia. Hyundai America (HMA) installations are on track in America while the rollout of the group’s Triage and Superservice Connect are progressing well in Europe. But, Infomedia estimates NPAT margin pressure during fiscal year of 2016, impacted by the group’s investments to enhance its potential business. IFM expects its fiscal year of 2016 NPAT would witness a financial impact but not more than $2.5 million. Meanwhile, the company estimates to maintain its dividend policy in the range of 75% to 85% of net profit after tax for FY16.

.png)

Sales by Region (Source: Company Reports)

We believe that IFM is trading at attractive valuations with a reasonable P/E while the stock has a good dividend yield. The stock recovered over 11.76% (as of December 29, 2015) in the last five days and we believe IFM has the potential to recover in the coming months. Based on the foregoing, we give a “BUY” recommendation on IFM at the current price of $0.725

IFM Daily Chart (Source: Thomson Reuters)

Asaleo Care Ltd

.png)

AHY Dividend Details

Strong distribution network: Asaleo Care Ltd (ASX: AHY) reported that the company faced challenging market conditions during first half of 2015 on the back of falling Australian dollar impact, coupled with increase in competition from new entrants in the Tissue and Personal Care categories. As a result, the stock fell over 15.16% in the last six months (as at December 29, 2015), as the management’s forecasts only a low to mid-single digit growth of the group’s NPAT and EBITDA for full year of 2015. However, Asaleo improved its bottom line, wherein NPAT rose by 15.2% yoy to $32.5 million in 1H15, while EBIT rose by 11.8% yoy to $51 million.

Asaleo Care Tissue business delivered a strong half with Tissue EBITDA rising by 15.3% driven by 4.3% growth (in consumer tissue) on its higher margin core brands. The group is expanding its brands presence (Sorbent, Handee, Libra and TENA) through its aggressive marketing efforts. AHY entered into a buyback program of up to 10% of issued capital (or up to $100 million) from fourth quarter of 2015, which would further support the stock in the coming months. The group has a good dividend yield. We reiterate our “BUY” recommendation on the stock at the current price of $1.595

AHY Daily Chart (Source: Thomson Reuters)

Mortgage Choice Ltd

.png)

MOC Dividend Details

Outstanding dividend yield: Mortgage Choice Ltd (ASX: MOC) shares plunged over 18.80% in the last six months (as at December 29, 2015) on the back of cyclical nature of the housing market and ongoing volatile conditions. On the other hand, the group reported a strong first quarter of 2016, and delivered a Home Loan Approvals and Home Loan Settlements growth of 3.3% and 8.4%, respectively, over Q1 FY15. Accordingly, MOC generated a Financial Planning and group cash revenue increase of 75.3% and 10%, respectively, to $2.08 million and $48.5 million.

.png)

Trading Update Q1 FY16 (Source: Company Reports)

Meanwhile, we believe that the recent correction in the stock placed MOC at attractive valuations with a cheaper P/E. The group also has an outstanding dividend yield. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $1.89

.png)

MOC Daily Chart (Source: Thomson Reuters)

Incitec Pivot Ltd

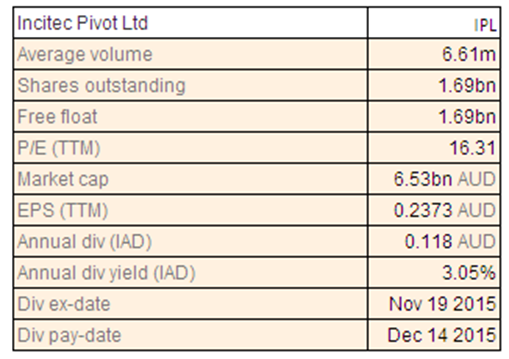

IPL Dividend Details

Enhancing efficiency: Incitec Pivot Ltd (ASX: IPL) was able to generate a bottom line growth of 12% yoy for fiscal year of 2015, despite tough market conditions as its Business Excellence efforts have paid off. IPL delivered a net BEx productivity benefits of over $41 million during the period and intends to deliver greater than $30 million of sustainable savings to offset the rising costs pressure. The Business Excellence model delivered gross benefits of over $75 million to the group’s results in fiscal year of 2015. The group is also seeking to decrease costs and accordingly became a major customer for a new pipeline which would offer conventional gas to its Phosphate Hill plant in North West Queensland for over 10 years from around late 2018. With this agreement, the group would be able to reduce its gas costs by over $55 million as compared to its present costs. Meanwhile, Incitec Pivot is focusing on other opportunities and accordingly developed its $1 billion Moranbah ammonium nitrate plant to leverage the growing demand for resources in China. IPL invested in WALA, an ammonia plant which is under construction at Louisiana, to leverage the shale gas opportunity in the US.

The shares of IPL delivered a year to date returns of 22.05% (as of December 29, 2015) and are trading at reasonable valuations. Incitec Pivot generated a decent dividend yield. We give a “BUY” recommendation on Incitec Pivot at the current price of $3.96

IPL Daily Chart (Source: Thomson Reuters)

Coca-Cola Amatil Ltd

.png)

CCL Dividend Details

Focusing on health alternatives to offset core business performance: The shares ofCoca-Cola Amatil Ltd (ASX: CCL) rose 3.44% during the last six months (as of December 29, 2015) while investors remained concerned over the group’s returns on Indonesia markets. Indonesia is estimating a tax on drinks with sugar which might hurt the volumes of CCL Indonesia as the group is the sole distributor in Southeast Asia. However, we expect a meek impact as Indonesia seems to account for about 5% of the earnings. CCL’s parent company, The Coca Cola Company invested USD 500 million into the Indonesia market by acquiring a 29.4% equity interest in CCA Indonesia, to leverage the flourishing Indonesia market driven by the increasing consumer purchasing power.

.png)

Indonesia and PNG first half of 2015 performance (Source: Company Reports)

On the other hand, Coca-Cola Amatil started focusing on healthy options to address the growing consumer preference towards healthy alternatives like iced coffee and water. As a result, CCL was able to deliver a 4.9% yoy increase in trading revenue to $2.4 billion for the first half of 2015. Meanwhile, Coca-Cola Amatil shares surged around 2.31% in just last five days (as of December 29, 2015), and we believe the stock may gain momentum in the coming months. Accordingly, we give a “HOLD” recommendation at the current price of $9.30

CCL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.